Travel Allowance, Company Car or Reimbursement? The Tax Rules

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

Your client phones in a panic. SARS has issued an additional assessment and they owe far more tax than expected.

The reason? They received a travel allowance every month, assumed it was tax-free because they spent it on fuel, but never kept a logbook.

Unfortunately, that is not how the tax rules work.

Travel-related payments are one of the most misunderstood areas of South African payroll tax. Many employees believe a travel allowance is simply extra money for fuel. In reality, most travel payments are taxable, and without the correct records, employees may lose valuable deductions.

This article explains the four main types of employer travel payments, how each is taxed, and why keeping a logbook is often essential.

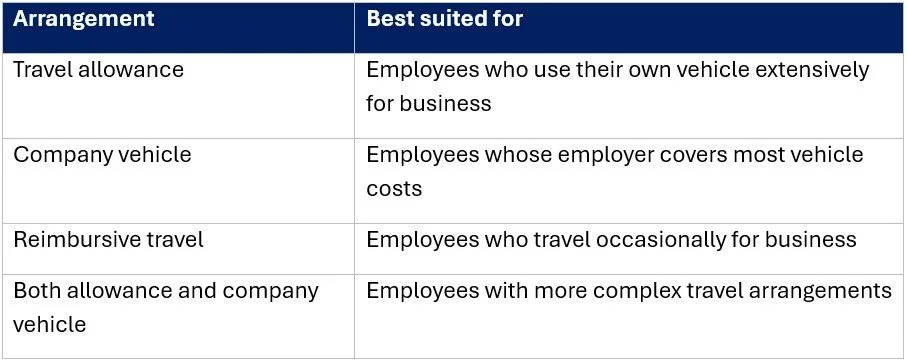

The Four Types of Employer Travel Payments

The four common employer travel arrangements are discussed below.

An employee uses his or her own car for business purposes as part of the employment.

The employee is given a company vehicle which is then used for business and also for private travel.

The employer pays the employee back for actual business kilometres travelled as and when the travel happened.

The employee receives both a travel allowance and a company vehicle.

Scenario 1. Travel Allowance

A travel allowance is a fixed amount paid by an employer to an employee who uses their own private vehicle for business travel.

How is it taxed?

A travel allowance is not tax-free.

For PAYE purposes, 80% of the allowance is normally included in the employee's taxable remuneration. The employer calculates PAYE using this amount as part of taxable remuneration.

If the employer is satisfied, based on written confirmation, that at least 80% of the employee's travel is for business purposes, only 20% of the allowance is subject to PAYE during the year.

Can the employee claim a deduction?

Yes. When submitting the annual ITR12 tax return, the employee may claim a deduction for qualifying business travel. To do this, a valid logbook is essential. Without a logbook, SARS will not allow the deduction.

Example

Thabo receives a travel allowance of R5 000 per month. His employer taxes 80% of the allowance for PAYE purposes.

During the year, Thabo keeps a detailed logbook showing 15 000 business kilometres. When he submits his tax return, he calculates his allowable deduction using the SARS travel cost method. This reduces his taxable income and results in a tax refund.

Without the logbook, he would lose the deduction entirely.

Scenario 2. Company Vehicle

Instead of paying a travel allowance, some employers provide employees with a company vehicle.

Although the employee does not own the vehicle, the private use of that vehicle is regarded as a taxable fringe benefit under the Seventh Schedule to the Income Tax Act.

How is the benefit calculated?

The monthly taxable benefit is generally:

3.5% of the determined value of the vehicle; or

3.25% if the vehicle was acquired with a maintenance plan.

For PAYE purposes, employers normally include 80% of this fringe benefit in taxable remuneration each month.

Where the employer is satisfied that at least 80% of the vehicle's use is for business, only 20% is included for PAYE purposes.

Can the taxable benefit be reduced?

Yes. At year-end, SARS recalculates the taxable fringe benefit using the employee's actual business and private use, supported by a complete logbook. No logbook means no adjustment.

Scenario 3. Reimbursive Travel Payments

A reimbursive travel payment differs from a travel allowance.

Instead of paying a fixed monthly amount, the employer reimburses the employee for actual business kilometres travelled at a rate per kilometre.

How is it taxed?

The tax treatment depends on:

the reimbursement rate paid per kilometre; and

the total business kilometres travelled during the tax year.

Generally:

If the reimbursement is paid at or below the SARS prescribed rate and the employee travels 12 000 business kilometres or less during the year, the reimbursement is generally not subject to PAYE.

If the reimbursement rate exceeds the SARS prescribed rate, the excess is taxable.

If business travel exceeds 12 000 kilometres during the year, different tax rules apply and the reimbursement must be taken into account when the employee submits their tax return.

A logbook should always be maintained to support the business kilometres travelled.

Example

Nomsa is reimbursed at the SARS prescribed rate for 14 500 kilometres during the tax year.

