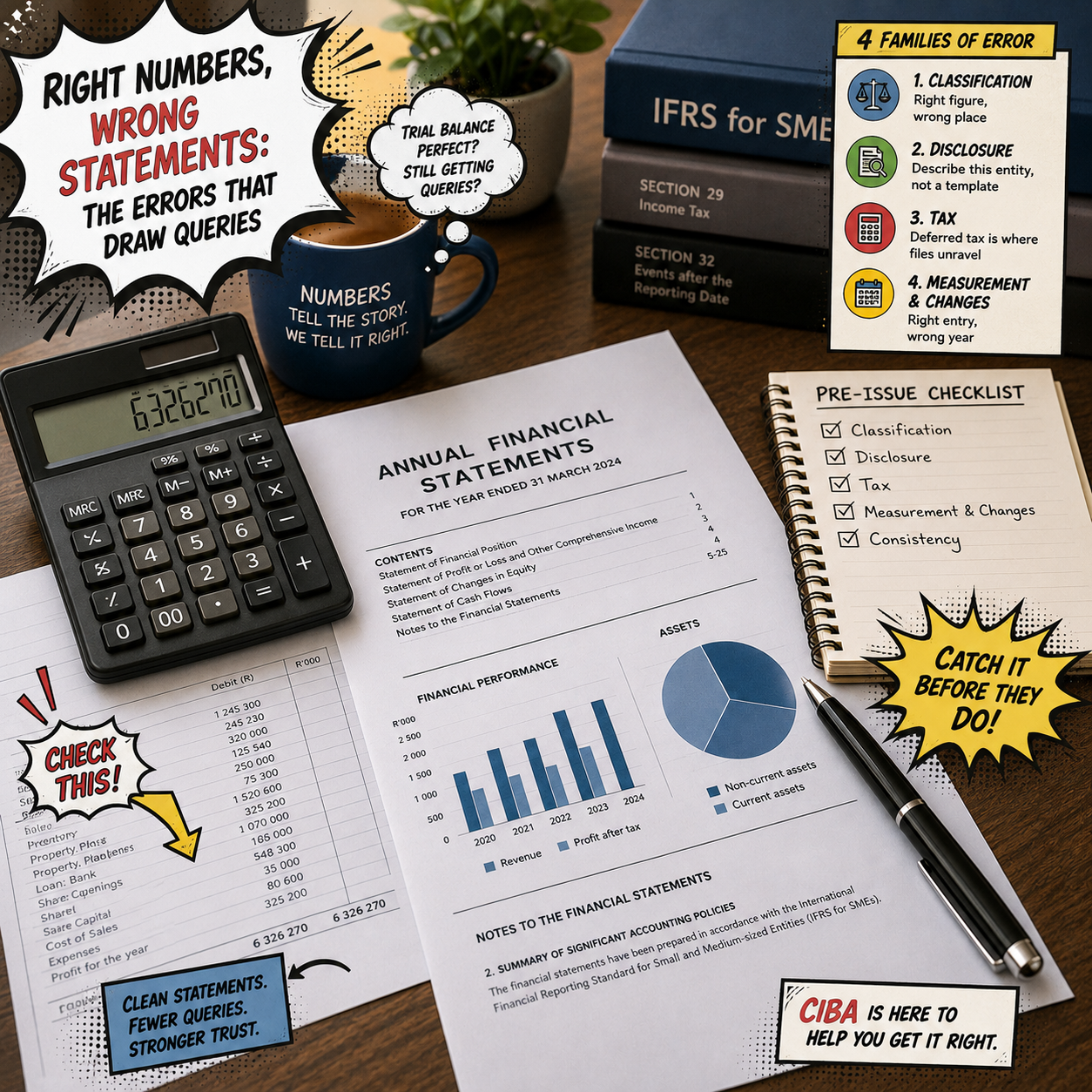

Right Numbers, Wrong Statements: The Errors That Draw queries

A trial balance can be perfectly correct and still produce a set of annual financial statements that SARS, the bank and the reviewer keep sending back. The difference is rarely the arithmetic; it is a handful of classification, disclosure and tax errors that repeat across SME files. Here are the ones to watch, grouped, with a checklist you can run before sign-off.

