Cash and Connections: Two Gaps Closing Your Clients’ Doors

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

Published in CIBA / SACCI Business Development, keeping you informed of broader business, economic and SME developments through CIBA’s strategic partnership with the South African Chamber of Commerce and Industry (SACCI).

More than half of South Africa’s small businesses are in distress, and most have less than a year of cash. SACCI’s two newest small business guides take on the two problems behind that number: cash and connection. Here is what the data shows, what the world’s best-run economies do about it, and the part you play.

Key Takeaways

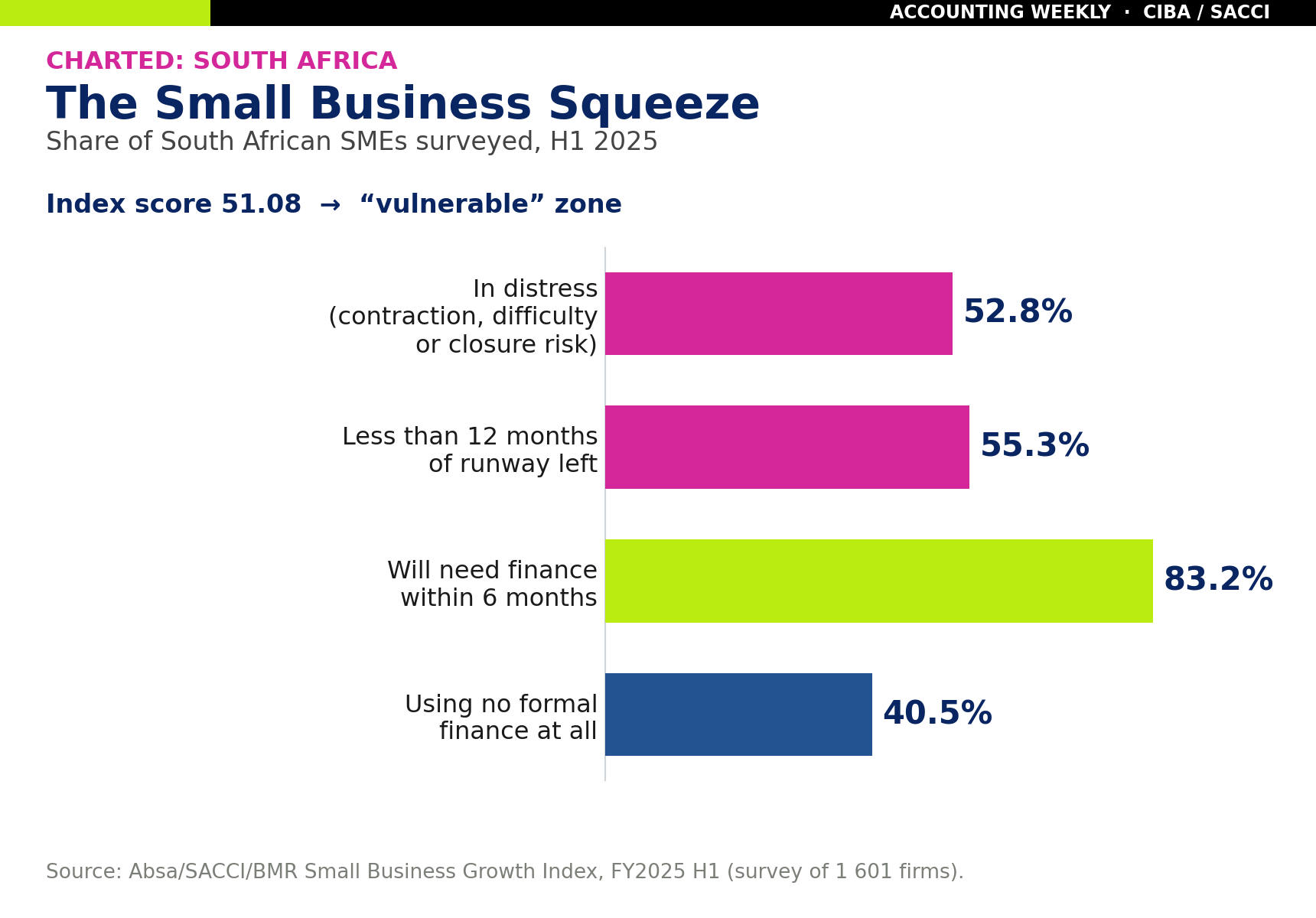

52.8% of South African SMEs are in distress, and 55.3% are looking at a risk of closure if no support mechanisms are implemented.

