Could the State Force Your Client's Crypto Sale?

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

Your client built a small tech business. He gets paid in crypto by an overseas customer, holds some Bitcoin, and runs a tidy set of books. Then he forwards you a draft regulation and one line in the news: the State could make him sell his crypto. He wants to know if it is true, and he wants to know today.

This is the moment exchange control stopped being someone else's problem. For the first time, crypto assets are being pulled into South Africa's exchange-control net, sitting alongside foreign currency, gold, and securities. If you advise anyone with a wallet, a foreign income stream, or a cross-border payment, this lands on your desk.

Figure 1. Crypto now sits inside the same cross-border perimeter as currency, gold and securities.

What the draft regulations actually do

On 17 April 2026, National Treasury published the draft Capital Flow Management Regulations, 2026, for comment by 30 June. They are made under the old Currency and Exchanges Act of 1933, and they repeal the 1961 Exchange Control Regulations that have governed cross-border money for over sixty years. That repeal is overdue and welcome.

But the draft does more than modernise. Above a set value, it lets the State compel a holder to sell foreign currency or crypto, in rand, within 30 days. It restricts taking crypto, currency, gold, or securities out of the country without permission. It allows attachment and forfeiture on reasonable suspicion. And in defined cases, it permits entry and search of premises without a warrant.

Before the panic spreads, two things need saying clearly, because a lot of the public noise has been wrong. The draft does not criminalise owning crypto. The offence attaches to breaking the rules, not to holding the asset. And the requirement to hand over passwords and keys applies only to crypto that has already been forfeited under the regulations. It is not a roadside power. CIBA has put both clarifications on record, because overstated fear helps no one and good advice depends on getting the facts straight.

South Africa only came off the FATF grey list in October 2025, as Accounting Weekly covered in SA is Off the Greylist: What Does the Big News Mean?. With the next FATF review due in 2026 and 2027, nobody is arguing that South Africa should drop its guard. The question is whether this particular instrument is the right tool.

CIBA said yes to the goal, no to the design

CIBA lodged a formal submission with National Treasury on 29 June 2026, signed by CEO Nicolaas van Wyk. The position is not opposition. CIBA backs the modernisation, the alignment with FATF and OECD standards, and bringing crypto inside a clear regulatory perimeter. The concern is execution. Five problems run through the draft, and every one of them lands on the professional who has to advise on it.

The threshold is blank. A single value decides how far at least eight of these regulations reach. That value is not in the draft. The Minister will fix it later. Until then, you cannot tell your client whether the rules bite only on large institutional transfers or on an ordinary retail wallet and routine business payments. CIBA's view is blunt: you cannot run a real public comment process on a regulation whose central number is hidden. Publish the threshold, then reopen comment.

The definition of "capital" is too wide. As drafted, "capital" means almost anything with monetary value, including intellectual property held entirely inside South Africa. An instrument meant to manage money crossing borders should not, on its face, reach a trademark used only in Johannesburg. The Constitutional Court has previously stated, in relation to another matter, that currency regulation powers are "unusually wide," but even that power stays tied to currency, banking, and exchanges. Stretch the definition past that, and you hand a future litigant an easy review. CIBA proposes a tighter definition anchored to value that actually moves across the border.

Figure 2. CIBA's central argument: the world supervises the platform, not the asset.

Forced sales and forfeiture touch constitutional rights. Compulsory acquisition is a deprivation of property and engages the right to privacy. CIBA is a professional accountancy body, not a law firm, so it flags these for Treasury's own legal scrutiny rather than ruling on them. But one technical point is squarely an accountant's business: "market value on the day of purchase" is a hopeless valuation standard for an asset that can swing ten percent in a day. CIBA recommends a defined reference price, a fixed valuation time, conversion at the SARB rate, and a fast dispute pathway.

Warrantless entry plus reverse onus needs a check. The draft lets officials enter and search without a warrant in some cases, and treats any person present in the country as resident until they prove otherwise. CIBA recommends real judicial oversight for non-consensual entry, and a fairer residence test.