Fair Value Finally Makes Sense: The IFRS for SMEs Reset

Fair value has always been part of IFRS for SMEs, but the rules were not always clear. Different sections used different guidance, which often caused confusion. The new Section 12 changes this by providing one clear method for measuring fair value across the whole standard. It introduces a simple hierarchy, clear definitions, and better disclosure requirements. This helps accountants apply fair value more consistently and gives users of financial statements a better understanding of how values have been determined and reported.

Your Financial Instruments Fallback Is Gone. Here Is What Replaces It.

The IAS 39 fallback is gone, and the new IFRS for SMEs Section 11 brings a simpler, more practical approach to financial instruments. The key change is the introduction of the SPPI test, which helps determine whether instruments are measured at amortised cost or fair value. Accountants should now review financial instruments, intragroup guarantees, and extended credit arrangements to ensure compliance with the third edition. While some rules have changed, the standard remains focused on providing clear, relevant, and reliable financial information for SMEs.

You Think You Know Who Controls That Company. The New Rules Might Disagree.

For many SMEs, the biggest change in the updated IFRS for SMEs is not how much of a company is owned, but who actually controls it. The revised Section 9 introduces a broader definition of control that looks beyond voting rights and focuses on who has the power to direct key decisions, who is exposed to the risks and rewards of the business, and who can use that power to influence outcomes. As a result, family groups, trust structures, and companies with dispersed shareholders may need to reassess whether consolidation is required, even where no single party holds a majority stake.

Assets, Liabilities and the Rule That Changed Everything

What qualifies as an asset? What creates a liability? These questions sit at the heart of every set of financial statements, yet the answers have changed significantly with the latest IFRS for SMEs updates. The revised framework moves away from a strict focus on probability and places greater emphasis on rights, obligations, relevance, and faithful representation. For accountants and business owners alike, this shift could affect how software licences, intellectual property, contractual rights, legal claims, and other uncertain items are recognised and reported in the years ahead.

The Accounting Standard That Quietly Changed Everything

Accounting standards rarely make headlines, but the latest update to IFRS for SMEs is one of the most significant changes in years. With major revisions to revenue recognition, business combinations, consolidation, financial instruments, and fair value measurement, accountants and business owners need to start preparing now. The transition period is already underway, and those who understand the changes early will be best positioned to guide their clients through what comes next.

The Most Valuable Assets You Cannot See

Intangible assets are often some of the most valuable resources a business owns, yet they are also among the least understood. From software and licences to patents and trademarks, these assets help businesses generate income and remain competitive, even though they cannot be physically seen or touched. Understanding how IFRS for SMEs treats intangible assets is essential for finance professionals, particularly when deciding whether costs should be recognised as assets or expensed. By applying the principles of Section 18 correctly, accountants can ensure that financial statements remain accurate, reliable, and useful for decision-making.

Property, Property... Who Are You Really?

You have a property on the books. But is it working in the business, or is it earning money on its own? The answer determines whether it is classified as Property, Plant and Equipment (PPE) or Investment Property under IFRS for SMEs. While the buildings may look the same, the accounting treatment is very different. This article breaks it down in simple terms so you can classify property correctly and avoid costly mistakes.

Family Deals, Trust Rentals: 3 Questions to Ask

Related-party transactions are one of the biggest hidden risks in family-run businesses. When family members own suppliers, properties, trusts, or other businesses connected to the company, important disclosures can easily be missed. For independent reviewers and compilers, understanding these relationships is essential to producing reliable financial statements, managing compliance risks, and protecting both the client and their own professional reputation.

Going Concern in a High-Rate Economy: How to Spot the Cliff Before They Drive Off It

High interest rates are pushing many businesses closer to the edge without owners even realising it. A company can look profitable on paper while struggling to pay suppliers, SARS, staff, and the bank. This article explains the real warning signs accountants should watch for, from growing overdrafts to rising interest costs, and why spotting these problems early can save a business before it falls off the cliff.