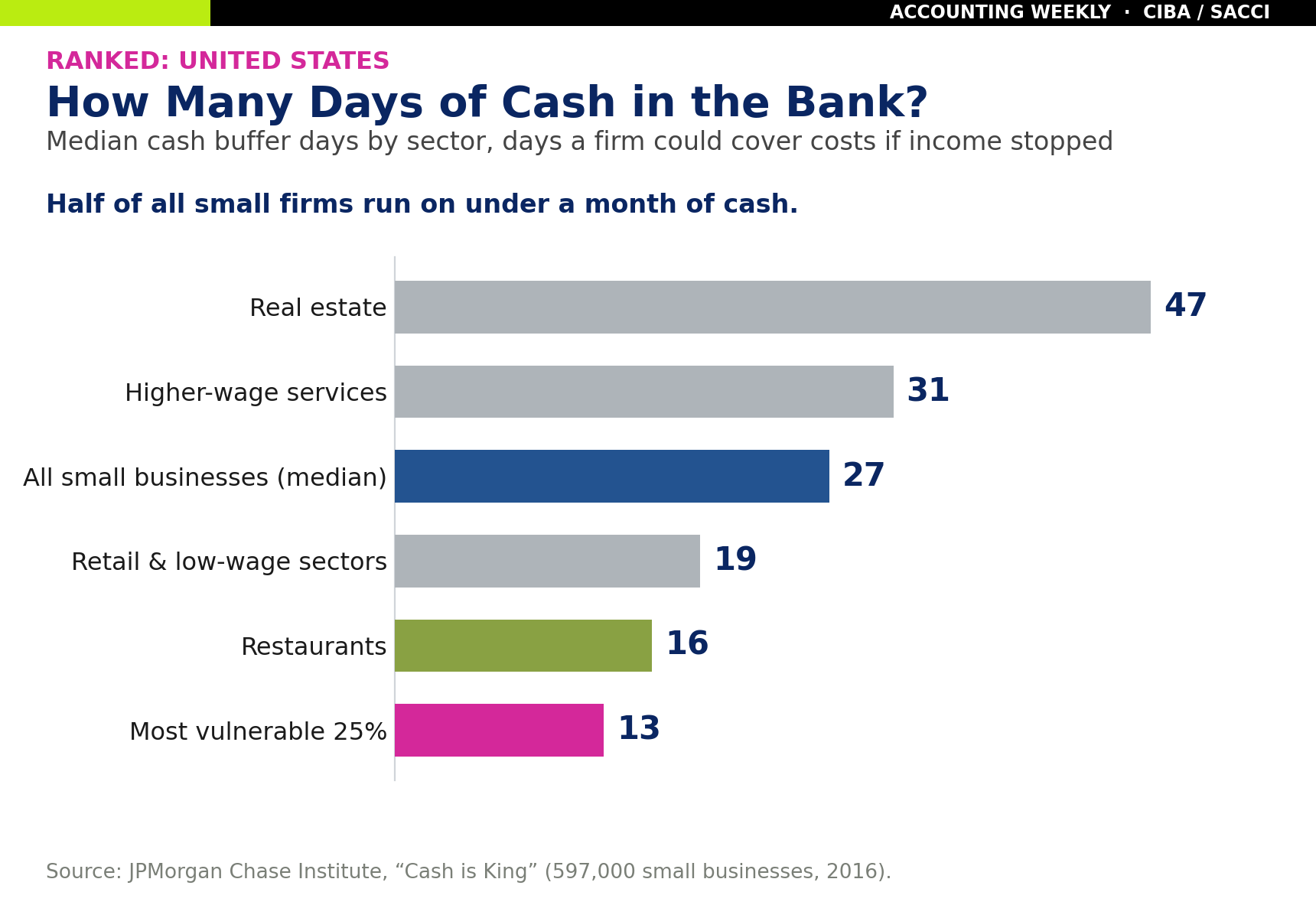

Worldwide, the median small business holds just 27 days of cash. This is a global condition, not only a local one.

