Ethics Under Pressure: A Routine That Protects Your Designation

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

Ethical failures rarely begin with bad people. They begin with small decisions under pressure that no one stops. Here is what a professional accountant can do, in advance, to protect a designation that took years to earn.

Pressure rarely looks like a bribe

The professional risk most South African accountants face is not a brown envelope. It is the client who calls at 16:30 needing an EMP201 signed off. The employer who says, after a difficult quarter, 'make the numbers work for the board'. The long-standing client who has become a friend and asks you to be 'understanding' about a transaction.

The IESBA International Code of Ethics, which underpins the CIBA Code of Professional Conduct, names five categories of pressure on professional judgement: self-interest, self-review, advocacy, familiarity, and intimidation. Each is human. Each is silent. And each compromises judgement in a way that is hard to see from the inside.

Naming the threat is half the defence. Once a pressure is identified by its proper category, the conversation moves out of the emotional space and into the procedural one. That is where professional ethics actually lives.

Silence is never neutral

South African law has become very specific about silence in recent years.

Section 29 of the Financial Intelligence Centre Act requires a Suspicious and Unusual Transaction Report (STR) to be filed with the Financial Intelligence Centre when there is suspicion that funds are the proceeds of crime. The threshold is suspicion, not proof. Failure to report is itself a criminal offence. Tipping off the client about the suspicion is a separate criminal offence.

The Tax Administration Act requires disclosure of reportable arrangements to SARS. Tax practitioners registered under section 240A carry personal responsibility for the accuracy and timeliness of disclosure. Internal politics, board calendars, and client convenience do not extend the deadline.

The Protected Disclosures Act 26 of 2000, as amended in 2017, protects employees who blow the whistle in good faith through the prescribed channels. This is the legislative safety-net for the bookkeeper, the business accountant, the in-house finance professional who sees something and decides to speak.