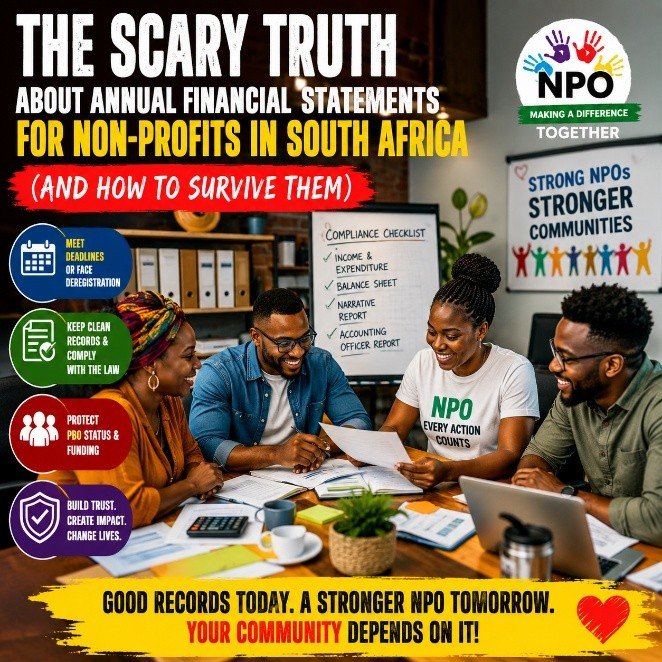

The Scary Truth About Annual Financial Statements for Non-Profits in South Africa

Thousands of South African non-profits are at risk of deregistration simply because their financial statements and compliance records are not in order. This article breaks down what every NPO needs to know about annual financial statements, reporting deadlines, audits, accounting officer requirements, and the real risks of getting it wrong. Written in simple language, it explains how proper financial records protect your funding, your reputation, and your ability to continue serving your community.

