The Client You Keep Is the Risk You Own

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

It is 9pm on a Tuesday. You are staring at a WhatsApp message from a client asking you to "just adjust the figures a little." Again.

You know what the right answer is. You also know you have not sent it yet.

There is a client on your books right now who is costing you more than their monthly fee. Not in time. Not in admin. In something far harder to recover: your professional standing, your FIC compliance, and your PI cover.

The longer you keep them, the deeper the exposure.

Most accountants know when a client relationship has gone wrong. What they do not know is what the law actually requires them to do about it. The answer is sharper than most people expect.

When "Difficult" Becomes a Legal Problem

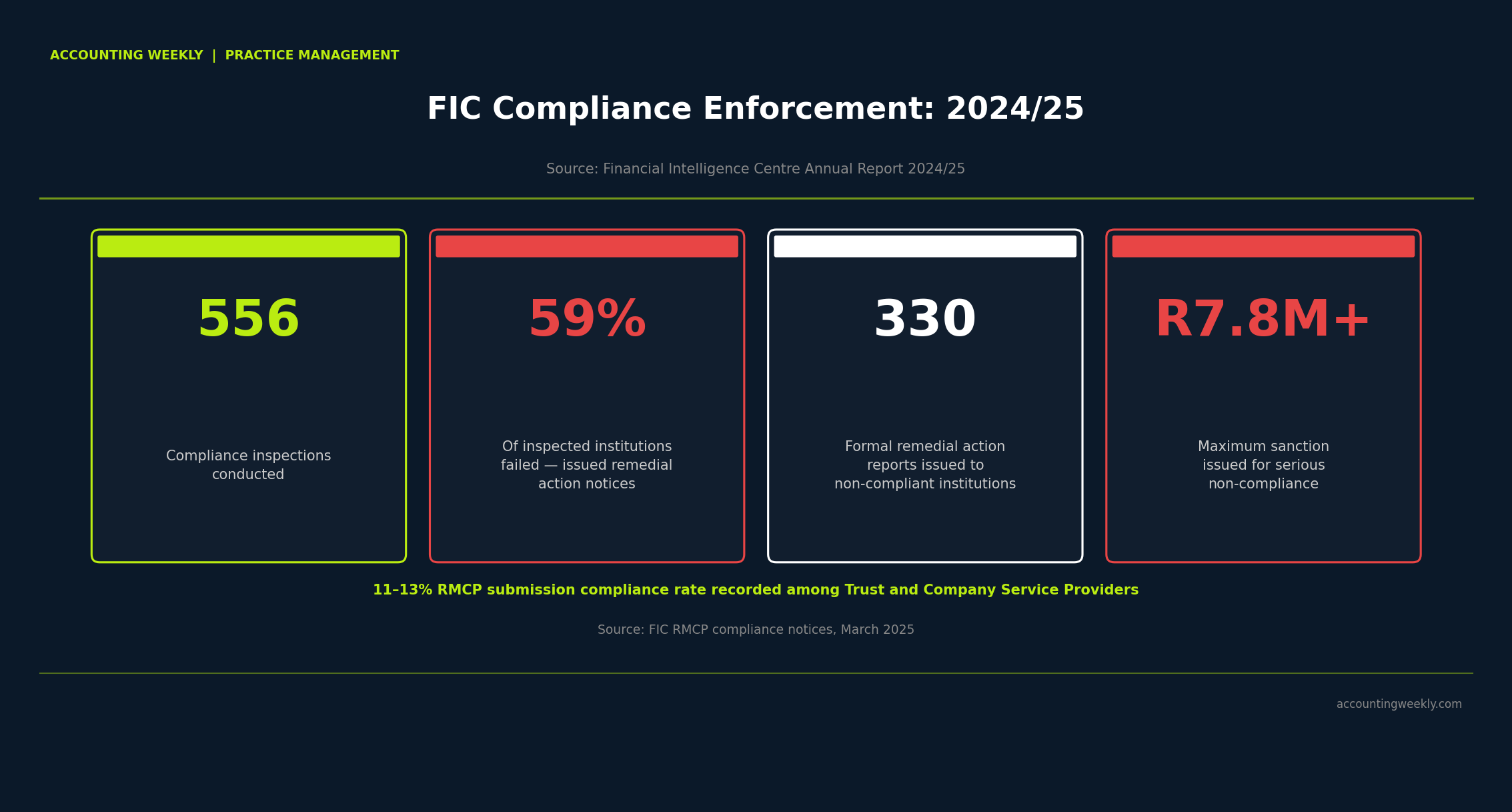

Let us start with the FIC Act, because this is where most practitioners have the most immediate exposure.

