New SARB Rules Are Coming for Cross-Border Payments

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

If you have a client selling to offshore customers, or using a platform that collects payments from South Africa for an overseas merchant, this one is worth a closer read. The South African Reserve Bank (SARB) is moving to regulate cross-border payment facilitators, and the comment window closes soon.

What is happening

The SARB has noticed a rise in cross-border payment facilitator activity. In these setups, payment transactions are aggregated and acquired in South Africa for offshore merchants selling goods or services, including digital products. These facilitators are not acquirers themselves. They operate under sponsorship arrangements with authorised domestic acquirers, but right now they sit outside any formal regulation in South Africa.

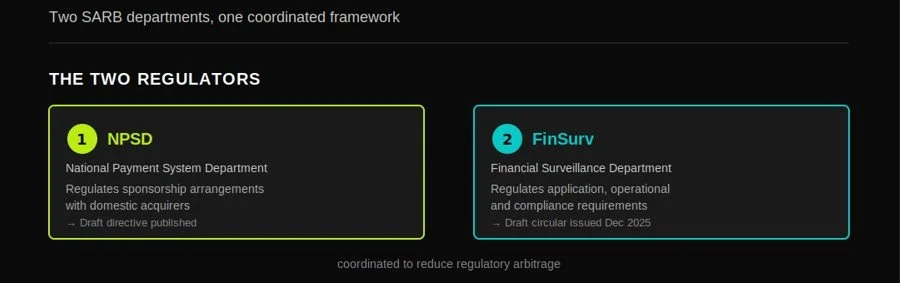

That is about to change. The SARB's National Payment System Department (NPSD) and Financial Surveillance Department (FinSurv) are building a coordinated regulatory approach. Payment facilitators will need to meet the NPSD's requirements because of their sponsorship arrangements, and they will also need to meet FinSurv's application, operational and compliance requirements. The goal is consistency across both departments, and less room for regulatory arbitrage. More specifically, the NPSD directive governs the payments side (who can acquire and process payments domestically). The FinSurv circular governs the foreign exchange side (how money legally leaves the country). A payment facilitator caught up in this needs to satisfy both at once, since the same business model touches both departments. That's exactly why SARB called this a coordinated approach.

In December 2025, FinSurv issued a draft circular for public comment on Authorised Dealer and payment facilitator responsibilities, cross-border settlement and reporting. That review is still underway. Now the NPSD has published its own draft directive, covering the issuing and acquiring of payments for goods and services from offshore merchants. The two documents will be finalised and published together once the process is complete.

Who it is for

If your client runs an e-commerce business that sells internationally, uses a payment aggregator to collect funds from local customers on behalf of a foreign supplier, or operates any kind of digital marketplace with cross-border money flows, this directly affects them. It also matters for clients in fintech, payments infrastructure, and any business sponsoring acquiring arrangements for offshore-linked merchants.

What you should do

Read through the draft NPSD directive and note how it could affect any client using or operating a payment facilitator model. Flag the closing date for comments, which is 17 July 2026. If you or a client wants to make a submission, comments must address the NPSD directive only, not the FinSurv circular, even though the NPSD references the FinSurv framework for context. Start the conversation with affected clients now, since regulatory change in payments tends to bring new reporting and compliance obligations once finalised. You do not want to do it alone? Send your comments to technical@myciba.org before 10 July 2026 and we will consider your inputs in our submission.

The two source documents are available here:

The NPSD draft directive is SARB's plan for who is allowed to handle payments inside South Africa, and how.

The problem it's fixing: SARB noticed that some payments for things happening entirely inside South Africa, like a local Uber ride or a local hotel booking, were being processed as if they were foreign transactions. This let businesses dodge local oversight and sometimes stick customers with international transaction fees for something that never left the country. SARB wants that stopped.

The new model it's allowing: Cross-border payment facilitators (the businesses collecting payments here for offshore sellers) can keep operating, but only through a formal sponsorship deal with a registered South African acquirer (usually a bank). The facilitator can't act alone. It always sits underneath a sponsoring acquirer who carries the legal responsibility.

What sponsoring acquirers must now do:

Apply to SARB in writing before sponsoring any facilitator, and hand over a full description of the business model, money flow, and risks.

Take full legal responsibility for everything the facilitator does, including compliance failures.

Keep merchant money strictly separate from the facilitator's own money, held in a segregated South African bank account, with no interest paid to merchants on those balances.

Give SARB any information about the facilitator within 24 hours of being asked.

Report numbers to SARB twice a year (January and July), including how many facilitators and merchants they're sponsoring and the transaction values involved.

Put real consumer protections in place, such as clear fee disclosure, exchange rate transparency, and proper complaint handling.

The bigger goal: Make sure SARB always knows who's really moving money through the system, and stop facilitators from being used to dodge anti-money-laundering or exchange control checks.

2. Draft Exchange Control Circular: Cross-border retail e-commerce regulatory framework

This is the companion piece, focused on the foreign exchange side rather than the payment system side.

It applies to a slightly different but overlapping business model: payment aggregators that collect small, frequent payments from South African individuals (think monthly subscriptions or small import purchases) and bundle them into one bulk payment sent offshore to the foreign merchant, via a bank that's an Authorised Dealer.

Key rules it introduces:

A hard cap of R50,000 per transaction, and splitting a bigger transaction to dodge that cap is explicitly banned.

The aggregator must be a registered South African company, formally contracted with the bank and the foreign merchant.

The bank, not the aggregator, sets the exchange rate and is legally the one settling the foreign exchange transaction.

The aggregator must collect and verify personal details (ID number, address, etc.) for every individual making a payment, and hand that information to the bank for reporting.

The aggregator is barred from buying or selling foreign currency itself, or holding foreign currency at all. That stays with the bank.

FinSurv can inspect the bank or the aggregator at any time to check compliance.

This builds on other recent shifts in cross-border regulation. CIBA's earlier coverage of the [removal of interest rate caps on cross-border related-party loans] showed how SARB is steadily tightening oversight of money moving across South Africa's borders. The same logic applies here. As cross-border digital commerce grows, so does the SARB's interest in tracking and regulating how the money flows.

The bigger picture

Every client you help navigate a new regulatory framework is a client who stays compliant, avoids penalties, and keeps trading with confidence. That is what business development looks like at ground level. When South Africa gets cross-border payment oversight right, it protects the country's foreign exchange position and keeps the door open for SMEs trading internationally.

Trending