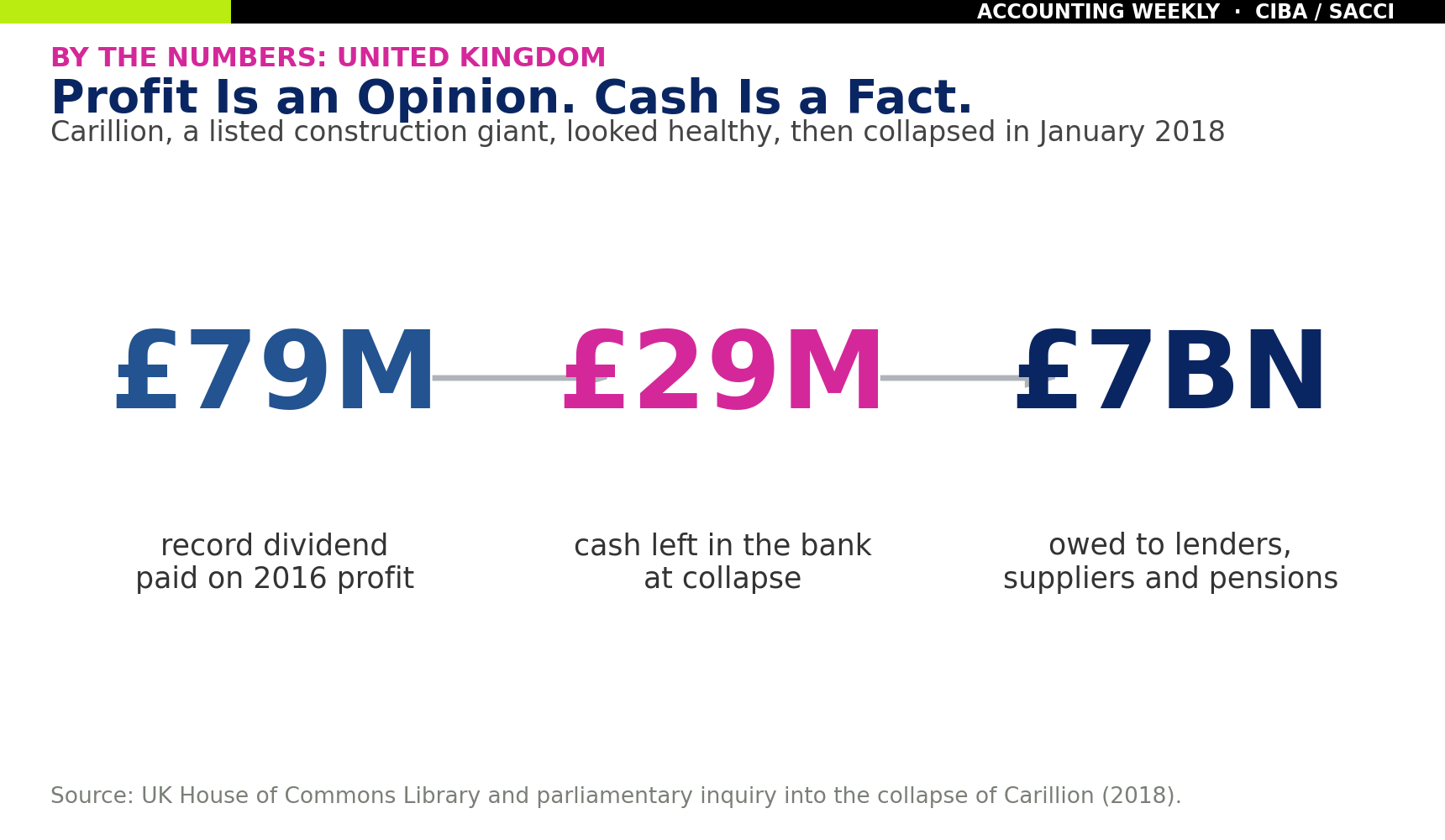

Profit is an opinion, cash is a fact: a profitable-looking UK giant collapsed with almost no cash in the bank.