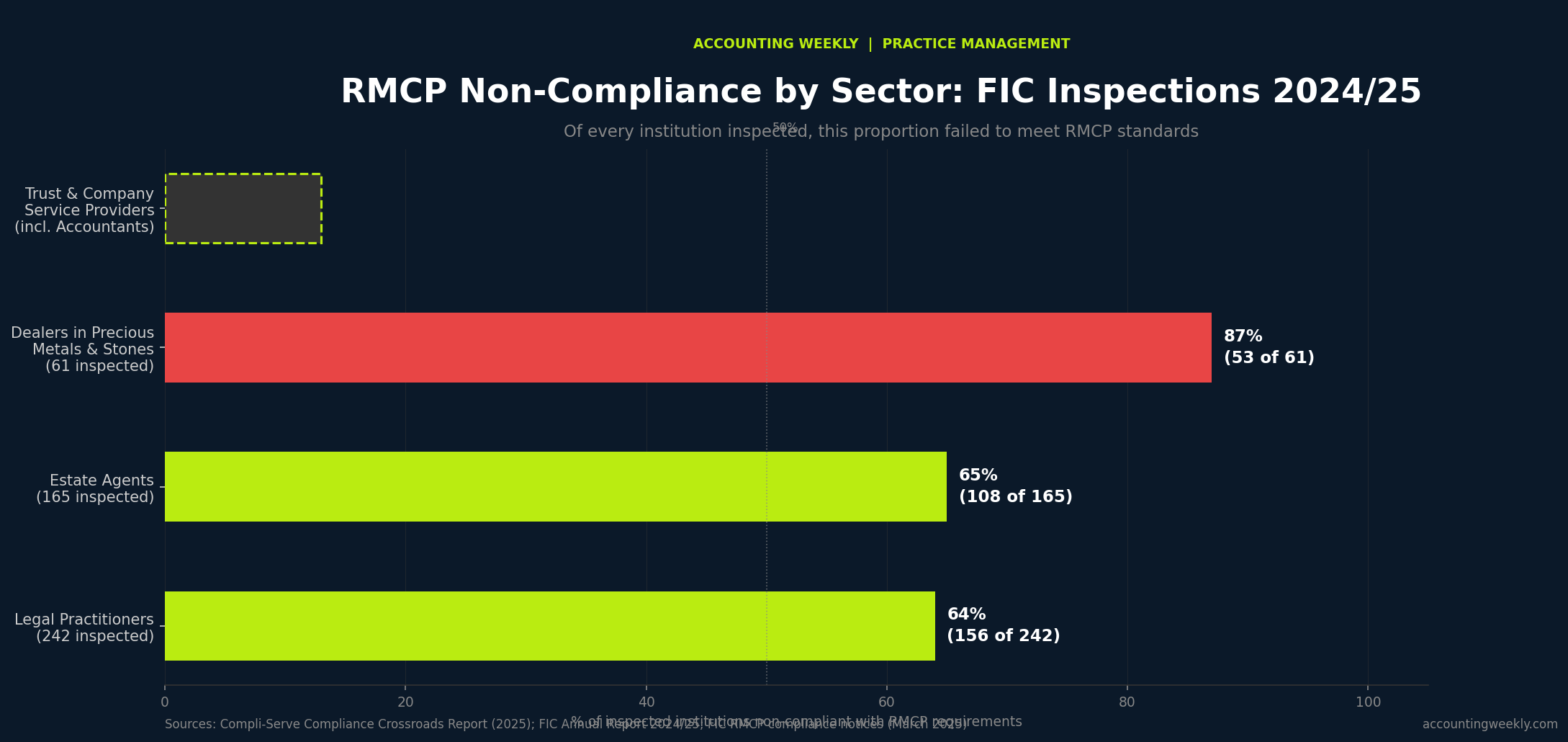

If your practice offers trust and company services, you are most likely an accountable institution. If you are an accountable institution, it means that every client on your books must be identified, verified, risk-rated, and monitored on an ongoing basis. Not once at onboarding. Ongoing.

As the AW breakdown of what FIC compliance actually requires after registration makes clear: Compliance does not end when you receive your registration confirmation. It starts there. Every client, every transaction, every day.

