Paid Last. If You’re Paid At All.

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

Your client delivered R400 000 of steel on a handshake. The customer just filed for liquidation. Now your client wants to know what they can get back. The honest answer is usually: nothing.

That conversation happens in practices across the country every month. And the reason your client walks away empty-handed almost always comes down to one word they never thought about: security.

Why security decides who eats and who starves

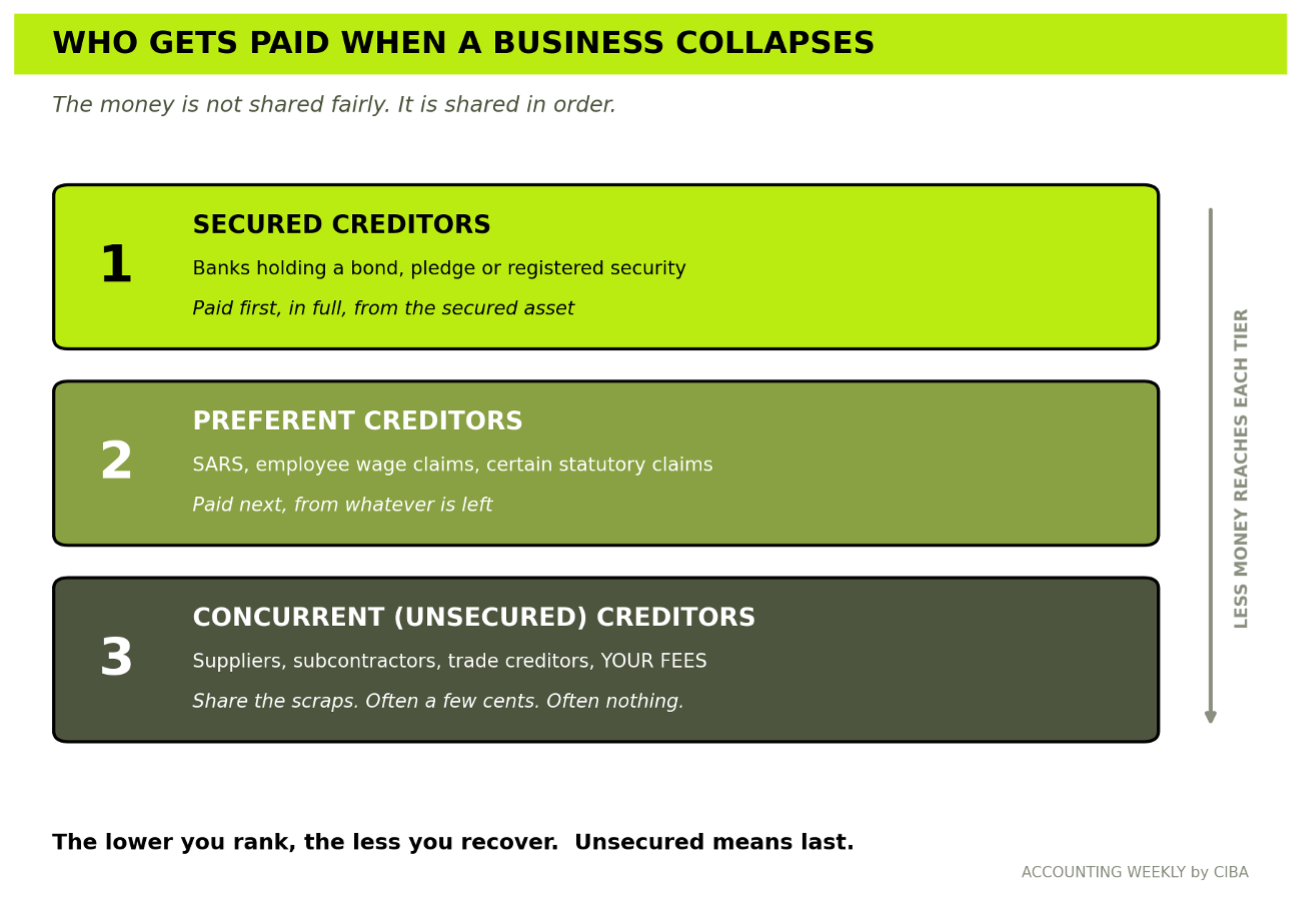

When a business collapses, the money does not get shared out fairly. It gets shared out in order. Secured creditors get paid first, from the specific assets tied to their claim. Everyone else, the suppliers, the subcontractors, the trade creditors, your client, lines up behind them and splits whatever is left. Which is often nothing.

