Provisional Tax and the Side Hustle: Protecting Informal-Economy Clients

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

SARS now matches bank and third-party data against every tax return, and the gig and informal economy is squarely in its sights. The e-hailing driver, the online seller and the weekend freelancer all earn income SARS can increasingly see, yet many have never heard of provisional tax. For accountants, this is both risk and opportunity: act early, keep these clients compliant, spare them penalties and estimated assessments, and turn a once-a-year scramble into a recurring advisory service worth charging for.

The income SARS used to miss

For years, the gig economy (freelance and platform-based work such as e-hailing, delivery and online selling) and the wider informal economy operated in a blind spot. The e-hailing driver, the online reseller, the freelance designer, the salaried employee with a weekend stall. Money moved through bank accounts and apps, and little of it reached a tax return.

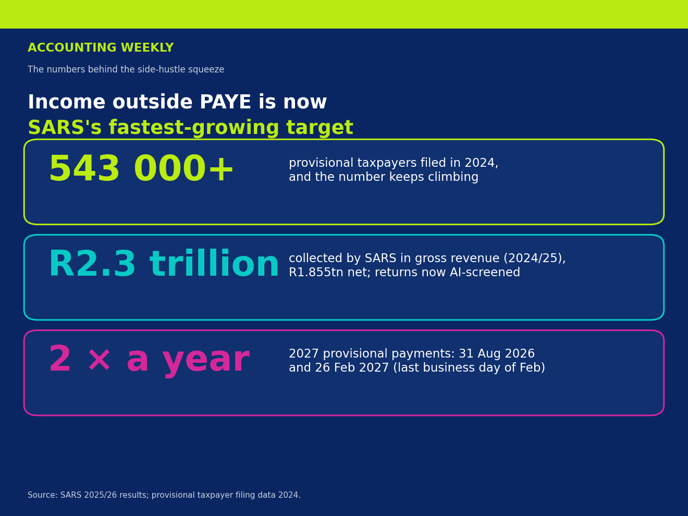

That blind spot has closed. Under section 26 of the Tax Administration Act, SARS receives third-party financial data directly from banks, financial institutions, medical schemes and fund administrators, and reconciles it against each taxpayer’s declaration, increasingly before the return is even assessed. SARS collected a record R2.3 trillion in gross revenue in 2024/25 (R1.855 trillion net of refunds), and, according to SARS’s reporting to Parliament’s Standing Committee on Finance, its AI-driven risk models now screen returns and flag discrepancies at scale.

The practical effect is simple. A side hustle still gets paid into a bank account, whether that is an app payout or a customer EFT, and that leaves a trail. Apps and marketplaces do not report to SARS directly, but the deposits do, and when a client’s declared income does not match what SARS can see, a verification letter follows.

Why your client is probably a provisional taxpayer

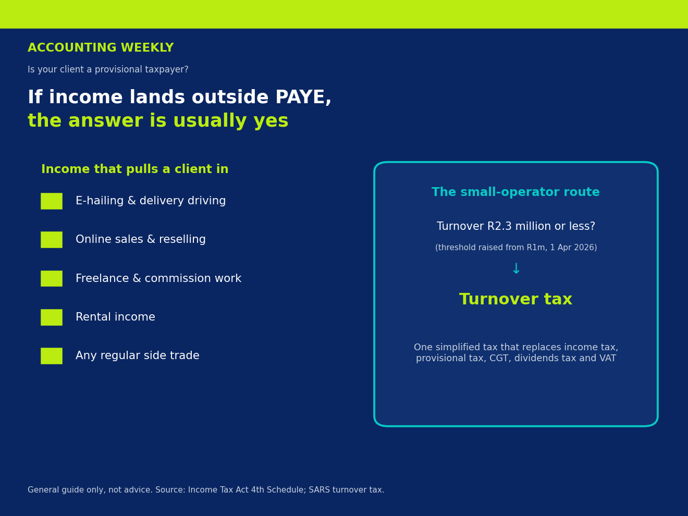

The Fourth Schedule to the Income Tax Act treats a person who earns income not subject to PAYE as a provisional taxpayer. A natural person with no business, whose only extra income is modest interest or rental below the set limits, may fall under an exclusion. The moment that income comes from a trade, however, that shelter falls away and the client is in the provisional system, regardless of how small the amounts feel.