Because her business travel exceeds 12 000 kilometres, the reimbursement must be taken into account when she submits her income tax return.

If she keeps a complete logbook, SARS can verify the business kilometres travelled and assess the reimbursement correctly. If she cannot produce a valid logbook, she may be unable to substantiate the business travel, which could result in the reimbursement being taxed on assessment.

Scenario 4. Receiving Both a Travel Allowance and a Company Vehicle

Some employees receive both a travel allowance and access to a company vehicle.

Special tax rules apply in these circumstances.

The employee cannot simply claim deductions as though only one vehicle exists. The logbook must clearly distinguish between travel undertaken using the company vehicle and travel undertaken using the employee's own vehicle.

Professional advice is often worthwhile where both arrangements exist.

When is a Logbook Required?

If there is any travel-related benefit or allowance reflected on an employee's IRP5, the first question should be:

"Do you have a logbook?"

If there is a travel-related allowance or benefit on the IRP5, employees should keep a complete logbook if they wish to claim deductions, reduce a company-car fringe benefit or substantiate reimbursive business travel. Consider the following scenarios and whether a logbook is required.

Receiving a fixed travel allowance. Yes, keep a logbook to claim a deduction during final tax assessment.

Using a company vehicle (to reduce fringe benefit). Yes keep a logbook

Receiving a reimbursive payment. Yes, keep a logbook to confirm business kms.

No vehicle benefit of any kind is received. No, you do not need a logbook.

A valid logbook should include:

Date of each trip

Starting point

Destination

Business purpose of the trip

Opening odometer reading

Closing odometer reading

Total business kilometres

Total private kilometres

Opening odometer reading at the beginning of the tax year

Closing odometer reading at the end of the tax year.

Remember that travelling between home and your normal place of work is regarded as private travel and is not deductible.

SARS accepts both manual logbooks and its official electronic e-Logbook. As noted in the SARS Travel e-Log Book guide for 2025/2026, logbooks must be kept for at least five years and may be requested during an audit. The guides for the different tax years can be found on the SARS website.

Common Mistakes by Employers

Many payroll errors occur because employers misunderstand the rules.

Some of the most common mistakes include:

Paying a travel allowance without reminding employees to keep a logbook.

Applying the reduced 20% PAYE inclusion without written confirmation that business travel exceeds 80%.

Reimbursing employees above the SARS prescribed rate without taxing the excess.

Failing to monitor employees who exceed the qualifying business kilometre limits.

These mistakes often result in unexpected tax liabilities for employees or PAYE compliance issues for employers.

Not reviewing the arrangement when km exceed 12,000. Reimbursive payments look clean until the employee passes the threshold. If the employer is not tracking this, the payroll is wrong for part of the year.

Which Arrangement Is Best for the Employee?

There is no universal answer, but here is how to think about it.

Travel allowance in own vehicle

This works best when the employee travels high business kilometres relative to private use. The logbook deduction can be substantial. The employee carries the running costs of the vehicle but claims them back through the tax system.

Company vehicle

Works best when the employer bears all costs. The fringe benefit can be reduced significantly with a good logbook. If the vehicle is used heavily for business, the net tax cost is low.

Reimbursive payments

The simplest arrangement for low-to-moderate travel. If the kilometres stay below 12,000 and the rate stays at or below R4.84/km (currently R4.95/km for the 2027 year of assessment), there is no tax at all. Clean, simple, and SARS-friendly. If business travel exceeds 12 000 km during the year, the reimbursive allowance must be taken into account on assessment and the employee's tax position is determined under the normal assessment rules.

The more private travel an employee does, the less favourable any of these arrangements become. SARS taxes the private benefit, not the business one.

What to Check Right Now

Before the end of the tax year, employers should review three important areas:

Travel allowances – Have employees been reminded to keep logbooks? Review every IRP5 code for travel. Codes 3701 (travel allowance) and 3802 (company vehicle fringe benefit) should trigger an immediate logbook check. If the client cannot produce one, the risk sits with the employee at assessment.

Reimbursements – Are reimbursement rates and business kilometres being monitored? Check reimbursement rates and km totals. If any employee is being paid above R4.84/km (currently R4.95/km for the 2027 year of assessment) or is approaching 12,000 business km, payroll needs to be adjusted now, not in February.

PAYE calculations – Is the correct 80% or 20% inclusion being applied, supported by written evidence where required? Confirm the PAYE inclusion percentage. If the employer is applying the 20% inclusion for high business use, make sure the written confirmation from the employee is on file. Without it, the employer is exposed.

Travel-related tax does not have to be complicated.

The biggest problem is usually not the legislation, it is poor record-keeping.

A simple logbook can make the difference between receiving a tax refund and facing an unexpected assessment from SARS.

For accountants and payroll professionals, checking travel arrangements before year-end is one of the easiest ways to protect clients, avoid PAYE errors and ensure employees claim the deductions they are entitled to.

Trending