What Is Your Practice Really Worth?

Free Cash Flow Valuation Explained

Most practitioners spend their careers building something valuable, then stumble at the finish line because they never actually know what their practice is worth. They rely on rough rules of thumb, like "one times annual revenue" or "a multiple of profit," only to discover at the negotiating table that buyers think very differently.

Sophisticated buyers, whether private equity, corporate consolidators, or experienced individual purchasers, do not buy revenue. They do not even buy profit. They buy cash. Specifically, they buy the cash your practice will generate for them after they own it.

That is what Free Cash Flow (FCF) valuation measures, and it is the language buyers actually speak. If you are thinking about selling your practice in the next one to ten years, understanding this method is one of the highest-return things you can learn.

Why Rules of Thumb Fail You

Many practitioners are told their practice is worth a fixed multiple of revenue or earnings. These rules of thumb are seductive because they are simple, but they almost always understate or overstate value, and either outcome costs you money.

A revenue multiple ignores profitability. Two practices with identical turnover can have wildly different earnings, working capital needs, and capital expenditure profiles. Yet the same multiple gets applied to both.

An earnings multiple ignores reinvestment. A practice that reports strong profit but constantly needs new equipment, software upgrades, or growing receivables is not as valuable as one with the same profit and lower reinvestment needs.

Both ignore risk and growth. A stable, growing practice in a defensible niche is worth more than a volatile one with the same earnings, but a flat multiple does not capture this.

Free Cash Flow valuation addresses all three weaknesses. It values your practice based on what a buyer can actually take out of it, adjusted for the risk of getting it.

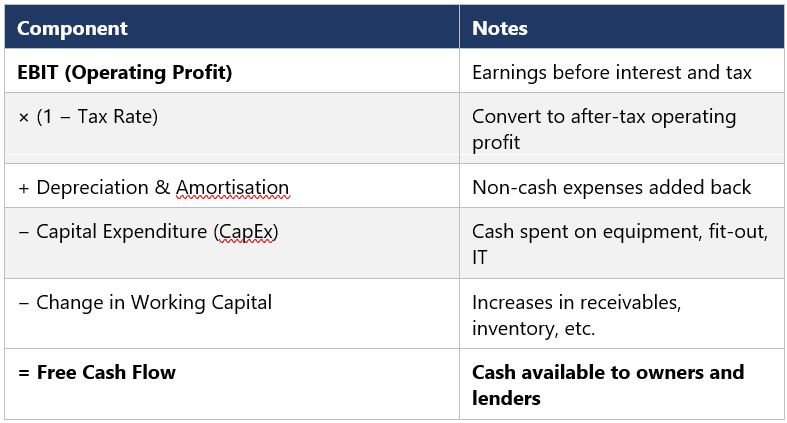

What Free Cash Flow Actually Is

Free Cash Flow is the cash your practice generates each year after paying everything it needs to keep operating and growing. It is not profit. It is not EBITDA. It is the cash a new owner could realistically pocket or reinvest.

The Standard FCF Formula

The most widely used version is Free Cash Flow to the Firm (FCFF), which represents cash available to all providers of capital before debt is considered:

This number, repeated and projected forward over several years and then discounted back to today, becomes the foundation of your practice's valuation.

The Three Levers That Drive Your Valuation

Once you understand FCF, three levers determine how much your practice is worth. Every action you take in the years leading up to a sale should be evaluated against these:

1. The Size of Future Cash Flows

Buyers project your FCF forward, typically five to ten years. The higher and more sustainable that projected stream, the more they will pay. This is why the years immediately before a sale matter so much. A buyer looking at your last three to five years of trading will form a view of where the cash flows are heading.

2. The Growth Rate

A practice with stable but flat cash flows is worth far less than one growing at five to ten percent per year. Even modest growth, sustained over many years, dramatically increases value because each future year's FCF is larger than the last. Demonstrable growth, supported by data on patient or client numbers, average fees, and retention rates, is one of the most powerful value drivers.

3. The Discount Rate (Risk)

Future cash is worth less than cash today, both because of the time value of money and because future cash is uncertain. Buyers apply a discount rate, typically the Weighted Average Cost of Capital (WACC), to convert future FCFs into today's value. The riskier your practice appears, the higher the discount rate, and the lower the valuation.

Risk factors that increase the discount rate include heavy reliance on the owner, concentration in a few major clients or referrers, regulatory exposure, and weak systems or documentation. Reducing these risks is one of the cheapest ways to lift your valuation.