Many clients do not know this. They treat tax as something their employer handles through monthly deductions, and assume the extra income is informal or invisible. According to SARS data, more than 543,000 provisional taxpayers filed returns in 2024, and the number continues to rise as more South Africans take on additional income to cope with cost-of-living pressure.

Provisional tax runs on two compulsory payments each year. For the 2027 year of assessment, which runs from 1 March 2026 to 28 February 2027, the first payment is due by Monday 31 August 2026 and the second by the last business day of February 2027, which is Friday 26 February 2027 (28 February falls on a Sunday). A third, voluntary top-up payment can follow by the end of September 2027 to settle any shortfall before interest builds. Underestimate the income, or miss a deadline, and SARS adds penalties and interest. Where no return is submitted, SARS may raise an estimated assessment using the data it already holds.

The accountant as protector

This is where your role matters most. The clients caught by this shift are rarely sophisticated taxpayers. They are drivers, traders, makers and freelancers building something from very little, and a penalty or an estimated assessment can wipe out a month’s earnings.

For the smallest operators, turnover tax offers relief. Available to businesses with a qualifying annual turnover of R2.3 million or less (raised from R1 million with effect from 1 April 2026), it replaces income tax, provisional tax, capital gains tax, dividends tax and, unless the business elects to stay in the VAT system, VAT, with a single simplified calculation. For everyone else, there is no separate provisional-tax registration to complete. The onus sits with the taxpayer to work out that they are liable and to request and submit the IRP6 return on eFiling, so the practical work is getting them set up on eFiling, keeping a basic monthly income record, and filing an accurate estimate that avoids penalties.

Where a client has carried undeclared income for years, the Voluntary Disclosure Programme under the Tax Administration Act provides a legal route to regularise their affairs before SARS acts, provided the disclosure is voluntary, complete, and made before an audit begins.

From compliance task to advisory service

Handled well, this is more than a clean-up job. A client who receives a verification letter is anxious and ready to act. That is the moment to move from once-a-year preparer to year-round advisor.

Flag every client with irregular or additional income. Get their IRP6 filed before the next deadline rather than after the letter. Build a simple record-keeping habit. Then price the work as an ongoing service. You protect the client, and you create predictable, recurring revenue for your practice.

When you keep these businesses compliant and growing, you do more than file returns. You help keep the informal and gig economy, and the households it supports, on a stable footing.

Your protect-the-client checklist

Run a bank-deposit review for every client with irregular or extra income.

Flag who is a provisional taxpayer: anyone with trade, freelance, rental or gig income outside PAYE.

Get them onto eFiling and submit the IRP6; remember there is no separate registration step.

Test turnover tax eligibility (turnover of R2.3 million or less) for the smallest operators.

File an accurate first estimate to avoid underestimation penalties.

Diarise both 2027 deadlines: first payment 31 August 2026, second 26 February 2027.

Keep a simple monthly income record so each estimate stays realistic.

Where a client has undeclared history, assess the Voluntary Disclosure Programme before SARS acts.

Package the work as a recurring compliance service, and price it accordingly.

Key takeaways

Income earned outside PAYE generally makes a client a provisional taxpayer under the Fourth Schedule, even when the amount is small.

SARS receives third-party data from banks and financial institutions and matches it against returns, so undeclared side income is increasingly visible.

For the 2027 year of assessment the first provisional payment is due 31 August 2026 and the second by 26 February 2027, with penalties and interest for underestimation or non-submission. There is no separate registration; the onus is on the taxpayer to file the IRP6.

Turnover tax, for businesses with turnover of R2.3 million or less (raised from R1 million on 1 April 2026), can simplify compliance for the smallest operators.

The Voluntary Disclosure Programme offers a legal route to correct years of undeclared income before SARS takes action.

Have a look at our upcoming CPD offerings

Trending