How the money flows when a business fails, and why unsecured creditors line up last.

Security is simply the legal backup that moves a creditor to the front of that queue. A mortgage bond over property. A notarial bond over equipment. A cession of book debts. A pledge. A suretyship signed by a director. These are not banking technicalities. They are the difference between recovering 100 cents in the rand and recovering zero.

Most of your SME clients extend credit every single day without a shred of it. The wholesaler who supplies on 30 days. The construction subcontractor who pours the slab and invoices later. The logistics operator who moves the load and trusts the account. Every one of them is an unsecured creditor. And unsecured debt is risky debt.

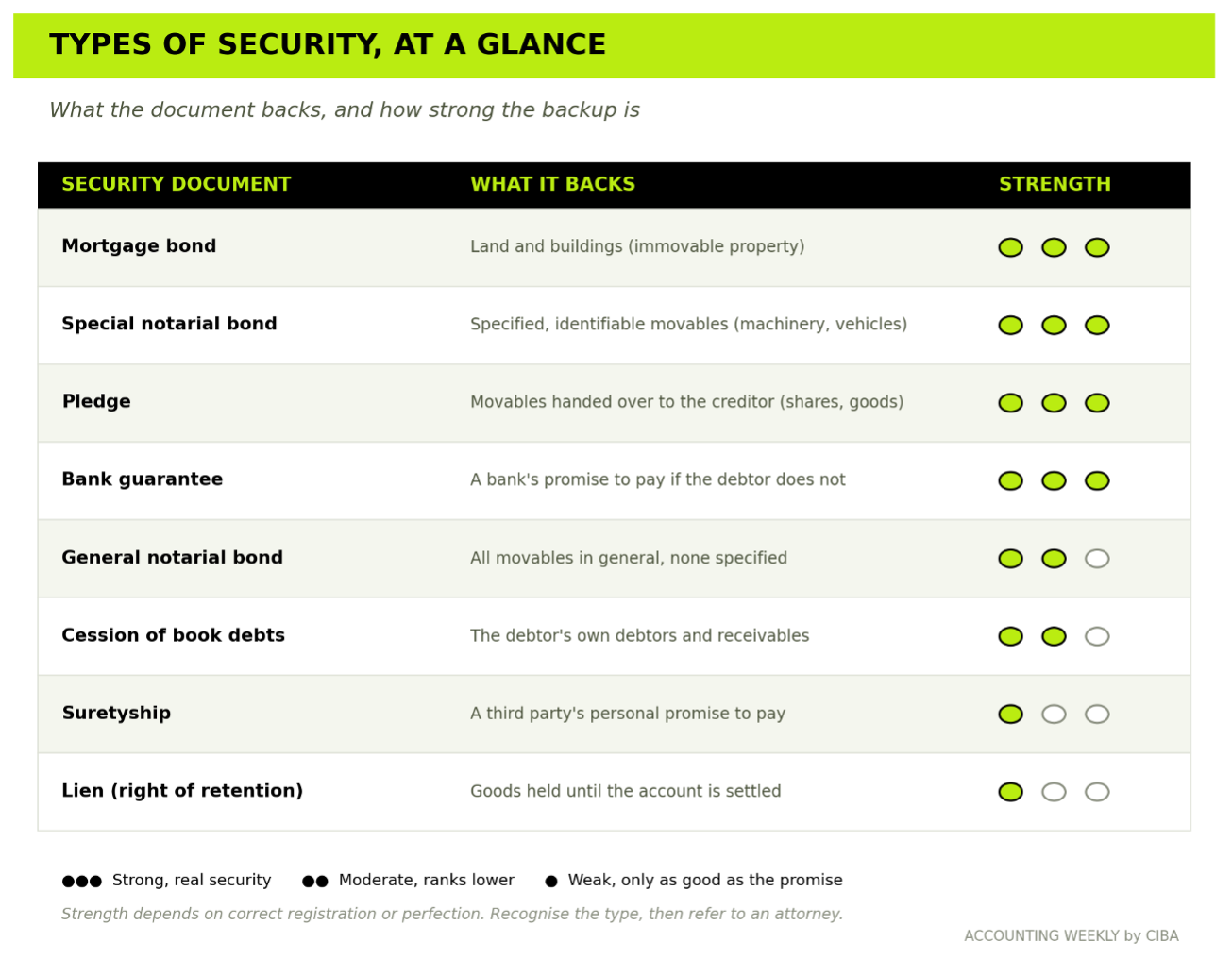

Types of security, at a glance

Not all backup is equal. Some security is real and registered, some is a personal promise worth only as much as the person who made it. You do not need to master the law of each one. You need to recognise which document is which, and how strong it tends to be, so you know when something looks thin and needs an attorney’s eye.

