PAYE and VAT Registration Issues, What You Need to Know and Do

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

Your client needs a VAT number. You submit the application, upload the documents, and wait. Three weeks later: rejected. No clear reason. Now you're starting over, your client is furious, and you still don't know exactly what went wrong.

This is not a rare story. In this article we look at the exact mistakes that are causing the most delays and rejections. The problems are consistent and avoidable. And they are costing practitioners real time, real clients, and real money.

In today’s SARS regional meeting the main issues highlighted by SARS are discussed below.

The fraud problem that changed everything

SARS did not introduce biometrics and desk reviews to frustrate practitioners. It introduced them because fraudulent VAT and PAYE registrations had reached a level where the entire system was being abused. Fake VAT numbers led to fraudulent input tax claims. Fraudulent PAYE registrations enabled the creation of false IRP5 files, which were then used to generate fake personal income tax refunds.

The modernised process is SARS's answer to that problem. And as covered in Accounting Weekly's earlier piece on VAT fraud and the push to clamp down on suspicious registrations, the burden of these controls falls heavily on legitimate practitioners, even though they are not the problem. That is frustrating, but it is the reality. The good news is that SARS itself confirmed at the KZN meeting: a properly prepared application, with the right documents and an accurate RAV01, should not require any back-and-forth at all.

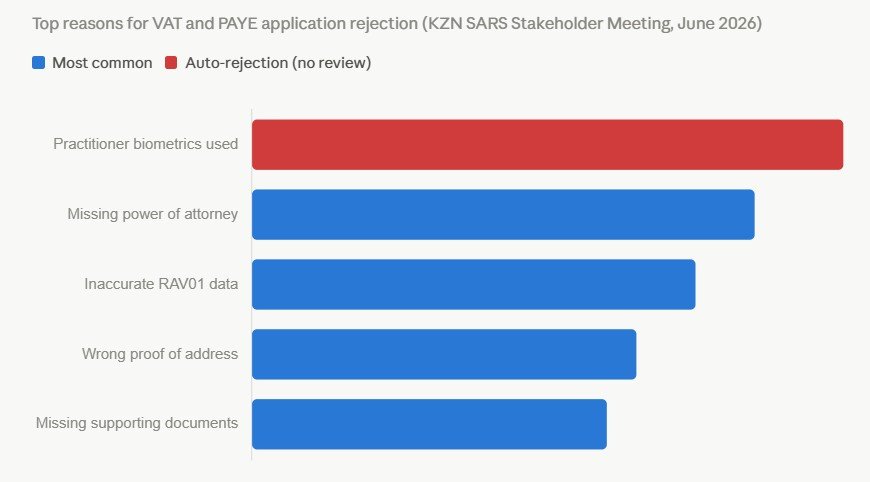

The biometrics mistake that means automatic rejection

This is the one that stings the most, because practitioners who make this mistake never get a chance to fix it.

SARS requires the taxpayer, or registered representative, to complete their own facial biometric verification. Not the practitioner. The practitioner submits the application on their own eFiling profile, the system sends an approval request to the taxpayer, and the taxpayer completes their own biometric on their personal eFiling or the SARS MobiApp.

When a practitioner does the biometric using their own face, the application is rejected outright. These applications are rejected outright without further engagement and the application has to be restarted. The application must be restarted from zero.

As explained in our earlier article, when SARS first introduced biometric facial ID checks for VAT and PAYE, this process is designed to authenticate the actual taxpayer, not the person acting on their behalf. Before you submit any registration application, your client must be registered on eFiling or the SARS MobiApp and be ready to complete their own biometric step. If they are not ready, do not submit yet.

