Prove It or Lose It: Treasury's New Budget Rules

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

National Treasury issued the 2027 Budget rules and the message is blunt: every rand will have to earn its place, or it gets taken away.

National Treasury released two documents that together reset how public money is planned, structured and justified. If you work in the public sector, advise an entity or municipality, or have clients who live off government contracts, these are not background reading. They decide whose budget survives the next three years. Here is what they are, and what they mean, starting at national level and working down to the provinces.

What Treasury actually published

The first document is the 2027 Medium Term Expenditure Framework (MTEF) Technical Guidelines, released through a media statement. These guidelines are issued every year under Section 27(3) of the Public Finance Management Act (PFMA). They tell every department and public institution exactly how to prepare their budget submissions for the next three years, in this case 2027/28 to 2029/30. They fire the starting gun on the budget process that ends with the fiscal framework tabled in October 2026 and the Budget Review in February 2027.

The second document is the 2026 Guidelines on Budget Programme Structures. This one is bigger than an annual update. It is the first major refresh of how budgets are built in more than a decade, and it changes the underlying logic of public budgeting. One sets the spending rules. The other rebuilds the structure the spending sits in. Read together, they point in the same direction: less spending, more proof.

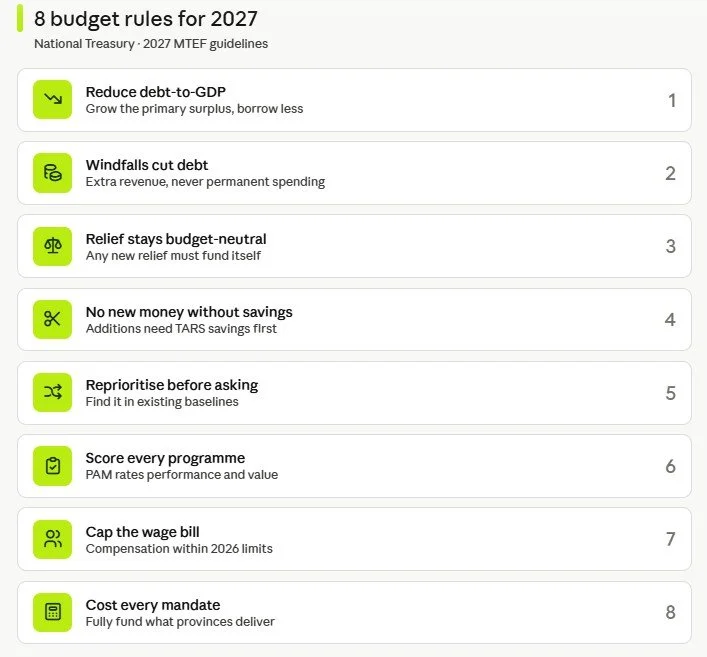

The national stance: spend less, prove more

The MTEF guidelines are anchored in one goal. Government wants to stabilise and then gradually reduce South Africa's debt-to-GDP ratio. The reason is simple and painful: interest on existing debt already swallows almost one fifth of all tax revenue. With the economy still growing slowly, Treasury says spending growth has to be held back and pointed at priorities only.

To get there, departments are now held to a set of firm budget principles. The headline rules are these.

Government must keep growing its primary budget surplus, where revenue beats non-interest spending by a wider and wider margin, so it can borrow less.

If revenue comes in higher than expected, the windfall goes to cutting debt or once-off needs like infrastructure. It will not fund permanent spending increases.

Any new relief must be budget-neutral. Treasury points to the recent fuel levy relief, granted in response to high oil prices from the Middle East conflict. It cost R17.2 billion, but was covered by underspending and higher revenue, so it added nothing to the deficit. Future relief has to work the same way.

New spending must first come from reprioritising existing baselines. Departments look inside their own budgets before asking for more.

Compensation budgets stay capped at the 2026 Budget limits. In plain terms, departments must manage headcount to stay inside the wage bill.

National departments must fully cost any policy they expect provinces and municipalities to carry out, so they do not create unfunded mandates.

Two tools enforce all of this. The Targeted and Responsible Savings (TARS) initiative hunts down programmes that are not cost-effective, do not deliver, or are simply low priority, and pushes to cut or close them. The Programme Assessment Matrix (PAM) gives departments a structured way to score how each programme actually performs. Additions to the overall budget will only be considered for priority work, and only if TARS has already found the savings to fund it.

