Fair Value Finally Makes Sense: The IFRS for SMEs Reset

Fair value has always been part of IFRS for SMEs, but the rules were not always clear. Different sections used different guidance, which often caused confusion. The new Section 12 changes this by providing one clear method for measuring fair value across the whole standard. It introduces a simple hierarchy, clear definitions, and better disclosure requirements. This helps accountants apply fair value more consistently and gives users of financial statements a better understanding of how values have been determined and reported.

Your Financial Instruments Fallback Is Gone. Here Is What Replaces It.

The IAS 39 fallback is gone, and the new IFRS for SMEs Section 11 brings a simpler, more practical approach to financial instruments. The key change is the introduction of the SPPI test, which helps determine whether instruments are measured at amortised cost or fair value. Accountants should now review financial instruments, intragroup guarantees, and extended credit arrangements to ensure compliance with the third edition. While some rules have changed, the standard remains focused on providing clear, relevant, and reliable financial information for SMEs.

You Think You Know Who Controls That Company. The New Rules Might Disagree.

For many SMEs, the biggest change in the updated IFRS for SMEs is not how much of a company is owned, but who actually controls it. The revised Section 9 introduces a broader definition of control that looks beyond voting rights and focuses on who has the power to direct key decisions, who is exposed to the risks and rewards of the business, and who can use that power to influence outcomes. As a result, family groups, trust structures, and companies with dispersed shareholders may need to reassess whether consolidation is required, even where no single party holds a majority stake.

Assets, Liabilities and the Rule That Changed Everything

What qualifies as an asset? What creates a liability? These questions sit at the heart of every set of financial statements, yet the answers have changed significantly with the latest IFRS for SMEs updates. The revised framework moves away from a strict focus on probability and places greater emphasis on rights, obligations, relevance, and faithful representation. For accountants and business owners alike, this shift could affect how software licences, intellectual property, contractual rights, legal claims, and other uncertain items are recognised and reported in the years ahead.

The Accounting Standard That Quietly Changed Everything

Accounting standards rarely make headlines, but the latest update to IFRS for SMEs is one of the most significant changes in years. With major revisions to revenue recognition, business combinations, consolidation, financial instruments, and fair value measurement, accountants and business owners need to start preparing now. The transition period is already underway, and those who understand the changes early will be best positioned to guide their clients through what comes next.

The Most Valuable Assets You Cannot See

Intangible assets are often some of the most valuable resources a business owns, yet they are also among the least understood. From software and licences to patents and trademarks, these assets help businesses generate income and remain competitive, even though they cannot be physically seen or touched. Understanding how IFRS for SMEs treats intangible assets is essential for finance professionals, particularly when deciding whether costs should be recognised as assets or expensed. By applying the principles of Section 18 correctly, accountants can ensure that financial statements remain accurate, reliable, and useful for decision-making.

Family Deals, Trust Rentals: 3 Questions to Ask

Related-party transactions are one of the biggest hidden risks in family-run businesses. When family members own suppliers, properties, trusts, or other businesses connected to the company, important disclosures can easily be missed. For independent reviewers and compilers, understanding these relationships is essential to producing reliable financial statements, managing compliance risks, and protecting both the client and their own professional reputation.

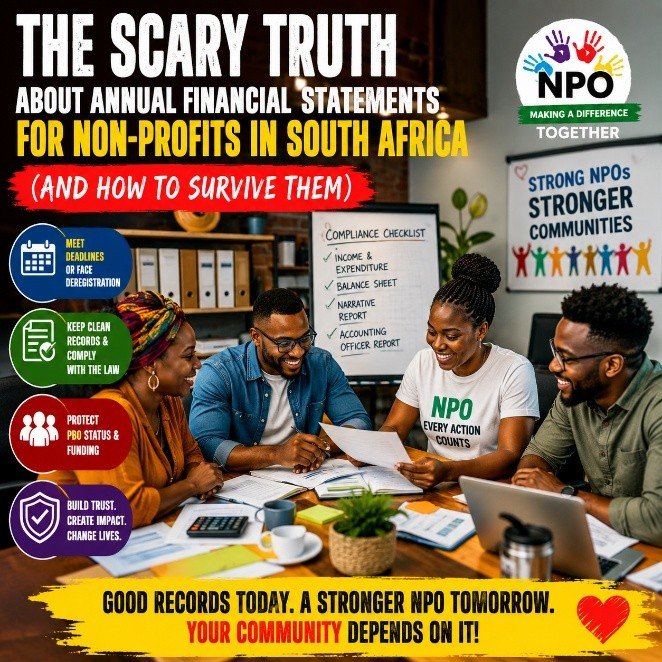

The Scary Truth About Annual Financial Statements for Non-Profits in South Africa

Thousands of South African non-profits are at risk of deregistration simply because their financial statements and compliance records are not in order. This article breaks down what every NPO needs to know about annual financial statements, reporting deadlines, audits, accounting officer requirements, and the real risks of getting it wrong. Written in simple language, it explains how proper financial records protect your funding, your reputation, and your ability to continue serving your community.