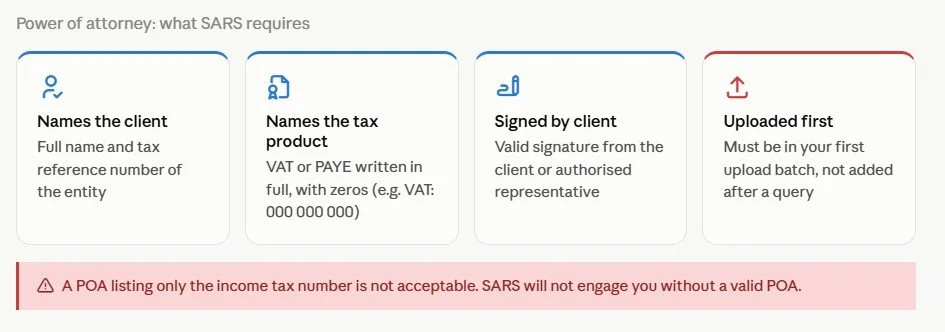

The power of attorney: your entry ticket

SARS is not obligated to engage you if there is no valid power of attorney on file. That is not a warning, it is their stated position. Yet a significant number of applications arrive without one, or with one that does not meet the requirements.

The POA must specifically authorise the relevant tax product (VAT or PAYE registration) as required by SARS. A POA that only refers to the entity's income tax number is not sufficient. A POA that only references the income tax number of the entity is not acceptable for a VAT or PAYE registration. Upload it with your very first batch of documents, not as an afterthought when SARS asks for it.

The RAV01 is a desk review, not a form

SARS processes these applications without sitting across from you. The RAV01 and your supporting documents are the only things they have to work with. If the two do not match, the application is flagged.

The most common RAV01 errors SARS highlighted are:

Business activities selected too broadly. Saying a company does "other business services" when the contracts clearly show it is a construction firm is a red flag. Select activities that actually reflect what the client does.

Turnover figures that do not make sense. SARS expects turnover to be reflected on an annualised basis so that it can determine whether the application falls within the compulsory or voluntary VAT registration rules. Where a business has only traded for part of a year, ensure the turnover disclosed accurately reflects the annualised position and is supported by the accompanying documentation. If SARS cannot tell from your RAV01 whether the registration is compulsory or voluntary, they will stop and ask, and that takes time.

The liability date is today's date. SARS sees this on application after application. The liability date must reflect when the entity actually became liable, not when you sat down to complete the form. For PAYE, there is currently no limit on how far back you can backdate. For compulsory VAT, eFiling allows up to six months of backdating, and SARS can consider further backdating after the number is issued if the evidence supports it.

Profile details that do not match the documents. If the entity's address on the SARS profile is different from the proof of address you upload, SARS will flag it. Update the profile before you submit the application.

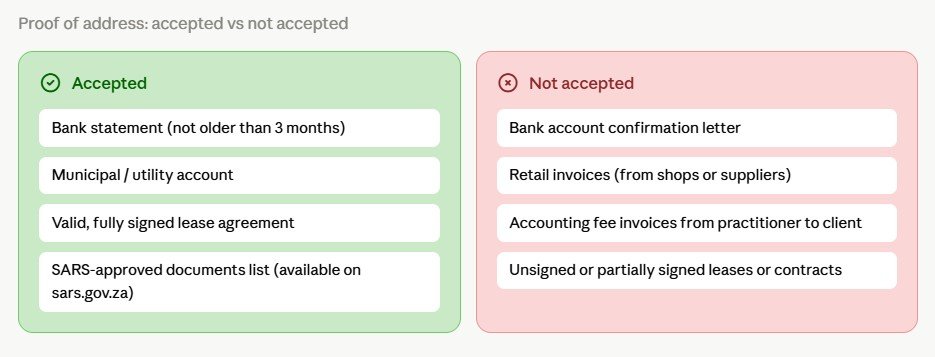

Documents that are not what you think they are

Some of the rejection causes here surprised practitioners at the meeting. SARS was direct about them.

Retail invoices are not FICA documents. Accounting fee invoices issued by the practitioner to the client are not FICA documents. Bank account confirmation letters are not proof of address. A bank statement that is not older than three months, a utility account, or a valid lease agreement, those are acceptable.

