The Gold Loophole SARS Just Closed

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

If you have any client touching gold, scrap metal, refining, jewellery, or mining waste, National Treasury just published the Draft Amendments to the Regulations on Domestic Reverse Charge Relating to Valuable Metal, issued in terms of section 74(2) of the Value-Added Tax Act, 1991 (Act No. 89 of 1991) that changes the rules under their feet. It's open for comment until 30 June 2026 and proposed to start on 1 August 2026. Here's what we can expect and how it lands on your desk.

First, what the reverse charge actually does

Normally the seller charges VAT, the buyer claims it back, and SARS sits in the middle. With gold, fraudsters turned that middle into a cash machine. A "missing trader" sells gold-bearing goods, adds 15% VAT, pockets the VAT, then vanishes before SARS comes looking. The buyer still claims the refund. SARS pays out money it never collected.

The Domestic Reverse Charge (DRC) breaks that cycle. When a supply counts as "valuable metal," the seller charges no VAT. The buyer declares both the output VAT and the input VAT in the same return. The two net to zero. No cash refund leaves SARS, so there is nothing to steal. This is the same trick that other countries used to shut down in the so-called "carousel" fraud. In a carousel scheme, the same goods get sold round and round through a chain of companies, often across borders. Each time, one seller in the chain charges VAT, pockets it, and disappears before paying SARS, while the next buyer claims that VAT back. The goods go in circles, but the VAT refunds keep flowing out. Tax authorities killed it the same way: stop the seller from charging VAT at all, so there is no cash sitting in the chain to steal.

So the main question is: does the supply count as "valuable metal" or not? Inside the net, the reverse charge applies and the fraud door shuts. Outside it, normal VAT runs and the cash refund is back on the table. The draft is all about who sits inside that net.

Before anyone rewrites their VAT manuals, it is worth noting what the draft does not do. The amendments only change the Domestic Reverse Charge (DRC) Regulations issued under section 74(2) of the VAT Act. They do not change the VAT rate, alter VAT registration requirements, or rewrite the general VAT treatment of ordinary goods and services. The focus is much narrower: refining the definition of "valuable metal" and closing perceived gaps in the reverse-charge system for certain gold-bearing materials. For most VAT vendors outside the affected supply chains, business continues exactly as before.

The hole that was left open

The rules already carried a "de minimis" rule. Any goods with less than 1% gold by gross weight were excluded from the DRC. The idea was fair, if a product only has a trace of gold by accident, don't drag it into the reverse-charge admin.

The problem is that low-grade gold material can still be worth quite a sum. Tailings, waste rock, and unprocessed ore often sit well under 1% gold by weight but carry real value once processed. Because they fell under 1%, they slipped out of the net, and the old refund scheme came straight back to life. SARS has repeatedly identified VAT fraud involving gold and precious-metal supply chains as an enforcement concern. As Accounting Weekly covered in Gold Mines, VAT Scams and Money Laundering, fraudsters disguise stolen or illegally mined gold as legitimate "scrap," feed it into refineries, and submit false VAT refund claims through fly-by-night suppliers that disappear once SARS comes knocking.

What the draft actually changes

Two changes, both aimed at the same hole.

The definition of "residue" is widened. The current version only counts waste as "residue" if it came from a mining operation. The draft strips those words out. Debris, tailings, slimes, slurry, waste rock, foundry sand, and similar waste now count as residue no matter where they come from. That pulls more gold-bearing waste back into "valuable metal."

The under-1% exclusion is narrowed hard. It no longer applies to everyone. It now only covers six named industries: medical, electronics, dentistry, automotive, defence, and aerospace. On top of that, any gold recycled from those industries has to stay and be used within those same industries to keep the exclusion. A new line also excludes gold-plated jewellery where the gold is only a minor part.

Put together, the effect is simple. The amendments are expected to bring a wider range of gold-bearing tailings, waste rock and similar residue within the DRC framework. Genuine trace-gold industrial supplies, a circuit board with a whisper of gold, a dental alloy, are left alone. SARS keeps the fraud door shut without burying clean industrial businesses in reverse-charge paperwork.

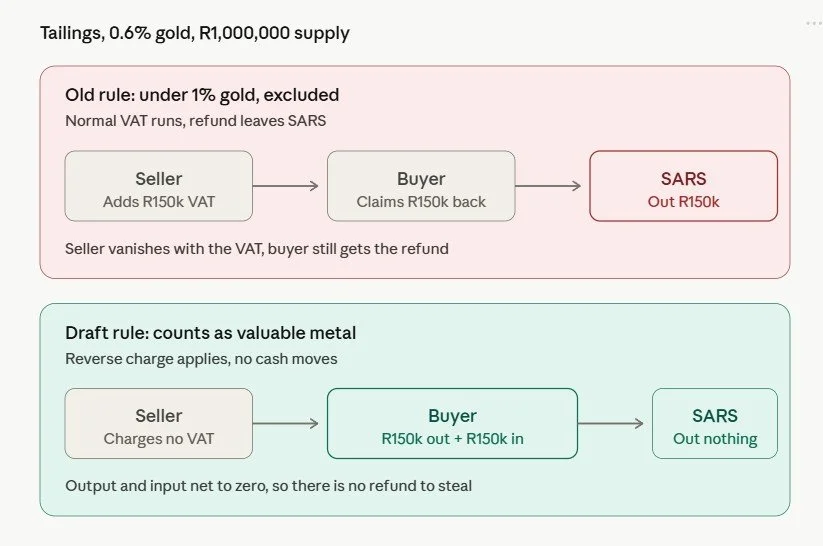

See it in one transaction

Picture a trader selling a batch of gold-bearing tailings, 0.6% gold by gross weight, for R1,000,000.

Under the old rule: under 1% gold, so excluded. Normal VAT runs. The seller adds R150,000 VAT. A dishonest seller disappears with that R150,000 while the buyer claims R150,000 back from SARS. SARS is out R150,000. That is the leak.

Under the draft: tailings now count as residue, and gold-processing tailings are not one of the six protected industries, so the supply is "valuable metal." The reverse charge applies. No VAT changes hands. The buyer books R150,000 output and R150,000 input in the same return. They net to zero. There is no refund to steal.

Now the supply that stays out: an electronics maker sells circuit-board offcuts at 0.3% gold, to be recycled inside the electronics sector. Electronics is on the list and the gold stays in the industry, so the exclusion still applies. Normal VAT runs and the business carries on as before.

The line moved. The same batch of tailings that was clean yesterday is now a reverse-charge supply.

What this means for your desk

This is where you earn your fee. Clean, reconciled records are now the difference between a refund that holds and a SARS query that doesn't. As we covered in VAT Reconciliation Doesn't Have to Hurt, the numbers in the books have to match the returns, or you are exposed the moment SARS looks closer.

Three things you can do today:

Check your client list for exposure. Anyone in scrap metal, refining, jewellery, mining, recycling, or waste handling needs to know whether their supplies cross into "valuable metal" from 1 August 2026. Gold content by gross weight is now the test that decides their VAT treatment.

Re-run the gold-content question on every borderline supply. The under-1% shortcut is gone for most clients. Sitting below 1% no longer means "excluded" unless the client is in one of the six protected industries and keeps the gold there.

Use the comment window. Comments close 30 June 2026. If a client in a legitimate low-gold trade gets caught by the wording, a submission to Treasury before the deadline is real, billable advisory work, not just compliance.

This is the shift from "pair of hands" to trusted advisor. You are the person who spots the exposure before SARS, a buyer, or a liquidator does. That is worth charging for.