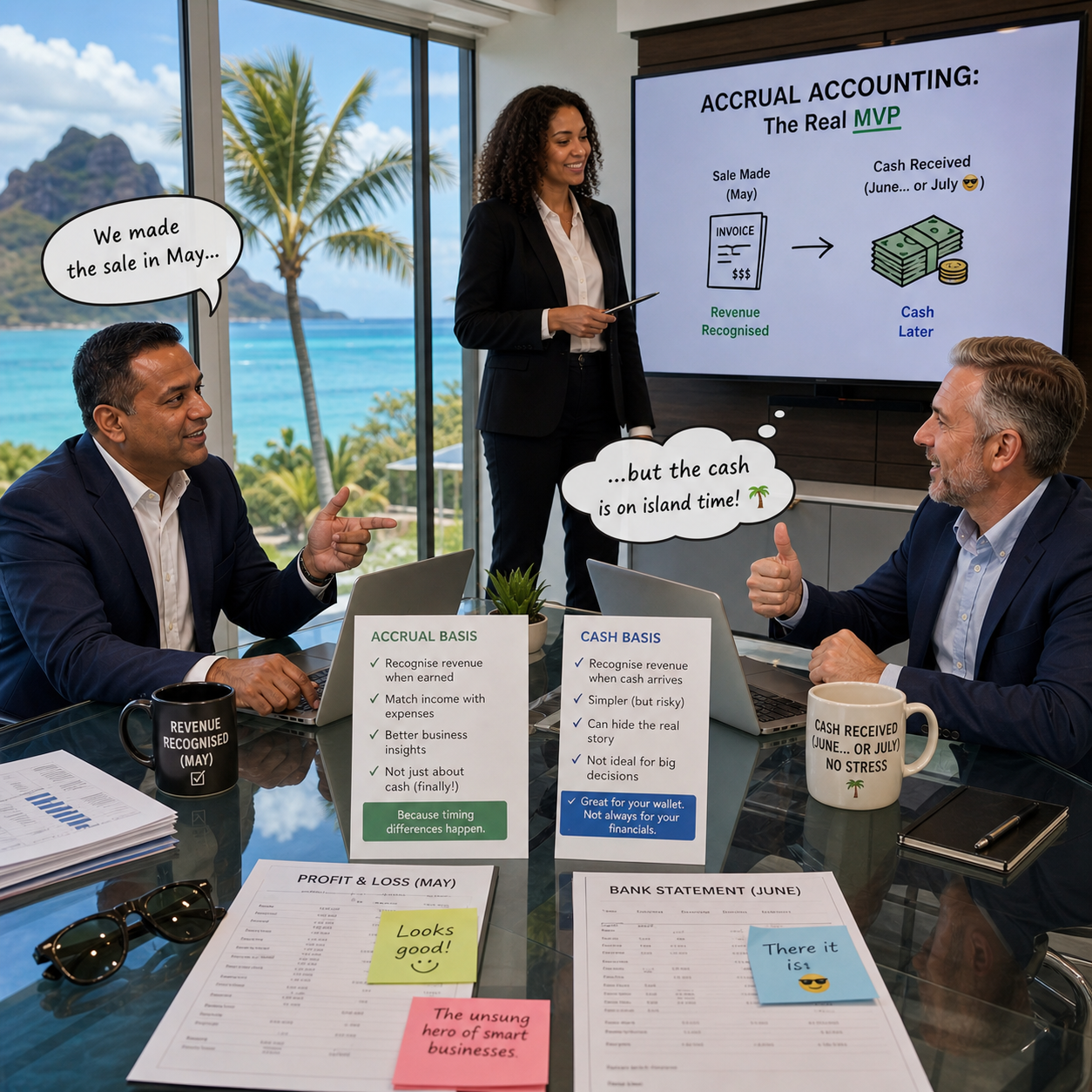

Accrual Accounting: The Quiet Principle That Changes Everything

Accrual accounting is the principle that ensures financial statements reflect what actually happens in a business, not just when cash moves in and out of the bank. By recognising income when it is earned and expenses when they are incurred, it provides a clearer and more accurate picture of performance. This approach moves beyond the simplicity of cash accounting and allows business owners and professionals to understand the true results of their activities, make better decisions, and avoid the misleading effects of timing differences.