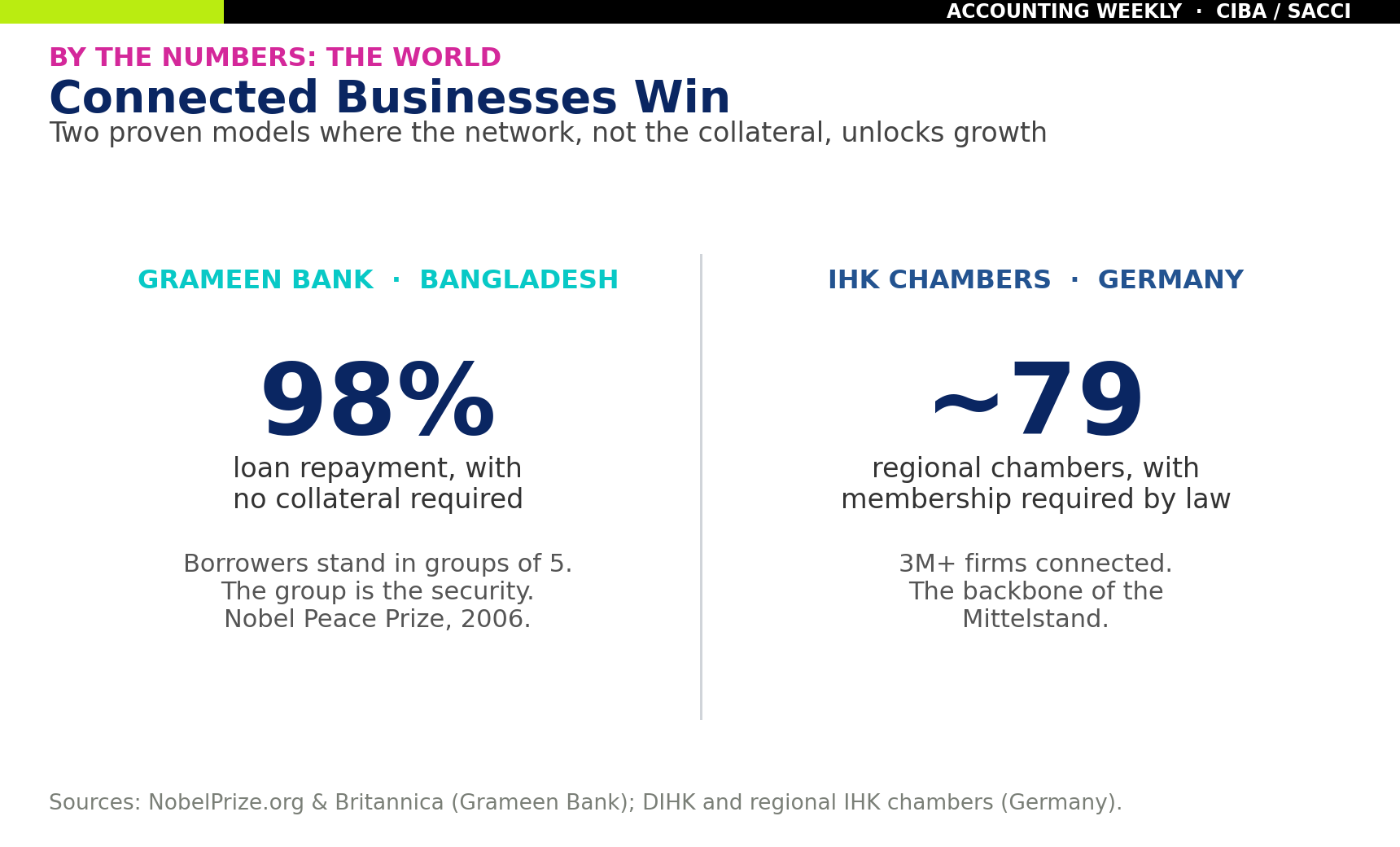

Connection beats collateral: from Bangladesh to Germany, networked businesses get finance and survive longer.

If you have a client who looks profitable on paper but cannot make payroll, or one who runs the whole business alone with nobody to call, this is for your next meeting. The charts below are built to forward, screenshot, and put in front of a client who needs to see the picture, not just hear it.

The squeeze - Volume 1: Strengthening Cash Flow to Fuel Small Business Growth.

The H1 2025 Small Business Growth Index scored the sector at 51.08, inside the “vulnerable” zone. More than half of SMEs are in contraction, difficulty or at risk of closure. A majority have under a year of runway. And while most will need finance within six months, four in ten use no formal finance at all.

