2026 Tax Filing Season Changes

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

The 2026 filing season introduces several new features designed to benefit taxpayers and improve the efficiency and accuracy of the assessment process.

The Overall Direction

SARS has built the 2026 season around a simpler, more secure, and more predictable filing experience. In practice this means three things: more taxpayers are auto-assessed, more services move to self-service and WhatsApp, and more weight is placed on employer and third-party data being accurate and submitted on time. For practitioners, the work shifts. Instead of capturing returns from scratch, more of the task is checking whether the information SARS already holds is correct, and correcting it where it is not.

Auto-Assessment Now Includes Some Provisional Taxpayers

Until now, auto-assessment applied mainly to taxpayers with simple, salary-only profiles. For 2026, eligible simple provisional taxpayers will also be auto-assessed based on third-party data from employers, banks, medical schemes, and retirement funds. However, the closing date for the submission of tax returns for these provisional taxpayers remains 22 January 2027.

Changes to the ITR12 Form and Wizard

Wizard questionnaire

The form and the wizard questionnaire have been revised. Overlapping questions have been consolidated and thereby promoting clarity with regards to the following:

Disability

S10(1)(o) foreign income criteria

Non-resident

IT3(t) trust data is now prepopulated on the return

The Trust Name field has been lengthened to hold longer names. Prepopulated data still needs to be checked against the trust's own records. Unique trade numbers on the return are now locked to prevent unauthorised changes. A prepopulated identifier cannot simply be overtyped, so this should be factored into your review process.

Residency Determination

New questions and date fields have been added to classify resident status more accurately, including a field for the date a taxpayer reinstated South African tax residency. These changes mainly affect taxpayers who ceased residency, returned to South Africa, or work across borders. For these clients, correct dates are important, and the area often requires specific advice rather than straightforward data capture.

Medical Aid Selection

The ITR12 now includes a drop-down list of approved medical aid schemes, replacing free-text entry. The scheme selected must match the approved list, which supports a more accurate medical tax credit calculation.

Capital Gains Tax and Partnership Expenses

The CGT partnership questionnaire has been enhanced. Taxpayers can now declare their own portion of an asset disposal, not only for a primary residence but for other assets as well. A new own or personal expense field has been added to the local business and rental property containers. This allows taxpayers in a partnership to claim their own expenses incurred in producing a profit or loss.

Section 20A Amendment

The section 20A assessed-loss ring-fencing test now applies at a marginal rate of 39%. This is the rate at which the ring-fencing of an assessed loss may become applicable for the year of assessment. Clients with loss-making side-businesses or rental operations should be reviewed to confirm whether ring-fencing now applies.

Investment Container

Section 11G interest expenses and the section 10(1)(h) exemption are now handled at transaction level, and a Double Taxation Agreement line item has been added. Clients with foreign interest or DTA positions need this detail captured per transaction rather than as a single combined amount.

NEW: The Declaration Alert Questionnaire

The major innovation introduced for the 2026 filing season is the Declaration Alert Questionnaire. This is a new step in the process which will surprise most taxpayers. After a return is submitted and an ITA34 assessment is generated, the system may flag the return as needing more information. If it does, a short guided questionnaire is shown to the taxpayer.

The taxpayer can: complete the questionnaire immediately (at a branch), complete it later via eFiling or the SARS mobile app, decline the questionnaire, or submit a Request for Correction (RFC) instead, using the existing RFC process. The purpose is to let the taxpayer explain certain transactions in advance, so the return is less likely to be routed for administrative verification.

NB! The alert declaration functionality does not apply to auto assessment, unless a taxpayer subsequently issues an amended assessment, then the alert declaration functionality will apply to an auto assessed taxpayer.

Hypothetical examples of circumstances in which an alert questionnaire may be triggered are set out below. This list is illustrative only and should not be regarded as exhaustive.

Example: 1

A taxpayer pays the medical aid contributions on behalf of an elderly, unemployed parent and claims the applicable medical scheme fees tax credit when submitting the income tax return. SARS may not have sufficient information to verify the claim, as the medical aid statement is issued in the parent's name rather than the taxpayer's name.

However, the taxpayer is able to demonstrate that the contributions were paid from his or her own bank account. In these circumstances, an alert questionnaire may be triggered, allowing the taxpayer to explain the transaction and submit supporting documentation at an early stage of the assessment process.

By providing the explanation and supporting evidence upfront, the taxpayer may avoid the need for a subsequent verification or audit relating to the transaction.

Example 2

When submitting a tax return, a taxpayer indicates that he or she has sixteen medical aid dependants during the current year of assessment. The eFiling system may flag this as a potential anomaly because, in the previous year of assessment, the taxpayer reported only six dependants.

In reality, the discrepancy may simply be the result of a data-capturing or typing error. An alert questionnaire may therefore be triggered, providing the taxpayer with an opportunity to explain the discrepancy and confirm that the incorrect number of dependants was entered inadvertently.

By allowing the taxpayer to clarify the issue immediately, the assessment process can proceed more efficiently and the need for a subsequent verification or audit may be avoided.

Note well: Not all transaction will trigger an alert questionnaire. The SARS AI system will automatically identify which transactions requires clarity.

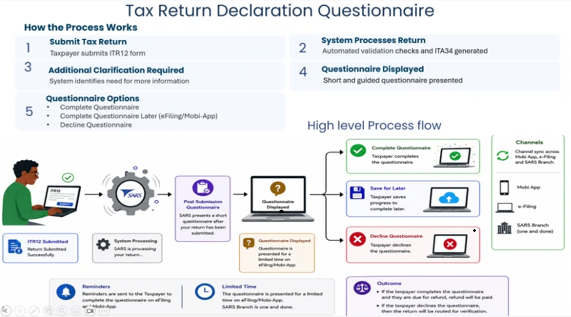

Below is a diagram which explains how it works:

The taxpayer submit a tax return on efiling

The system processes the return and generates and ITA34

At this stage if the system identifies an irregular transaction

Questionnaire is displayed

The taxpayer will have three options in relations to the alert questionnaire

Complete the questionnaire

Complete the questionnaire later ( eFiling / Mobi- App)

Decline the questionnaire.

If the taxpayer completes the questionnaire and they are due for a refund, refund will be paid.

If the taxpayer declines the questionnaire, then the return will be subject to verification

Digital Channel Updates

Several changes affect how taxpayers receive documents and interact with SARS. ITA34s for auto-assessed taxpayers without email or eFiling can now be sent via WhatsApp. Non-provisional and provisional taxpayers can request their ITA34 and Statement of Account on WhatsApp, and all taxpayers can upload supporting documents through the channel. ITA34s issued through WhatsApp and Kiosk channels are now encrypted and password-protected to protect taxpayer confidentiality. On eFiling: contact details can be updated before login, ITA34 quick links have been added to the landing page, and the return-overdue message now displays correctly on the income tax return page.

Key Deadlines

The official 2026 filing deadlines are:

Non-provisional individual taxpayers: 23 October 2026.

Provisional taxpayers: 22 January 2027.

Trusts: 22 January 2027.

Companies, approved public benefit organisations, and approved recreational clubs: within 12 months of their financial year-end.

The full list of who must file and who is exempt is set out in Filing Season 2026: SARS Has Set the Dates.

You can download the sample version of a 2026 ITR12 return here.