Recognition vocabulary, not legal advice. Strength always depends on correct registration or perfection.

This is your problem too

Here is the uncomfortable part. You are an unsecured creditor in your own practice.

Think about your fee book. The client who is three invoices behind. The one who keeps promising to settle “next month.” If that client goes under, you stand exactly where the steel supplier stands: at the back, holding a claim worth very little. Knowing how security works protects your own income before it protects anyone else’s.

As CIBA explored in Your Client Is Drowning in Debt. What’s Your Legal Role?, the financial position behind a failing debtor is your territory. Quantifying the exposure, modelling the recovery, flagging the risk early. That is real, billable work, and it is exactly where you add value.

The line you must not cross

There is a second uncomfortable truth, and it matters more than the first.

The moment you start telling a client whether their suretyship is “watertight,” or whether their security is “strong enough,” or whether they can enforce, you have stepped out of accounting and into legal advice. That is not your lane. It is unauthorised, it is uninsured, and it is the fastest way to convert a helpful conversation into a claim against you.

CIBA’s own analysis in Your Client Signed the Loan. Are You Exposed Too? puts it plainly. The National Credit Act reaches into loans, overdrafts, instalment sales, and the suretyships your clients sign without a second thought. Your job is to know the framework well enough to refer correctly, not to opine on enforcement.

So what is your role? Recognise. Flag. Refer. In writing.

You are the person who spots that the client is about to supply R1 million of goods to a single customer with no security in place. You are the person who notices the loan agreement was signed but never registered, so the “security” does not actually exist. You are the person who says: “This is a legal question. Let’s get your attorney to look at it before you sign.” That sentence is worth more to your client than any opinion you could risk giving yourself.