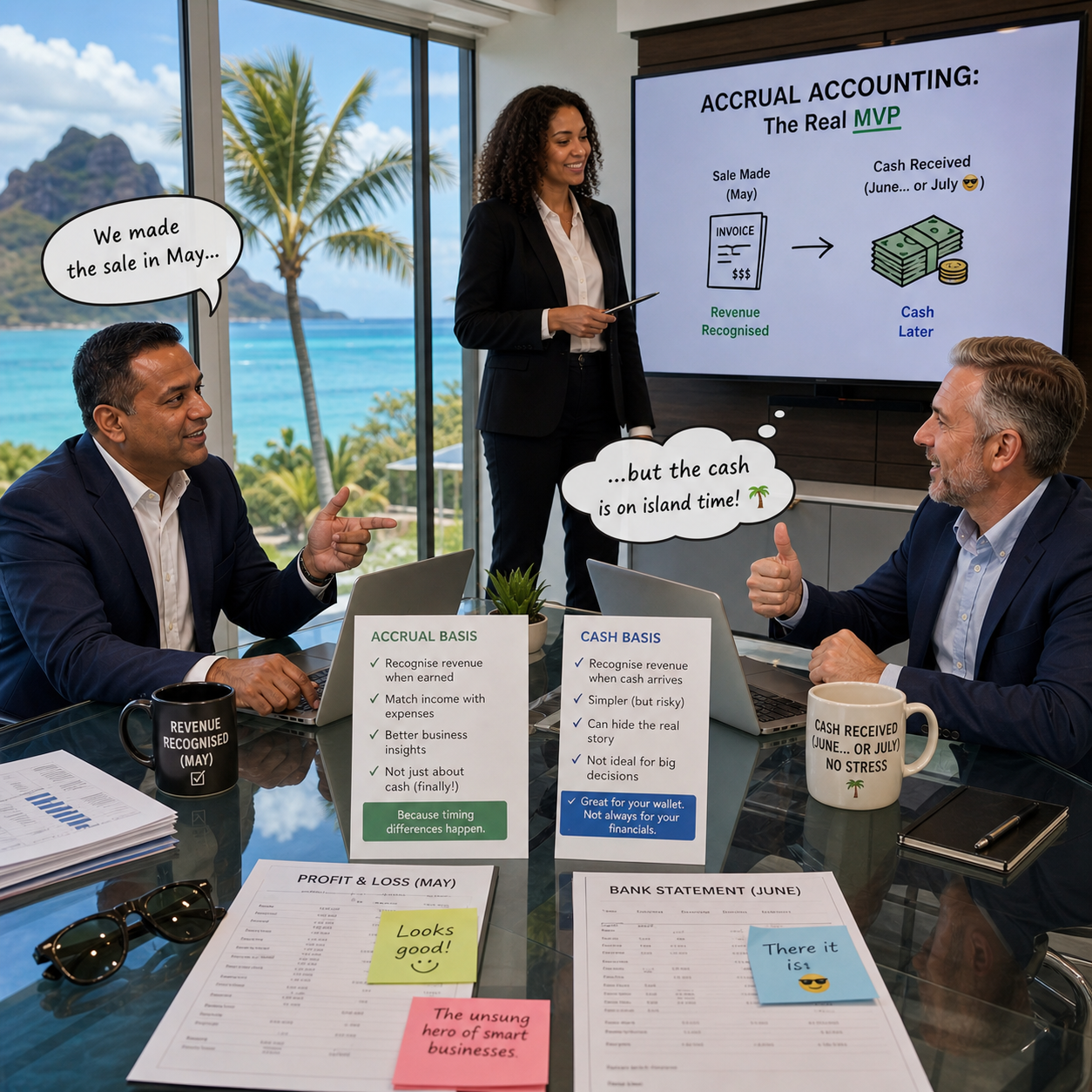

Accrual Accounting: The Quiet Principle That Changes Everything

Accrual accounting is the principle that ensures financial statements reflect what actually happens in a business, not just when cash moves in and out of the bank. By recognising income when it is earned and expenses when they are incurred, it provides a clearer and more accurate picture of performance. This approach moves beyond the simplicity of cash accounting and allows business owners and professionals to understand the true results of their activities, make better decisions, and avoid the misleading effects of timing differences.

IFRS for SMEs vs ISRS 4410: Know the Difference

When preparing a compilation report for an SME, it is important to understand that IFRS for SMEs and ISRS 4410 do not compete with each other. They serve different purposes. IFRS for SMEs is the framework used to prepare the financial statements, which means it determines how the numbers and disclosures are presented. ISRS 4410 is the standard that guides the practitioner on how to perform the compilation and how to write the report. In simple terms, IFRS for SMEs explains what the financial statements must look like, while ISRS 4410 explains how the practitioner does the work and reports on it.

How One “Yes” Can Cost Your Career in Municipal Finance

One phone call. One rushed decision, one mistake that changed everything. This article looks at real-world governance failures in local government that are costing accountants their careers, often not because of fraud, but because of pressure, shortcuts, and “just this once” decisions. If you work in or advise government, read below and learn how to protect yourself before it’s too late.

Trust Accounting Mistakes Under the LPA That Can End Your Career

Trust accounting under the Legal Practice Act 28 of 2014 is one of the most heavily regulated areas in South African legal practice, and one of the most commonly mismanaged. The mistakes are often technical in nature, but the consequences are anything but.

Sales, Stock and the Truth in Between

Every time a sale is made, your accounting system records more than just income. It also captures the cost of the product you sold, even if you never see it happening. This is what shows whether your business is actually making money. When you understand how revenue, VAT, cost of sales and inventory work together, your numbers start to make sense and your financial decisions become far more informed.

The Impact of Audit Quality on Financial Statements

Only 28% of audits passed the IRBA's latest inspection. The rest? Flagged, referred, or failed. And if you think that's the auditor's problem, think again. Your financial statements feed directly into every deficiency they're finding. Here's what it means for your practice and the steps you can take to ensure your clients' files hold up under scrutiny.

Before You Sign: The Final Steps of an Independent Review

Most independent review problems don’t start with technical standards, they start when the practitioner must draw a conclusion and sign the report. If the work performed isn’t clearly documented or evaluated, that final step becomes difficult. This practical guide walks through the key steps to finalise an independent review, evaluate findings, and issue a defensible report.

Not Everything You Buy Is an Expense

Not Everything You Buy Is an Expense

Bought a laptop for R20,000? Many business owners assume the full amount must be expensed immediately. In accounting, that’s not always the case. Some purchases are assets, not expenses — and how you record them affects your profit and financial statements. This practical guide breaks down fixed assets and depreciation using a simple example showing how an asset bought today can still appear on the balance sheet years later, and how spreading costs over time keeps financial statements accurate.

Segregation of Duties: Because Even Saints Need Supervision

In many small businesses, one trusted individual quietly becomes the centre of every financial process, approving payments, capturing transactions, reconciling bank accounts, and reviewing their own work. While this arrangement often grows out of necessity rather than intent, it concentrates risk in a way that is rarely visible until something goes wrong. Errors go undetected, pressure builds, and the absence of independent oversight undermines both governance and confidence in the numbers. What appears efficient on the surface can, over time, expose the business to financial loss, compliance failures, and reputational harm.