A Taxman’s Casebook Trusts: Viable or not?

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

Alfred E. Neuman, the fictitious, gap-toothed mascot and cover boy of the American humour publication, MAD Magazine, said:

“Today, it takes more brains and effort to make out the income-tax form than it does to make the income”

This statement is probably most applicable where a taxpayer needs to navigate the complex tax regime applicable to Trusts.

Whereas a company or a natural person is simply taxed on any income that accrues to the taxpayer, the income of a Trust may, depending on the circumstances, be taxed in the hands of the following:

Donor (“funder”);

Beneficiary; or

Trust.

Where the Trust itself is taxed, it is taxed at a flat rate of 45% with 80% of capital gains being subject to normal tax making the effective capital gains tax rate 36%. It follows that the tax rates applicable to Trusts is highly punitive.

The legislator and SARS have over the past 10 years targeted Trusts as a tax planning tool with the following notable events:

Legislative changes

Introduction of Section 7C resulting in low interest/interest free loans to trusts or companies owned by trusts attracting annual donations tax in the hands of the lender.

Amendment of Section 25B that prohibits the “flow through” principle to apply to non-residents.

Amendment of Section 10(1)k) dividend exemptions to make certain dividends received via discretionary share incentive trusts taxable in the hands of beneficiaries.

SARS initiatives

SARS challenged the application of the “flow-through principle” via multiple trusts for Capital Gains in the highly publicised Thistle Trust Appeal Court case. The Appeal Court found that capital gains do not retain its nature if vested via multiple trusts.

SARS targets the application of Section 25B where the Trustees meeting vesting income in beneficiaries occurs after year-end. If the “vesting” only occurs after year-end, then the income is taxed in the hands of the trust and not in the hands of the beneficiaries.

The ITR 12 and ITR 14 contains numerous questions whether or not the taxpayer established or is a beneficiary of a local or foreign trust.

SARS focuses on high-net-worth individuals who externalised wealth via foreign trusts. Whilst the SA Reserve Bank has relaxed its position on so-called loop structures, SARS strengthened the policing of abusive practices by applying Transfer Pricing principles and effective management principles.

Are Trusts Still Viable?

The question arises whether Trusts are still worthwhile. The answer to that is complex and cannot be applied to all instances. The following should be considered:

A trust remains an attractive estate planning tool. It is however very difficult to transfer existing wealth to a Trust without triggering Capital Gains Tax or deemed annual donation in terms of section 7C.

Low value assets with good growth potential could potentially be transferred to a trust without triggering significant donations tax or capital gains tax.

The attractiveness of Trusts as Employee Incentive mechanisms has diminished due to the anti-avoidance legislation found in section 10(1)(k).

Advice to Trustees

Trustees should be familiar with tax legislation and should ensure that the documentary evidence supports the tax positions taken. Trustees are advised of the following:

Ensure that vesting occurs before year-end (28 February).

If dividends are to be vested in an entity that enjoys reduced Dividend Tax Rates (e.g. a Public Benefit Organisation (“PBO”) or resident company), ensure that the necessary declarations are provided to the company declaring the dividend. If a dividend attracted 20% dividend tax but is vested in e.g. a PBO in the same tax year, then a refund of Dividend Tax can be requested from the company that paid the dividend.

Ensure provisional taxes are calculated based taking into account the complex tax legislation affecting the vesting of income.

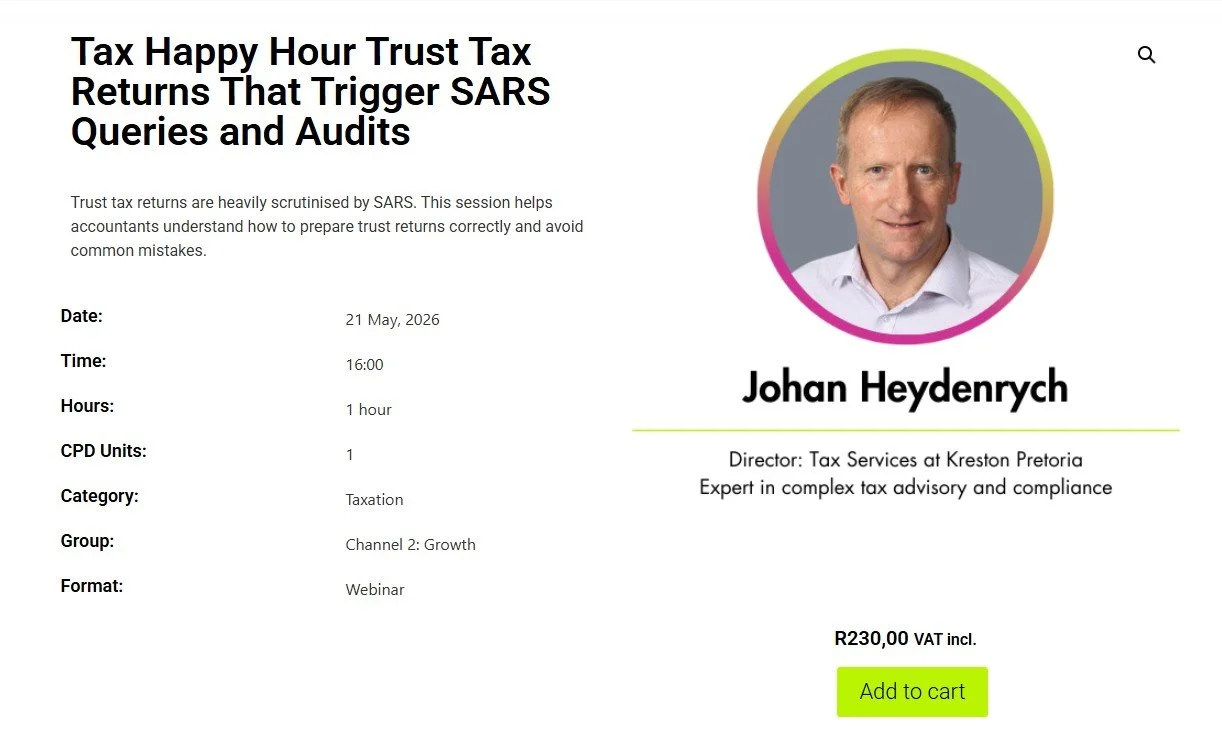

Enroll to CIBA’s Tax Happy Hour Trust Tax Returns That Trigger SARS Queries and Audits and learn more about trusts and how they are taxed.

By attending this event, you will learn:

Identify common problem areas in the preparation of trust tax returns

Understand where trust returns most often go wrong

Learn how to prepare trust returns in a safe, compliant, and defensible manner

Trending