Your Financial Instruments Fallback Is Gone. Here Is What Replaces It.

The IAS 39 fallback is gone, and the new IFRS for SMEs Section 11 brings a simpler, more practical approach to financial instruments. The key change is the introduction of the SPPI test, which helps determine whether instruments are measured at amortised cost or fair value. Accountants should now review financial instruments, intragroup guarantees, and extended credit arrangements to ensure compliance with the third edition. While some rules have changed, the standard remains focused on providing clear, relevant, and reliable financial information for SMEs.

The Accounting Standard That Quietly Changed Everything

Accounting standards rarely make headlines, but the latest update to IFRS for SMEs is one of the most significant changes in years. With major revisions to revenue recognition, business combinations, consolidation, financial instruments, and fair value measurement, accountants and business owners need to start preparing now. The transition period is already underway, and those who understand the changes early will be best positioned to guide their clients through what comes next.

The Most Valuable Assets You Cannot See

Intangible assets are often some of the most valuable resources a business owns, yet they are also among the least understood. From software and licences to patents and trademarks, these assets help businesses generate income and remain competitive, even though they cannot be physically seen or touched. Understanding how IFRS for SMEs treats intangible assets is essential for finance professionals, particularly when deciding whether costs should be recognised as assets or expensed. By applying the principles of Section 18 correctly, accountants can ensure that financial statements remain accurate, reliable, and useful for decision-making.

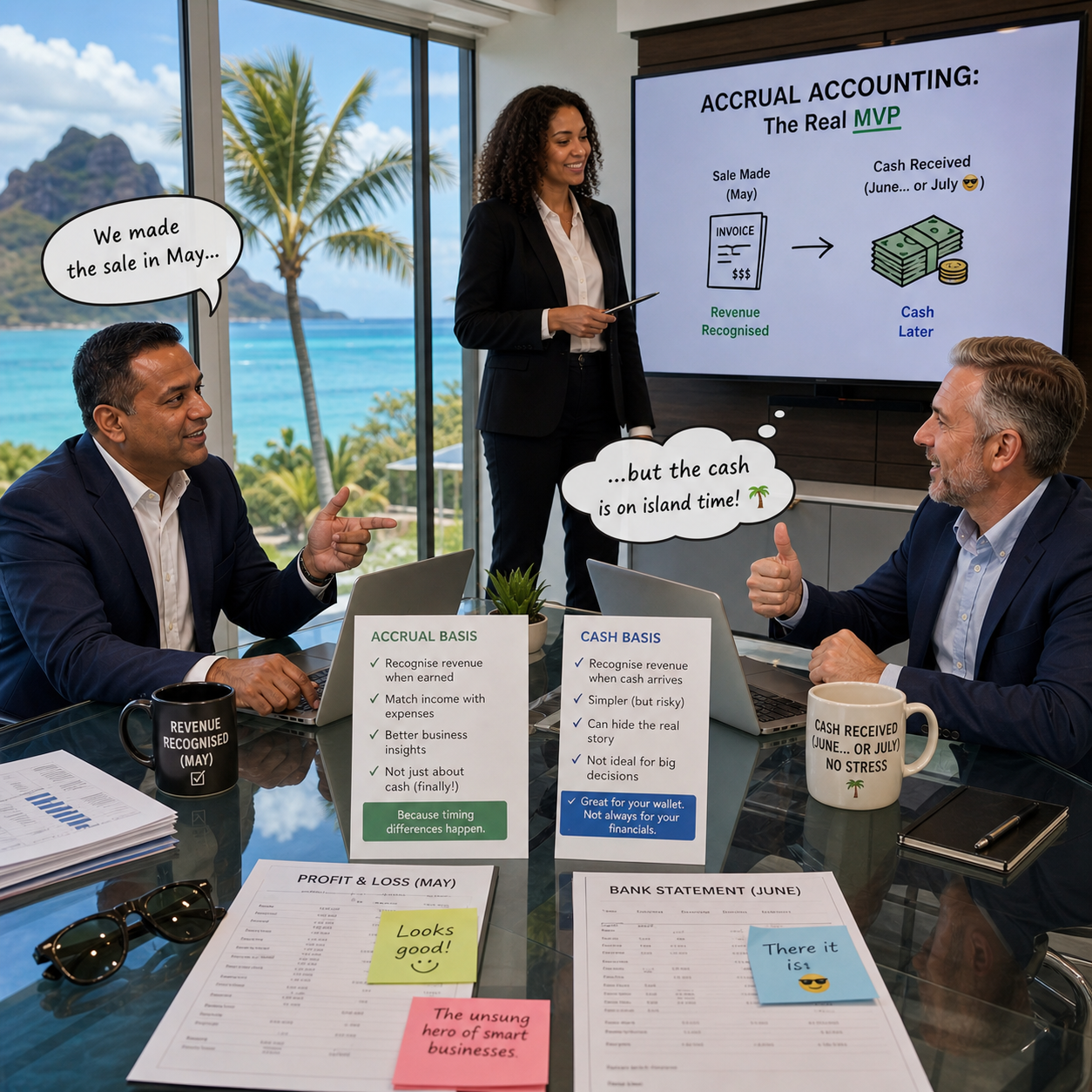

Accrual Accounting: The Quiet Principle That Changes Everything

Accrual accounting is the principle that ensures financial statements reflect what actually happens in a business, not just when cash moves in and out of the bank. By recognising income when it is earned and expenses when they are incurred, it provides a clearer and more accurate picture of performance. This approach moves beyond the simplicity of cash accounting and allows business owners and professionals to understand the true results of their activities, make better decisions, and avoid the misleading effects of timing differences.

IFRS for SMEs vs ISRS 4410: Know the Difference

When preparing a compilation report for an SME, it is important to understand that IFRS for SMEs and ISRS 4410 do not compete with each other. They serve different purposes. IFRS for SMEs is the framework used to prepare the financial statements, which means it determines how the numbers and disclosures are presented. ISRS 4410 is the standard that guides the practitioner on how to perform the compilation and how to write the report. In simple terms, IFRS for SMEs explains what the financial statements must look like, while ISRS 4410 explains how the practitioner does the work and reports on it.

Fair Presentation, Because Creative Accounting is Frowned Upon

Financial statements must be clear, accurate, and follow IFRS for SMEs. They should reflect the true financial position of a business and include key reports like the balance sheet, income statement, and cash flow statement. Consistency, transparency, and proper labeling help ensure reliability for investors and stakeholders.

Investment Property and IFRS for SME’s

Investment property under IFRS for SMEs refers to land or buildings held for rental income or capital appreciation. The standard outlines how to recognise, measure, and disclose investment property in financial statements. Properties can be measured at fair value if reliably measurable or at cost if not. Mixed-use properties require classification based on usage. Leased properties can be treated as investment property under specific conditions. Proper accounting ensures transparency and accurate financial reporting for SMEs.