Influencing Stakeholders: The Accountant's Strategic Edge

Imagine a Senior Accountant, Thabo, who identifies a significant leak in a company’s operational expenses. He presents a detailed 15-tab spreadsheet to the board, proving that a specific supplier is overcharging them. However, the board is focused on a new product launch and finds the data overwhelming. They thank him for his "input" and move on. Six months later, the company faces a liquidity crisis because those same costs spiraled out of control.

Thabo’s advice was technically perfect, but it was ignored. This highlights a hard truth for professionals: technical competence alone does not guarantee influence. To move from being a "number cruncher" to a strategic partner, you must master the art of stakeholder management.

Section 1: Understanding Your Stakeholder Landscape

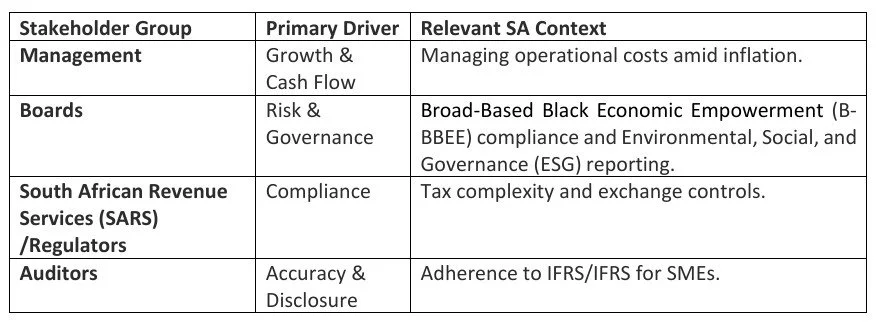

Your influence is often tied to how well you navigate a complex web of interests and regulations. Before you can influence anyone, you must map out who they are and what keeps them awake at night.

Mapping Motivations

Different stakeholders have different "north stars." For example, if you speak to a board about debits and credits when they care about risk mitigation, your message will most likely get lost.

The Trust Gap

Many business accountants struggle with the "trust gap", the perception that accountants are backward-looking historians rather than forward-looking advisors. To bridge this, you must stop reporting simply what happened and start explaining why it matters for the future.

Section 2: From Reporting to Advisory – Shifting Your Communication

The most practical way to gain influence is to speak their language. This means translating financial jargon into business impact.

The "So What?" Test

Never present a figure without a "So what?" attached to it.

Weak Communication: "Our profit decreased by 12% this quarter."

Influential Communication: "Our profit decreased by 12%, and if this trend continues, it will threaten our working capital within three months, potentially delaying our planned branch expansion."

The Past-Present-Future Framework

When presenting findings to management or clients, use this structure to ensure your insights are actionable:

Past: "We spent 15% more on fuel than budgeted last month."

Present: "This is currently eroding our margins on the Cape Town distribution route."

Future: "I recommend we renegotiate our fleet contract now to lock in rates, which will stabilize our margins for the upcoming peak season."

Lead with insights, support with numbers. Your first slide or paragraph should be the conclusion/recommendation; the supporting data should only be produced if someone asks to see the "engine room."

💡Real-World Example: Securing Board Approval

An accountant at a South African manufacturing firm noticed that aging machinery was causing a 5% increase in waste. Instead of asking for "Capital Expenditure for Asset Replacement," she framed it as a "Production Efficiency Opportunity." She showed how the new machinery would improve the company's B-BBEE procurement score and pay for itself in 18 months through reduced waste. The board approved the infrastructure spend immediately.

Section 3: Building Influence Through Credibility

Influence is built on a foundation of trust and consistency. You cannot influence a board if your VAT submissions are consistently late or inaccurate.

Deliver Consistently

Accuracy is your "license to play." Meet your deadlines, follow through on small commitments, and ensure your data is airtight.

Stay Current

South Africa’s regulatory environment is constantly shifting. Show your value by proactively informing stakeholders about changes in that environment, particularly those that affect each stakeholder’s primary driver.

Ask Better Questions

Move away from asking, "What figures do you need?" Instead, ask: "What decision are you trying to make?" This shift allows you to provide the right data, rather than just more data.

Call to Action: Your Path to Impact

In South Africa’s complex business environment, the accountants who thrive are those who can navigate both the ledger and the boardroom. Your technical skills as a CIBA member opened the door, but your ability to influence will determine how far you go within the organization.

Your Challenge: Choose one stakeholder relationship—perhaps a difficult department head or a skeptical client—and focus on strengthening it this quarter. Find out what professional issue keeps them awake at night. Then apply the "So What?" test to your next communication to them, linking it to how that affects their primary drivers. Watch how the conversation shifts.