The global benchmark: cash is king

When your client says they have a year or less, they are not unusual. They are the global norm. The Profit mask, cash face. A business owner holding up a smiling "profit" mask on a stick, while the real face behind it looks worried and the wallet is empty. It captures "profit can lie" and the Carillion idea in one cheeky image, and works as a strong scroll-stopper for the LinkedIn post.PMorgan Chase Institute studied 470 million transactions from 597,000 American small businesses and found the median firm held just 27 days of cash. The most vulnerable quarter held 13 days or fewer. A 13-week cash flow forecast is how you give an owner sight of the cliff before they reach it.

When profit lies

Profit and cash are not the same thing, and the gap between them is where businesses die. As covered in When Profit Lies and Cash Tells the Truth, a profitable business can still run dry. The UK construction group Carillion is the clearest warning. It reported solid profits and paid a record dividend, then collapsed months later with almost nothing in the bank. If it can kill a listed giant, it can kill a client on a thin margin.

The other half of survival: connection - Volume 4: Building Networks and Reducing Isolation.

An isolated owner makes worse decisions and struggles to raise money. A connected one finds buyers, suppliers and finance. The world’s most successful models prove it. In Bangladesh, Grameen Bank lent to groups of five with no collateral and still hit near 98% repayment. In Germany, almost every firm belongs to a chamber by law, and that network underpins the Mittelstand. Connection is a form of collateral.

Who it’s for

Almost every owner-managed client under 50 staff. The index points straight at the most exposed, so these are the clients to picture:

Sole proprietors and single-owner clients. They are the largest and most fragile group in the survey, scoring lowest on the index, with no partner or team to share the load.

Clients turning over under R1 million. They make up the bulk of the sector and carry the thinnest buffers against a shock.

Anyone running on weak or critical cashflow, which is nearly two-thirds of all small firms, and is common in retail, hospitality and personal services.

Construction and manufacturing clients waiting 60 or 90 days to be paid while wages fall due now.

Township and rural clients, and those in the Northern Cape, North West and Limpopo, the lowest-scoring regions and often outside the formal credit system.

Any solo founder deciding everything alone. That isolation is exactly what Volume 4 addresses.

What you should do

Forward both guides. Then go further.

Build a 13-week cash flow forecast. Move the client off the bank balance and onto a forward view. For a stressed owner, this is the single most useful thing you can hand them. Bill for it as advisory work.

Separate profit from cash. Show the client where the money leaks: pricing, payment terms, stock sitting too long. Profit can flatter a business that is quietly running out of money.

Get them finance-ready before they need it. With 83.2% needing capital soon and 40.5% outside the formal system, prepare the management accounts, forecasts and a clean funding pack now. You are often the reason an application gets approved.

Tighten the working capital cycle. Invoice faster, chase debtors, renegotiate supplier terms. Small timing wins free up real cash with no new borrowing.

Plug them into a network. Point clients to SACCI and their local chamber. An isolated owner makes worse calls. A connected one finds buyers, suppliers and funding leads.

Be their thinking partner. Volume 4’s real point is that owners should not decide alone. That standing relationship is advisory work, and it is what keeps the client.

The bigger picture

Cash and connection are two sides of survival. A client with no cash forecast trades blind. A client with no network trades alone. You give them sight and you give them company. Every SME that stays open because its accountant saw the cash crunch coming is a job kept, a tax base widened, and a small piece of GDP defended. This is what business development looks like at ground level.

For your client: Download SACCI’s Small Tips 4 Small Business Volume 1 (Strengthening Cash Flow) and Volume 4 (Building Networks and Reducing Isolation) from the SACCI Small Business Growth Index page. Direct any SACCI partnership queries to Tshidi Ndebele at the South African Chamber of Commerce and Industry.

Not a CIBA member? Join CIBA and get access to the SACCI business-development feed and the practical advisory tools that turn cash flow forecasting and funding readiness into fee-earning work for your SME clients.

👉 Click here: https://myciba.org/apply-for-membership

This update was shared with CIBA by Tshidi Ndebele of the South African Chamber of Commerce and Industry. Through CIBA’s strategic partnership with SACCI, members receive ongoing updates on business, economic and SME-relevant developments, positioning CIBA as the strategic conduit between national business policy and the accountants who serve South Africa’s SMEs

Trending