Now consider your FICA ghost. The client whose certified ID you have asked for three times. Whose beneficial ownership structure you cannot explain. Who responds to compliance requests with "I'll sort it out." That client is not just an admin headache. They are an open gap in your Risk Management and Compliance Programme. The FIC does not accept "the client was uncooperative" as a defence. They inspect your systems. If the gap is there, the gap is yours.

The FIC's Draft Directive 11 signals exactly where this is heading: Away from "show us your document" and toward "show us your data." The firms that kept non-compliant clients on the books for convenience are the ones that will have the hardest conversations when that reporting period arrives.

Three Clients That Must Go

Not every difficult client creates legal risk. But three categories create exposure no fee justifies.

The FICA ghost. Incomplete identity verification. Opaque ownership. Consistent non-response to compliance requests. You cannot build a compliant RMCP around a client who will not cooperate with it. Every month you keep them, you extend a documented breach.

The pressure merchant. This is the 9pm WhatsApp client. The one who asks you to adjust figures, omit a disclosure, or sign something you should not sign. As AW's piece on the ethics mistakes that quietly cost accountants explains: When a client sees you are willing to bend once, the professional boundary shifts permanently. The requests become more frequent. When things go wrong, they distance themselves from the decision. You carry the risk. They walk.

The chronic non-payer. This is more than a cash flow problem. A client who withholds payment as leverage, disputes invoices without basis, or pays three months late, is also creating professional risk. Fee disputes almost always pull work quality into the frame. An overdue fee file is a litigation file in waiting. And a client you resent is a client whose work you are not doing at your best. The construction sector sole proprietor who pays when he feels like it, or the retail trader who says "I'll sort you out at year-end," is not a client. They are a liability with a trading name.

The Exit That Protects You

Walking away is a professional act. Doing it badly is a professional risk.

Step 1: Go back to the engagement letter. Your engagement letter governs termination. Check the notice period, the conditions, and what happens to work in progress. If you have no engagement letter (which is never recommended as it leaves you exposed), you are ending a common law contract of mandate. The client is entitled to reasonable notice and access to their records.

Step 2: Document your reasons internally. You do not owe the client a detailed explanation. You owe yourself a clear internal record. Dates of FICA requests. Description of pressure applied. Your refusal and why. This record protects you if the client later reframes the exit as negligence on your part.

Step 3: Write a clean termination letter. Short, professional, and factual. You are withdrawing from the engagement with effect from a specified date. The client must make alternative arrangements. Outstanding work and fees are addressed. No debate. No apology. No drama.

Step 4: Return the records. The client owns their records. You keep copies for your own professional purposes. You do not withhold originals to leverage unpaid fees. That creates a separate dispute, and it creates the impression that you have something to hide.

Step 5: Consider your STR obligations. This is the step most accountants do not know about. If the reason for termination involves transactions that may trigger a reporting obligation under the FIC Act, the termination does not relieve you of that duty. A Suspicious Transaction Report may still need to be filed via goAML. Tipping off the client about that filing is itself an offence. If you are unsure whether a filing is required, get guidance before you send the termination letter. The RMCP guidance on your reporting obligations covers the framework. Apply it.