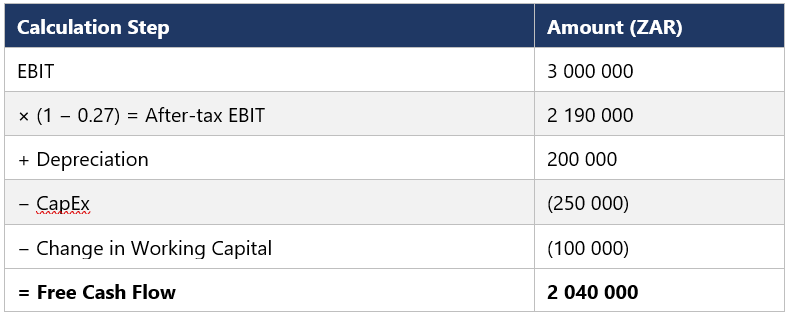

A Worked Example

Consider a practice with the following profile in its most recent year:

• Revenue: R 12 000 000

• EBIT: R 3 000 000 (25% margin)

• Tax rate: 27%

• Depreciation: R 200 000

• CapEx: R 250 000

• Change in working capital: R 100 000

The Free Cash Flow for this year is calculated as follows:

Now assume the practice is expected to grow FCF at 5% per year for the next ten years and then settle into long-term growth of 2% thereafter. Using a discount rate of 14%, the present value of the next ten years of cash flows plus a terminal value will produce a valuation in the region of R 22 to R 25 million, depending on assumptions.

Compare that to a simple "one times revenue" rule of thumb, which would value the practice at R 12 million, or a 4× EBIT multiple, which would give roughly R 12 million as well. The FCF method, properly applied, often reveals that a well-run, growing practice is worth substantially more than the rules of thumb suggest.

How to Increase Your FCF Valuation Before You Sell

The valuation is not fixed. Practitioners who understand the FCF model can take deliberate steps in the two to five years before a sale to materially increase what they receive at the closing table. The most effective actions fall into four categories:

Lift Operating Margins

Margin improvements flow directly into higher EBIT, which compounds across every projected year. Review pricing, fee structures, staff productivity, and supplier costs. A two to three percentage point margin improvement, sustained, can add millions to your final sale price.

Reduce Working Capital Drag

Slow-paying clients, bloated inventory, and inefficient billing all consume cash. Tightening credit terms, automating invoicing, and improving collections frees up cash today and reduces the working capital deduction in your FCF calculation.

Be Smart About CapEx

Necessary investment is fine, but unnecessary or poorly timed capital spending in the years before a sale directly reduces FCF. Prioritise investments that produce visible returns within the projection window, and avoid large discretionary purchases close to a sale unless they materially support growth.

De-risk the Practice

This is where many owners leave the most money on the table. Anything that reduces the buyer's perceived risk lowers their discount rate and increases your valuation. Concrete actions include:

• Reducing dependency on the owner by building a capable second tier of practitioners or managers.

• Diversifying the client, patient, or referrer base so no single source represents an outsized share of revenue.

• Documenting systems, protocols, and procedures so the practice runs without you in the room.

• Securing long-term contracts, retainers, or recurring revenue streams that buyers can model with confidence.

• Cleaning up the financials so historical FCF is easy to verify and trust.

Common Pitfalls Practitioners Should Avoid

Confusing profit with cash. A profitable practice can still generate weak FCF if it absorbs cash through working capital growth or heavy capital spending. Buyers will spot this immediately.

Loading personal expenses through the practice. Many owners run cars, travel, or family expenses through the business, which depresses reported profit. These add-backs need to be documented, defensible, and presented cleanly during due diligence; otherwise, buyers will discount them or ignore them.

Selling on a peak year. A single exceptional year does not create a sustainable FCF stream. Buyers normalise earnings across multiple years, so timing your exit immediately after an unrepeatable boom rarely captures the upside you expect.

Underestimating the discount rate. Owners often value their own practice using rates that are far too low because they do not perceive the risks the way buyers do. A realistic discount rate, benchmarked against similar transactions, gives you a more honest picture.

What to Do Next

If you are within ten years of selling, treat your valuation as a project, not an event. The work you do now will determine what you walk away with.

1. Calculate your current FCF using the formula above, working from your most recent two to three years of financials. Look for trends, not just a single year.

2. Identify your three biggest risk factors from a buyer's perspective. Write them down. These are your priority projects.

3. Build a simple five-year projection of revenue, EBIT, CapEx, and working capital. Stress-test it. Buyers will.

4. Engage a valuation professional at least eighteen to twenty-four months before you intend to go to market. The earlier you have a credible number, the more time you have to improve it.

5. Document everything. Buyers pay premiums for clarity. Clean management accounts, signed contracts, written procedures, and a clear organisational structure all reduce the discount rate applied to your cash flows.

The Bottom Line

Your practice is worth the present value of the cash it will produce for its next owner, adjusted for the risk of producing that cash. Rules of thumb miss this entirely. Free Cash Flow valuation captures it directly.

The practitioners who walk away from a sale with the strongest outcomes are not necessarily the ones with the highest revenue or even the highest profit. They are the ones who understood, years before the sale, what drives value and built their practice deliberately around those drivers.

Knowing your FCF valuation is not just preparation for a sale. It is one of the most powerful tools you have for running a better practice today.