For VAT, include bank statements even if the upload letter does not specifically request them. SARS explained that bank statements are used during the desk review as supporting evidence of an ongoing enterprise and should be read together with invoices and contracts, not as standalone proof of turnover. SARS uses bank statements during the desk review as evidence of ongoing trade. They will look for deposits that correlate to the invoices and contracts you submitted. A bank statement submitted in isolation as proof of turnover is not accepted either. It needs to be read alongside invoices and contracts.

For PAYE, payslips or employment contracts are required. A payroll schedule of names and salary figures without the underlying payslips or contracts will not be accepted. If your client hired staff in the last two to four weeks and payslips are not yet available, submit the employment contracts. SARS confirmed at the meeting that contracts are an acceptable substitute. If an application is rejected because contracts were submitted and payslips were not, escalate to your branch stakeholder liaison.

This connects directly to a point made in our guide on the actions and consequences of late VAT registration, which outlines how important it is to ensure both registration timing and documentation are correct from the start. Getting it right the first time saves your client from backdated VAT assessments, interest, and penalties.

When SARS tries to call and nobody answers

This one is costing practitioners applications they did not expect to lose. SARS tries to contact the practitioner or taxpayer up to three times. If they cannot get through, the application can be auto-rejected. SARS numbers can be flagged as spam on some mobile networks. SARS advised that officials generally make up to three attempts to contact the taxpayer or practitioner. If they are unable to make contact, the application may be rejected.

The solution is straightforward: write a brief explanation letter and include it with your first upload. Introduce the client, explain the business, describe the reason for registration, and flag anything unusual about the circumstances. If SARS can understand the application from the documents alone, they do not need to call. The calls happen when the picture is incomplete.

Also tell your clients to expect a call from SARS. Ask them to save the SARS contact centre number so it does not come through as an unknown caller. CIBA has formally recommended to SARS, through the RCB Forum, that telephonic contact should always be followed up by an electronic notification. That recommendation has been noted but is not yet standard practice. Until it is, the explanation letter is your best protection.

What to do when you need to escalate

If an application is genuinely stuck or has been rejected without a clear reason, use the appropriate stakeholder escalation process or engage your branch stakeholder liaison. Include all supporting documents, every case reference number, and a record of all prior interactions, calls, emails, and branch visits.

For PAYE cases where the upload link on eFiling cannot be reopened (PAYE modernisation is still in progress), use the SARS Online Query system to upload additional documents. Navigate using the entity's income tax credentials. There is no PAYE number yet, so that is the only way in.

For cases where the same application is being handled differently by different branches, for example companies where the trading address differs from the CIPC registered address, document the inconsistency and escalate through your local stakeholder liaison. SARS acknowledged at the meeting that this appears to be an internal inconsistency, not a policy requirement, and has asked practitioners to flag these cases so the specific offices can be identified.

What this means for your practice

Every rejected application is unbillable rework. Every delayed registration puts your client's business at risk, and puts your relationship with that client under pressure. The practitioners who are getting registrations approved first time are the ones who treat the RAV01 as a desk review document, not a form to fill in quickly, who prepare their clients for the biometric step before submitting, and who include enough supporting documentation that SARS does not need to ask follow-up questions.

That level of preparation is also a billable service. Clients who have had bad experiences elsewhere will pay for a practitioner who knows how to get this right without the drama. Getting your applications right now is how you demonstrate that you are one of them.

Your practical takeaway

Before you submit your next VAT or PAYE application, run through these four checks:

Is your client registered on eFiling and ready to complete their own biometric? If not, do not submit yet.

Does the POA name the specific tax product with zeros? If not, fix it before uploading.

Does the RAV01 turnover figure match the bank statements and contracts, with the correct liability date? If not, revise the RAV01.

Have you included an explanation letter giving SARS the full picture of the client's business? If not, write one. Two paragraphs is enough.

Those four checks will eliminate the majority of rejections before they happen.

Join CIBA and enjoy free tax webinars. For more go go the cpd@myciba.org website and browse the tax webinar selection here.

Trending