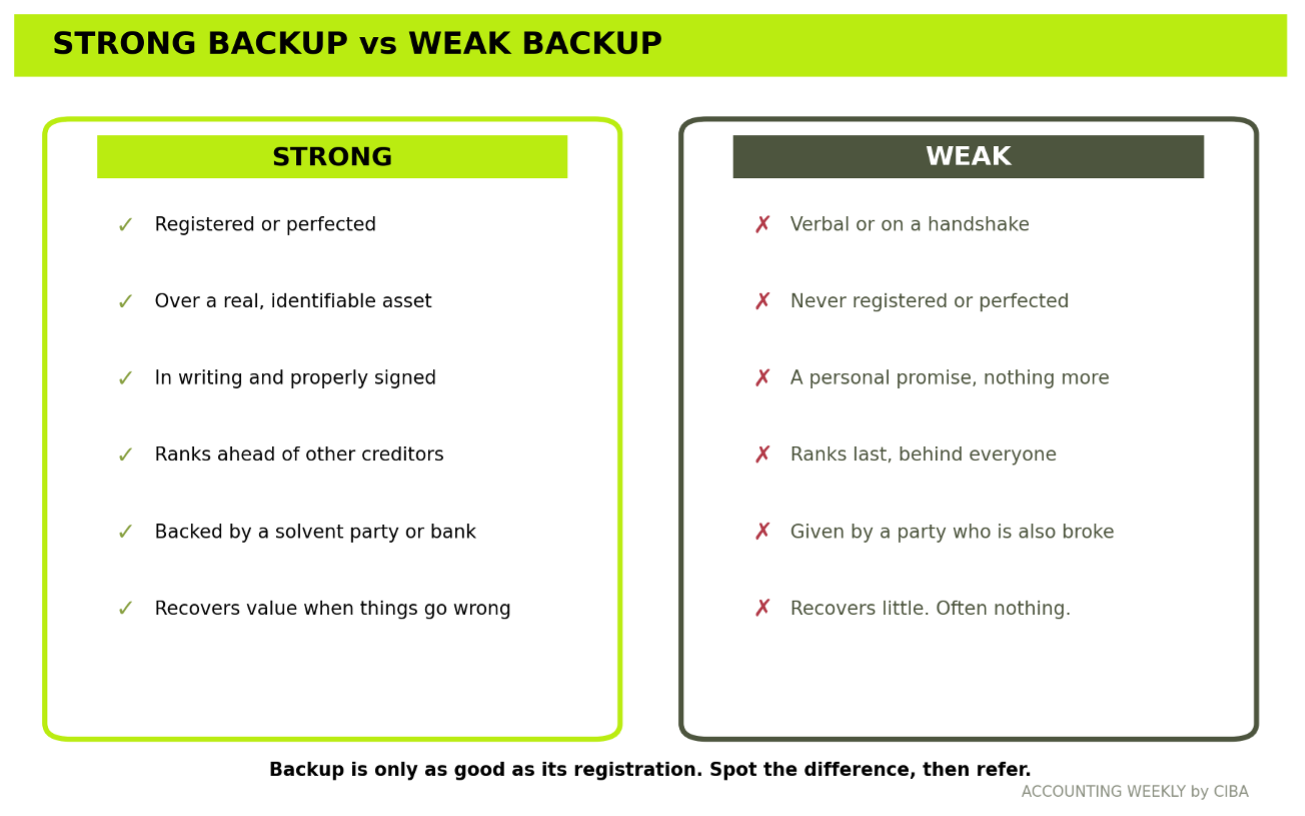

The difference between backup that recovers value and backup that recovers nothing.

The construction trap (and how to spot it)

Take one sector where this bites hardest. Construction.

A subcontractor on a large site does the work, submits the payment certificate, and waits. The main contractor runs into trouble and goes into business rescue or liquidation. As CIBA set out in Rescue Me, Accountant, the ranking of claims is tightly legislated, and secured creditors sit at the top. The bank with a bond over the development gets paid. The subbie with an unpaid certificate and no security gets cents, if anything.

You cannot fix that after the fact. But if you had seen the concentration risk in the debtor book six months earlier, you could have raised it. That is recognition. That is the service.

What you can do on Monday

You do not need a law degree. You need three habits.

First, read your own debtor book like a risk register. Which clients are over-exposed to a single customer? Which of your own fees are quietly turning into bad debt? Quantify it.

Second, learn the vocabulary. Know the difference between a real security right and a worthless promise, between strong and weak backup, between a claim that ranks and one that does not. Not to advise on it. To recognise it and raise it.

Third, build a referral reflex. When the conversation turns to enforcement, suretyships, or whether security will hold, you say the same sentence every time: this needs an attorney, and here is who I would call. Then you record that you said it. As Your PI Cover Has a Hole. Here’s Where It Is. makes clear, the paper trail is what protects you when a client later looks for someone to blame.

When your clients survive a debtor collapse instead of being sunk by one, they keep trading, they keep staff, and they keep paying you. That is how a single recognised risk ripples out into the wider economy.

LEARN IT PROPERLY

Law of Security: When Debt Needs Backup — CIBA CPD Webinar

Available from 30 June 2026 at 14:00 · Webinar · 2 CPD units

Covers what security means in law, the types of security, the priority of claims, enforcement realities, weak versus strong security, and recovery risk. In plain language, built for the conversation you will have with a client next week.

👉 Join CIBA and we’ll show you how to turn risk-spotting into advisory income clients will pay for, while keeping yourself firmly on the right side of the line.

Further Reading

Your Client Signed the Loan. Are You Exposed Too? — How the National Credit Act reaches suretyships and credit agreements, and the three ways accountants land in the liability chain.

Your Client Is Drowning in Debt. What’s Your Legal Role? — Where your financial advisory work ends and regulated debt and legal work begins, and how to stay in your lane.

Rescue Me, Accountant: How to Save Clients from Themselves (and Liquidation) — How claims rank in business rescue, why secured creditors come first, and where the accountant fits.

Your PI Cover Has a Hole. Here’s Where It Is. — Why a clear engagement letter and a written referral record decide whether your insurer pays out.

Choose Your Path to Exclusive Insights

Stay ahead in the world of accounting with premium content designed for professionals like you. Access expert articles, industry trends, and essential resources. Become a CIBA member and claim your CPD hours from CIBA.

CIBA Member Access

R250.00 FREE!

100% Discount when you become a CIBA Member. Join now to claim your CPD Hours. Register here: https://accounts.myciba.org/register

Premium

R250.00

Every month

Trending