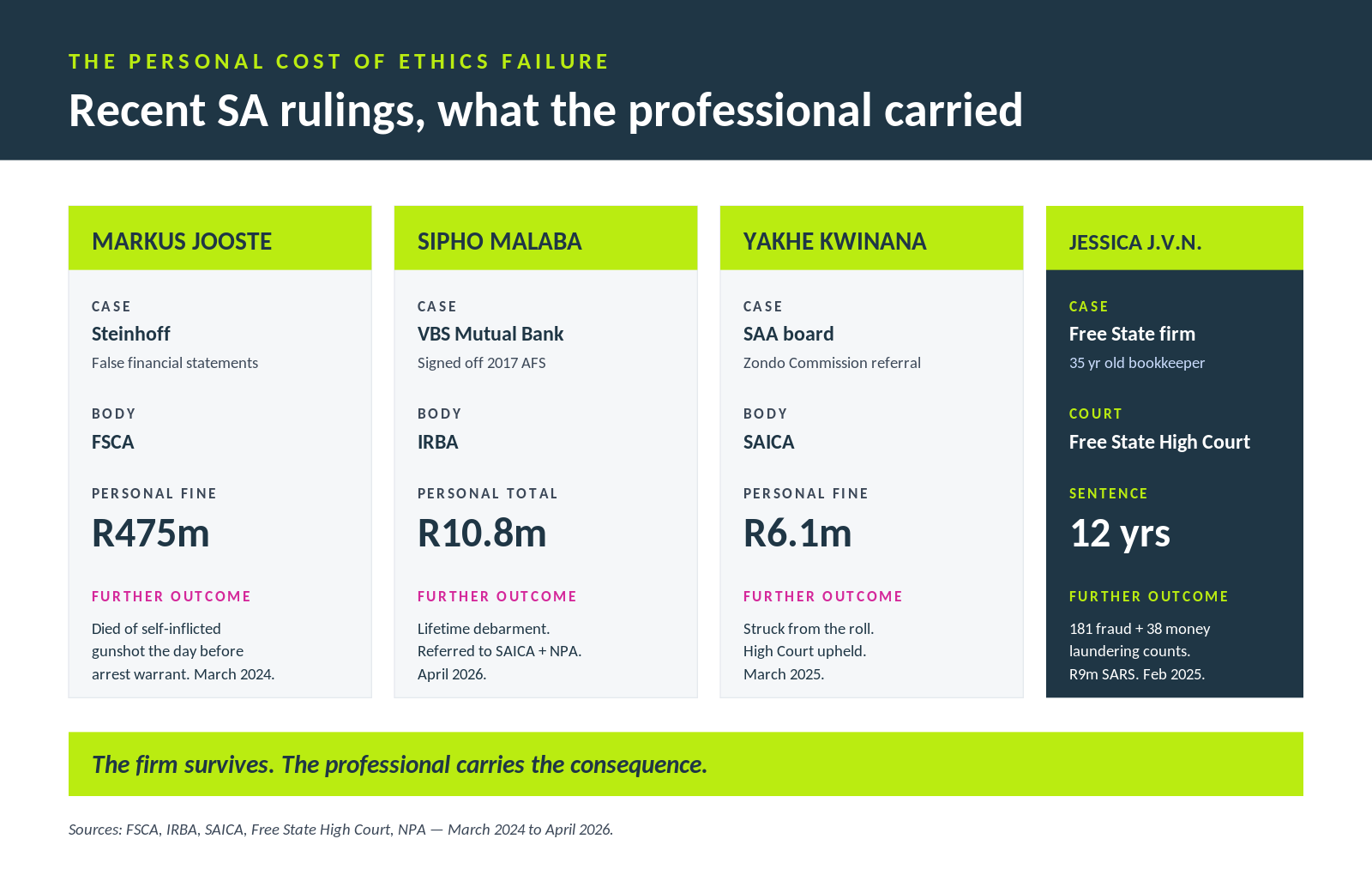

The professional carries the cost

Across the recent disciplinary and criminal record in South Africa, one pattern repeats. The firm survives. The individual professional does not.

Audit firms have paid hundreds of millions in settlements to liquidators and to JSE-listed companies since 2023 and continue to operate. The institutions move on. The named professionals do not move on at the same pace.

The Independent Regulatory Board for Auditors imposed lifetime debarment on a senior audit partner in April 2026, with a R1.6 million personal fine and a R9.2 million costs order. The Financial Sector Conduct Authority imposed a R475 million administrative penalty on a former JSE-listed CEO in March 2024. The Gauteng High Court upheld a SAICA strike-off in March 2025 against a chartered accountant found not to be a fit and proper person. The Free State High Court sentenced a small-practice bookkeeper to 12 years in prison in February 2025 for SARS fraud running across four years. Each ruling is a public record. Each carries the professional's name forever.