As Auditors Sharpen Their Scrutiny of Fraud, Accountants Will Feel the Impact

Fraud is back in the spotlight and accountants need to pay attention. With new changes to the audit standard ISA 240, there’s now more focus on identifying and responding to fraud risks in financial reporting. What does this mean? There will be more questions from auditors, stricter checks on controls, and closer review of red flags like unusual transactions or poor cash flow. Do not be left behind, know what’s changed, what to look out for, and how to stay prepared.

Revenue Recognition: Why So Many Get It Wrong

Many business owners still believe revenue is recognised when the customer orders, pays or collects. But accounting does not follow the cash or the excitement of a new order. It follows performance. Revenue is only recognised when you have delivered what you promised and the customer has gained control of it. This simple idea, performance before payment, is the key to getting revenue recognition right and avoiding the common mistakes that distort profits.

Prepayments: The Hidden Story Behind “Pay Now, Benefit Later”

Prepayments may seem like small accounting entries, but they reveal a lot about how a business thinks about time and value. Paying upfront for future benefits is not just a cash flow decision — it’s a lesson in discipline, foresight, and financial honesty. For accountants in practice, explaining prepayments in plain language can turn a routine adjustment into a powerful conversation about planning, trust, and smarter business. After all, good accounting is not about the past; it’s about making tomorrow’s numbers make sense.

Understanding Amortised Cost: The Measurement Model for Most SME Financial Instruments

Amortised cost is one of the most important measurement tools in SME accounting, yet many professionals are unsure how it works. In this article, we explain amortised cost in simple terms and show how to apply it using the effective interest method. You will learn how to measure loans, receivables, and payables correctly, including how to deal with transaction costs and interest. With step-by-step examples and practical tips, this article helps CIBA members confidently apply Section 11 of the IFRS for SMEs in everyday situations.

Initial Recognition and Measurement: What to Do When You First Record a Financial Instrument

The moment you enter into a contract involving money, whether it’s a loan, a sale on credit, or an interest-free advance, you need to recognise it in your accounting records. Section 11 of the IFRS for SMEs tells you exactly when and how to do this. In this article, we explain the rules for initial recognition and measurement of financial instruments in simple terms. You’ll learn how to record trade receivables, loans, and financing transactions correctly, and how to apply present value when needed. With practical examples and clear guidance, this article helps you get the basics right from day one.

Income Statements That Work as Hard as You Do

Too many accountants still fumble the basics of Section 5 reporting—and that can make your work look sloppy, even if it’s technically correct. Whether you're prepping year-end for a client or presenting to a board, how you lay out that income statement matters. This article breaks down exactly what Section 5 of IFRS for SMEs requires—no jargon, no fluff. You’ll see why choosing one or two statements isn’t just an admin choice, and how small mistakes (like calling something "extraordinary") can raise red flags with SARS or your client.

Farming and Finances: Because Crops Won’t Count Themselves

Understanding how to account for plants, animals, and farm produce is important for businesses in agriculture. IFRS for SMEs Section 34 explains how to record and report biological assets like crops and livestock and harvested products like milk or fruit. This article breaks down the key rules in simple terms, helping businesses stay compliant and manage their finances better.

Your Business in a Nutshell the Statement of Financial Position Explained

The statement of financial position shows what a business owns, what it owes, and what is left for the owners. It helps businesses understand their financial health at a specific point in time. Section 4 of the IFRS for SMEs explains how to present this information clearly. By following these guidelines, businesses can organise their assets, liabilities, and equity in a way that makes sense. This ensures financial reports are accurate and useful for decision-making

Investment Property and IFRS for SME’s

Investment property under IFRS for SMEs refers to land or buildings held for rental income or capital appreciation. The standard outlines how to recognise, measure, and disclose investment property in financial statements. Properties can be measured at fair value if reliably measurable or at cost if not. Mixed-use properties require classification based on usage. Leased properties can be treated as investment property under specific conditions. Proper accounting ensures transparency and accurate financial reporting for SMEs.