What Firing the Right Client Actually Does

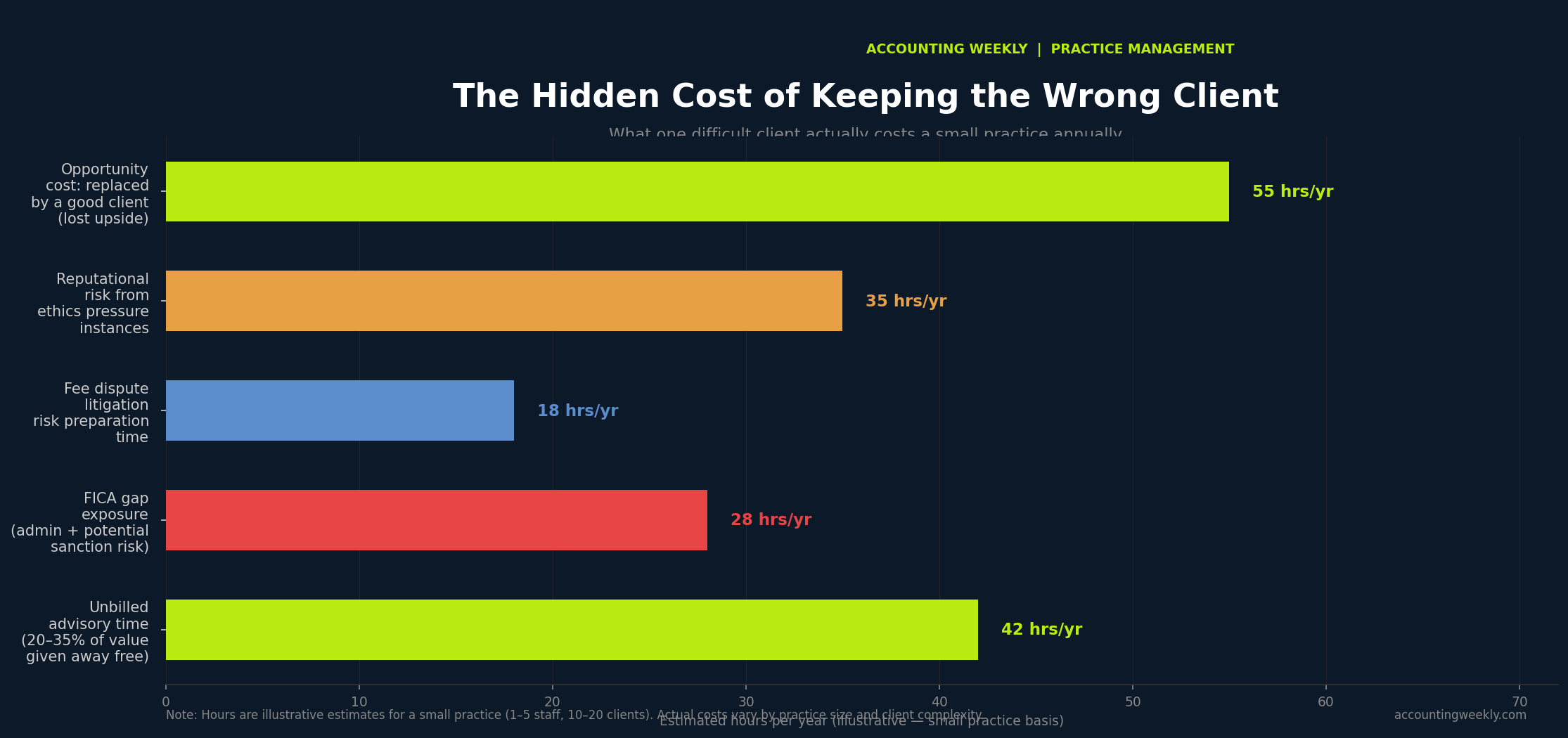

A bad client has a hidden cost most practices never calculate. Consider the construction SME client who pays late, pushes back on every invoice, and asks you to misrepresent certified claims. The direct fee might be R3 500 a month. The hidden cost is six hours of resentful admin, a FICA file with gaps, two WhatsApp conversations that put your professional judgment in writing, and the creeping risk that one of those conversations ends up in front of a disciplinary committee.

Fire that client. Replace them with one who pays on time, cooperates with FICA, and trusts your advice.

Your RMCP will be cleaner. Your PI insurer will be happier. Your practice will be worth more.

And at 9pm on a Tuesday, you will not be staring at a WhatsApp message wondering whether this is the one that ends your career.

Practical Exit Checklist

Before you send the termination letter, confirm:

Your engagement letter has been reviewed for notice and termination terms

Your internal record documents the specific grounds (FICA gap, pressure applied, non-payment history)

The termination letter is professional, factual, and short

Work in progress is noted and the client is given adequate time to transition

Client records are ready to be returned or transferred

STR obligations have been assessed and acted on if required

Your RMCP is updated to reflect the client's removal from your active book

👉 Join CIBA and we'll show you how to build a practice where the clients you keep make you grow, and the clients you lose no longer cost you.

Further Reading

When Should an Accounting and Tax Practitioner Walk Away From a Client? — Practical indicators that signal it is time to disengage, with guidance on exit steps

The Ethics Mistakes That Quietly Cost Accountants Clients, Fees, and Their Reputation — How small ethical compromises shift the balance of power in a client relationship, and why they always end badly for the accountant

FIC Compliance After Registration: What You Should Know — Why registration is just the start, and what your ongoing FICA obligations are for every client on your books

Accounting Practices as Accountable Institutions: Building an RMCP — How to build the risk-based compliance programme the FIC actually inspects

Choose Your Path to Exclusive Insights

Stay ahead in the world of accounting with premium content designed for professionals like you. Access expert articles, industry trends, and essential resources. Become a CIBA member and claim your CPD hours from CIBA.

CIBA Member Access

R250.00 FREE!

100% Discount when you become a CIBA Member. Join now to claim your CPD Hours. Register here: https://accounts.myciba.org/register