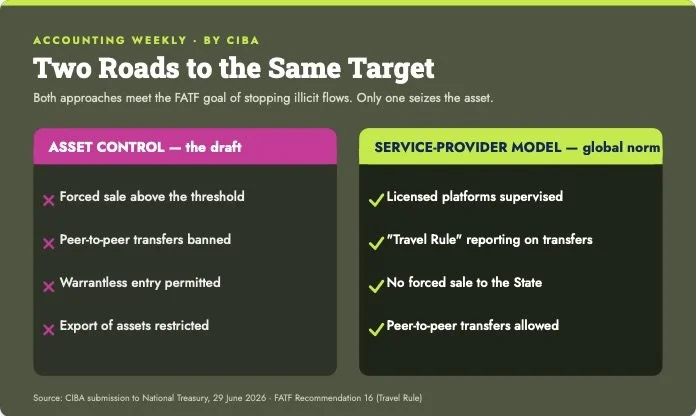

The whole approach is heavier than the goal requires. This is the heart of it. Almost every comparable country meets its FATF crypto obligations through the Travel Rule, which supervises the licensed platform, not the asset. The platform records who sends and who receives above a published threshold. The individual does not need permission to transact, is not forced to sell to the State, and can still send crypto directly to another person. The EU, United States, United Kingdom, and Singapore all run versions of this. None of them seizes the asset. South Africa has already built most of this machinery through the FSCA and the FIC Act. The same approach also matches the OECD's Crypto-Asset Reporting Framework that South Africa is adopting, which Accounting Weekly explained in New Regulations Affecting the Reporting on Crypto Assets.

Figure 3. On forced sales and an undisclosed threshold, the draft makes South Africa the outlier.

The part that should make you sit up

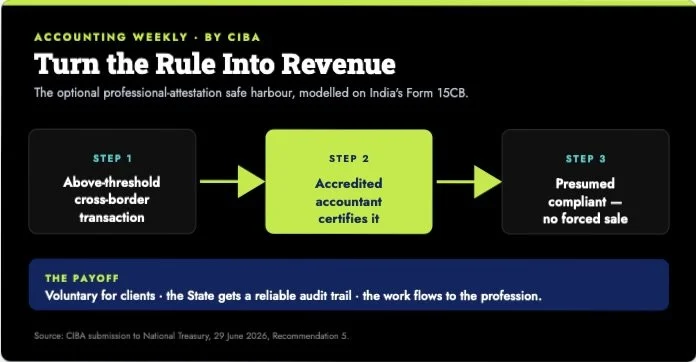

Buried in CIBA's recommendations is an idea that could put accountants at the centre of this regime, not on the receiving end of it. CIBA has proposed an optional professional-attestation safe harbour, modelled on India's Form 15CB. In India, before a large cross-border remittance goes through, a qualified accountant signs a certificate confirming it complies with the law. The bank will not process the transfer without it.

Figure 4. The safe harbour puts accountants at the centre of the regime — and turns compliance into a billable service.

Picture the South African version. An above-threshold cross-border crypto or currency transaction, certified by an accredited and professionally liable practitioner as compliant, is presumed compliant. The holder is not forced to sell. The State gets a reliable, professionally prepared audit trail over exactly the high-risk transactions it cares about. And the work, the certification, the ongoing monitoring, the compliance opinion, flows to the profession that is trained, accountable, and already doing assurance.

That is the same shift Accounting Weekly described in The Cash Clients That Could Cost You: every new compliance duty is also a service you can charge for. The accountants who read this regime early will not be the ones panicking when it commences. They will be the ones their clients pay to navigate it.

Your practical takeaway

You do not need to wait for the final regulations to act. Do three things now. First, run a quick scan of your client base and flag anyone with crypto holdings, foreign income, or cross-border payments. These are your exposed clients, and the conversation is best started by you, not by an enforcement officer. Second, confirm your own FIC registration is current and that you are listed under the right item, because a service-provider model only strengthens the duties you already carry. Third, package the knowledge. A short briefing note to affected clients explaining what is proposed, what is overstated, and what to watch for is a billable advisory service and a trust-builder in one.

This is what it looks like to be the expert in the room. You are not doing admin. You are keeping your clients on the right side of a regime that most of their advisers have not even read yet.

FURTHER READING

SA is Off the Greylist: What Does the Big News Mean? — Why the FATF context behind these regulations matters for your practice.

The Cash Clients That Could Cost You — How to turn FICA and AML duties into a real advisory service.

New Regulations Affecting the Reporting on Crypto Assets — South Africa's adoption of the OECD Crypto-Asset Reporting Framework, explained.

The Accountant's Magnifying Glass: Finding Out Who Your Client Really Is — A practical KYC and beneficial ownership process for your firm.

IRS Crypto Crackdown Beats Legal Challenges — How courts abroad have treated crypto privacy and surveillance arguments.