The protective routine

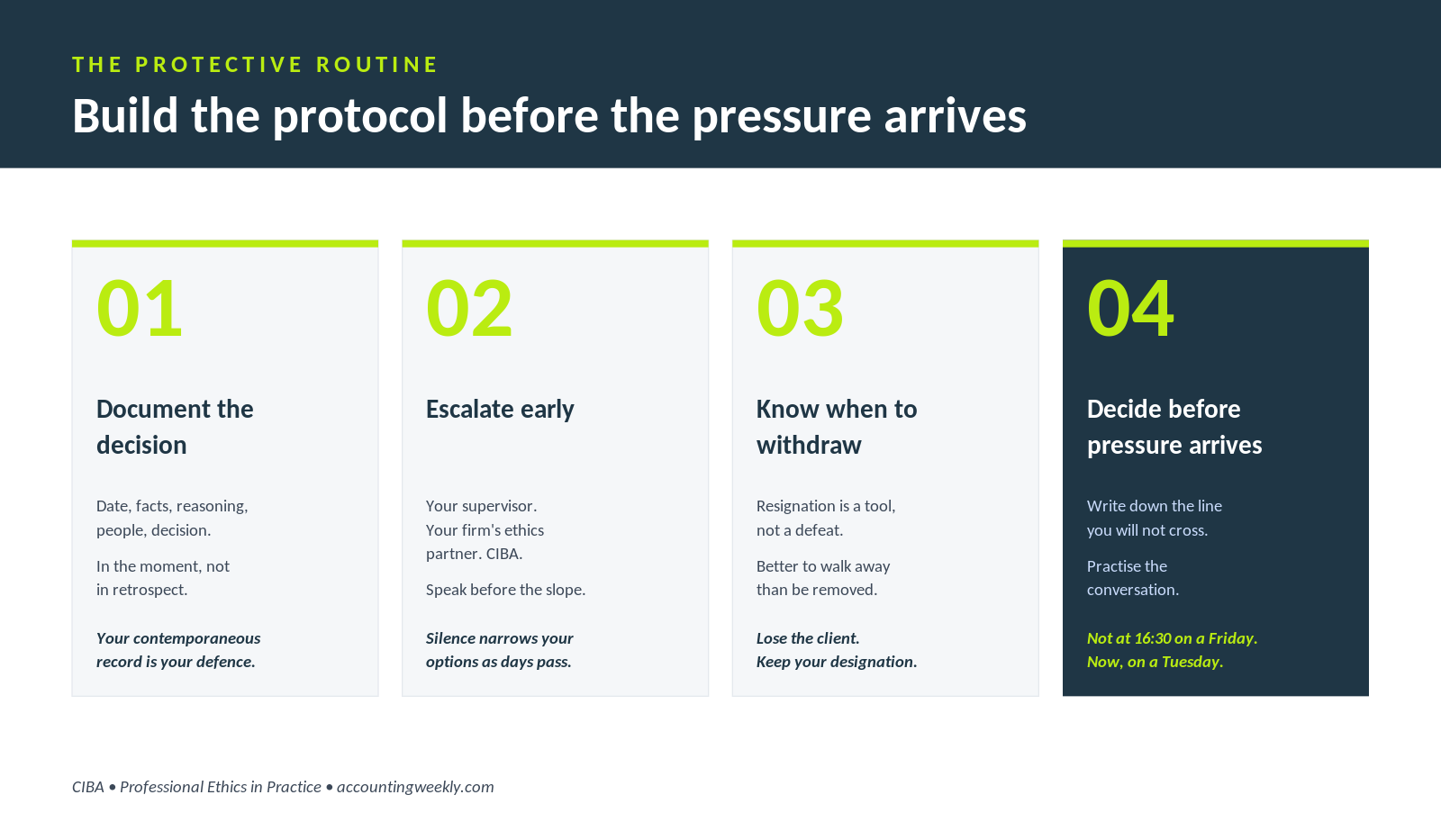

Four routines protect the professional in advance of pressure, not after it has arrived.

1. Document the decision in the moment. When the choice is to decline work, qualify an opinion, or escalate a concern, write it down. Date, facts, reasoning, people involved, decision taken. The contemporaneous record is the defence. Without it, the regulator will reconstruct the reasoning from the worst possible angle.

2. Escalate early. The supervisor, the firm's ethics partner, the professional body. Silence narrows the options available as the days pass. The longer the wait, the harder the raising, and the more compromised the position appears in retrospect.

3. Know when to withdraw. Resignation is a tool, not a defeat. Walking away with a designation intact is a better outcome than being removed from it. The choice is between a difficult conversation now and a worse one later.

4. Decide before the pressure arrives. Write down the line that will not be crossed. Discuss it with the team. Practise the conversation in the calm of a Tuesday morning, not the panic of a Friday afternoon. The time to plan the defence is not at 16:30 on a Friday.

A monthly risk identification checklist

Use this checklist monthly, or at the start of any new engagement. Tick honestly. The point is not to score zero. The point is to know where the pressure is, while there is still time to act.

Client and engagement red flags

☐ A client has asked for work I would not be comfortable showing a supervisor.

☐ One client now represents more than 15% of my total fees.

☐ I am preparing financial statements and also reviewing or signing them off.

☐ I have accepted gifts or hospitality from a client in the past twelve months.

☐ A current client is a family member, business partner, or close friend.

Pressure and judgement red flags

☐ Someone has said 'just this once' about an accounting treatment, an invoice date, or a disclosure.

☐ I have been asked to back-date, restate, or delay something.

☐ The instruction is verbal when it should be in writing.

☐ I am skipping procedures because of time, fee, or capacity pressure.

☐ I have accepted work that falls outside my professional competence.

Legislative duty triggers

☐ I suspect that funds in a client's account may be the proceeds of crime. (FICA section 29)

☐ I have identified a reportable arrangement that has not been disclosed to SARS. (Tax Administration Act)

☐ I am aware of a breach or irregularity at a client or employer that has not been escalated.

Documentation and escalation gaps

☐ I have not documented the reasoning behind a recent judgement call.

☐ I have not raised any of the above with a supervisor, my firm's ethics partner, or CIBA.

☐ I do not know who I would escalate to if pressure arrived tomorrow.

How to read your score

0 ticks. The protective routine is working. Continue documenting and reviewing monthly. Diarise the next review.

1 to 2 ticks. Name the threat using the IESBA framework. Document the reasoning. Decide this week whether escalation is required.

3 or more ticks. Stop. Document the position. Escalate to a supervisor, the firm's ethics partner, or CIBA before the week is out. Consider whether withdrawal from the engagement is required.

Ethics is a career asset, not a compliance overhead

The CIBA Code of Professional Conduct, the IESBA International Code of Ethics, and the IRBA Code for assurance work share the same five fundamental principles. Integrity. Objectivity. Professional competence and due care. Confidentiality. Professional behaviour. The principles do not change between codes. The standard does not bend in response to pressure.

