VAT Registration Reset: What the VAT Increase Really Means for Your Clients

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

The VAT registration threshold was last adjusted seventeen years ago, increasing from R300,000 to R1,000,000. Clearly, the business environment has changed dramatically since 2009, and a further increase in the threshold was long overdue.

CIBA has persistently lobbied for a review of the VAT registration threshold requirements. At long last, it has begun to see the results of these sustained efforts. With effect from 1 April 2026, the compulsory VAT registration threshold will increase to R2,300,000. At the same time, the voluntary VAT registration threshold will rise from R50,000 to R120,000.

Vendors welcome the change — but there are important considerations to keep in mind.

New Registration Thresholds: New Questions

While the increase in VAT thresholds is most welcome, any significant change inevitably raises new practical questions, including:

Should we expect a wave of VAT de-registrations now that the compulsory registration threshold has increased substantially?

What advice should tax practitioners give their clients? Should businesses de-register as VAT vendors, or retain their vendor status?

Guidance for Tax Practitioners

The first point to bear in mind is that when a person ceases to be a VAT vendor, any goods that formed part of the enterprise’s assets (excluding goods on which input tax was denied, such as motor cars and entertainment) are deemed to have been supplied by the vendor immediately before the cessation of vendor status.

The value of this deemed supply (also referred to as “exit VAT”) is the lower of:

The cost to the vendor (including the cost of transport and installation). In the case of inventory, this also includes all costs forming part of the trading stock valuation; and

The open market value.

No deemed supply will arise if:

The total value of taxable supplies made by the vendor during the preceding 12 months did not exceed R20 000; or

The vendor ceases to be registered in respect of a commercial or residential rental enterprise solely because the total receipts and accruals from that enterprise during the preceding 12 months did not exceed R48 000.

However, it is hoped that SARS will issue a statement on this matter, as you may recall that schools which were required to deregister were previously granted a special dispensation regarding the terms on which the exit VAT had to be settled.

The decision to remain registered or to de-register for VAT should be made on a case-by-case basis. As VAT is essentially a tax that is paid on ‘value-added’, in other-words on profits made - it is expected that many entities under R2.3 million turnover will be interested in de-registering.

Businesses with taxable supplies exceeding R2.3 million will be required to remain registered. For those below the threshold, the following considerations may assist.

A key factor is the VAT status of the client’s customers.

Businesses supplying mainly final consumers (individuals)

If a small business has taxable supplies below R2.3 million and most of its customers are individuals who are final consumers, de-registration may be advantageous. However, SARS will still require all outstanding VAT201 returns to be submitted and any liabilities settled. The new threshold applies only from 1 April 2026.

Businesses supplying other VAT-registered entities

If a small business has taxable supplies below R2.3 million but primarily supplies other businesses that are VAT vendors (with taxable supplies exceeding R2.3 million), those customers will prefer dealing with VAT-registered suppliers in order to claim input tax. In such cases, the business may find it commercially necessary to retain its VAT vendor status despite being below the threshold. Administrative obligations, such as submitting VAT201 returns, should also be considered.

A Positive Development for Small Businesses

Overall, the 2026 Budget appears supportive of small businesses. Reducing the VAT compliance burden provides both new and existing small enterprises with greater capacity to grow. Although the removal of VAT obligations may increase taxable income, potentially resulting in higher provisional and corporate tax liabilities, this impact may be moderated by other relief measures.

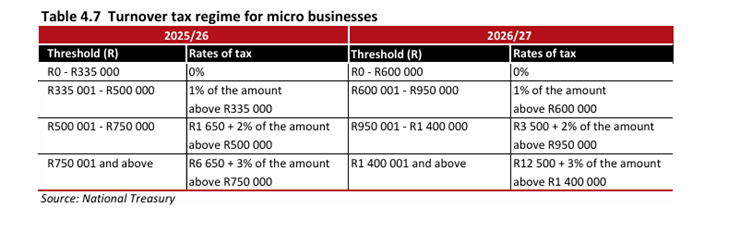

Micro Businesses

If a business qualifies as a micro business, the new tax rates effective from 1 March 2026 are as follows:

Annual turnover limit for the turnover tax is increased from R 1 000 000 to R2 300 000.

For the year of assessment ending 28 February 2026, no corporate tax was payable where taxable turnover was below R335,000. With effect from 1 March 2026, this threshold has been increased, and no tax will be payable where taxable turnover is below R600,000.

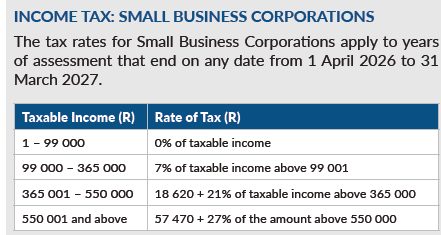

Small Business Corporation (SBC)

If the business can be classified as micro business, the new rates with effect from 1 April 2026 (not March 2026) 2026 are as follows:

Business classified as SBC will only pay corporate income tax if their taxable income exceeds R99 000 (previously R95 750).

Conclusion

The changes to the VAT regime announced on Budget Day 2026 are significant and mark a new phase for small business development. This phase is further characterised by increased tax relief for micro businesses and Small Business Corporations (SBCs).