This is the same direction Treasury signalled a year ago. As covered in Accounting Weekly's breakdown of the 2026 MTEF Budget Guidelines, the shift to evidence-based, results-first budgeting is not a one-year experiment. It is becoming the norm.

A new blueprint for how budgets are built

The Programme Structures guidelines answer a different question: not how much to spend, but how the budget itself must be shaped.

The biggest change is a shift away from activity-based budgets towards objective-based, results-oriented structures. Old budgets often described what a unit does. The new approach demands that funds link to measurable goals and real socio-economic outcomes. If you cannot show the result, you cannot easily defend the money. Three more changes matter.

Cross-cutting priorities are now compulsory. Departments must deliberately build gender equity, climate change, and science, technology and innovation into their programmes and subprogrammes. These can no longer be bolted on at the end. They have to be visible in the structure.

Accountability is split into three clear tiers. The logic of intervention, the strategic link between inputs and goals, is set during strategic planning. Delivery of outputs sits squarely with the programme manager, who owns the actual services delivered. Achievement of outcomes, the high-level impact like reduced poverty, rests with Ministers as the political head. No more blurred lines about who answers for what.

Every programme must fit one of three types. Support Services is always called "Administration", always Programme 1, and covers HR, finance and IT. Enabling programmes handle policy, regulation and oversight. Service Delivery programmes do the frontline work the public actually sees. A programme can mix enabling and service delivery, but Administration must stay separate. Each programme needs a named manager, a clear purpose, and performance indicators. So does each subprogramme.

The guidelines are direct about the risk of running budget structures and organisational structures as two separate worlds. That creates what they call "administrative shadow-accounting", where nobody is sure who is accountable for what. The fix is alignment between the two.

From national to provincial

The same rules reach down to the provinces, but they are applied differently.

Many public services, like health and education, are concurrent functions. National departments set the policy, and provincial departments deliver it. To keep this honest, the guidelines require uniform budget programme structures across provinces in each sector. Uniformity lets Treasury compare provinces, benchmark them sector by sector, consolidate budgets, and track whether a national priority is actually being delivered in all nine provinces.

Because of this, a province cannot quietly redesign its own structure. Changes to provincial budget programme structures are a collaborative, sector-wide exercise, led by the relevant national department and signed off by National Treasury. National changes go to Treasury's Public Finance division. Provincial changes go to its Intergovernmental Relations division. And as a rule, structures should not change more than once in a five-year electoral cycle.

This is where the national rule on unfunded mandates bites hardest. When a national department hands a policy to a province or municipality without fully costing it, the lower sphere is left to deliver a promise it was never funded to keep. The new guidelines try to close that gap by making national departments cost their policies up front and align them with the fiscal framework.

What this means for you

If your work touches public money, several things change at once. Performance data is now a funding risk. Under TARS and PAM, a programme that cannot prove results is a candidate to be cut. Weak or missing performance indicators are no longer just an audit finding. They are a reason to lose your budget.

Headcount is under pressure. With compensation capped at 2026 limits, departments and entities have to manage staff numbers carefully. That affects planning, restructuring advice, and how teams are costed.

Costing must be tight. Conditional grants, transfers to entities, and shared services all have to be traceable to the right programme. Genuine overheads stay in Administration, but specialised services done for another programme must be identifiable. Sloppy cost attribution will not survive the new structure.

For practitioners with private clients, the spillover is real. Tighter spending, reprioritised baselines and closed programmes can change contract volumes and payment timelines for any business that depends on government work. Your clients will feel it before they understand it.

And there is a timing point that is easy to miss. The budget calendar is now public and the process has only just begun. The time to engage is now, not in February 2027 when the numbers are locked. CIBA has long argued that the smart move is to comment before the budget is written, not after, the same approach it took when it raised concerns directly with Treasury, as set out in 5 Key Comments From CIBA on the 2025 Tax Amendment Bill.

The practical takeaway

Do not wait for the Budget Review to react. This week, you can:

Map your programmes to the three new types and check that each has a named manager and outcome-linked indicators.

Stress-test for TARS. Be honest about which programmes look low priority or underperforming, and build the evidence to defend the ones worth keeping.

Cost every mandate before agreeing to deliver it, especially anything handed down from national to provincial or local level.

Fix your cost attribution so the full cost of each programme is clear and overheads sit where they belong.

Engage early in the open budget calendar while the numbers can still move.

The departments and professionals who treat results as the language of budgeting will keep their funding. The ones who cannot prove their value will spend the next three years explaining cuts.