Strong ethics is what makes a designation portable, a name trusted, and a career durable in a profession where everyone knows everyone, and where mistakes are remembered far longer than good intentions. It is the durable asset that survives every difficult client, every restructure, every tribunal.

The routine is the protection. The protection is the asset. Build it before it is tested.

Key Takeaways

▸ Ethical failures rarely begin in one moment. They build through silence, rationalisation, and small compromises under pressure.

▸ The IESBA framework names five threats to professional judgement, self-interest, self-review, advocacy, familiarity, and intimidation. Naming the threat is the first defence.

▸ South African legislation criminalises silence in specific cases. FICA section 29, the Tax Administration Act, and the Protected Disclosures Act all carry duties that override convenience.

▸ Recent regulator and court outcomes show one pattern. The firm survives. The professional carries the consequence, in fines, debarment, strike-off, or imprisonment.

▸ Four routines protect the professional in advance, document the decision, escalate early, know when to withdraw, and decide the line before the pressure arrives.

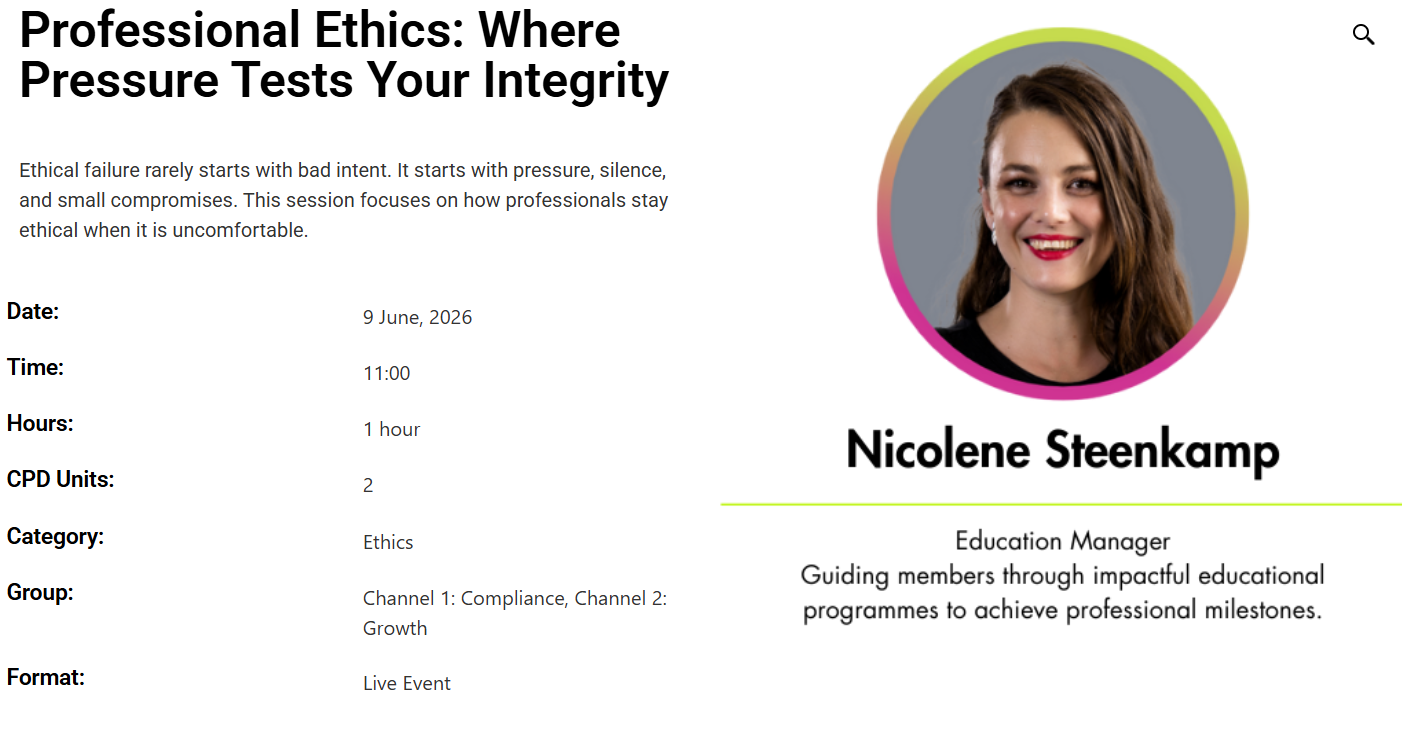

CPD ON Professional Ethics: Where Pressure Tests Your Integrity

Ethical failure rarely starts with bad intent. It starts with pressure, silence, and small compromises. This session focuses on how professionals stay ethical when it is uncomfortable.