Property, Property... Who Are You Really?

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

You've got a building. Great. But here's the question your client's financial statements are asking: Is that building working for the business, or is the business working for that building?

That distinction, deceptively simple on the surface, is at the heart of one of the most misclassified items in SME financial statements: the difference between Property, Plant & Equipment (PPE) and Investment Property.

Get it wrong, and you're not just ticking the wrong box. You're applying the wrong accounting model, disclosing the wrong figures, and potentially misrepresenting your client's financial position to lenders, SARS, and shareholders.

Let's fix that. For good.

The Big Picture: What Are We Even Talking About?

IFRS for SMEs has two separate sections for property assets held by a business:

• Section 17 — Property, Plant and Equipment (PPE)

• Section 16 — Investment Property

They look similar. They're both property. They're both on the balance sheet. But they are governed by different rules, measured differently, and tell a completely different financial story.

Think of it this way: a hammer in a carpenter's workshop is PPE. A hammer sitting in a display case being rented out to a museum is... well, it's a strange investment property, but you get the idea. Same object. Completely different purpose. Completely different accounting.

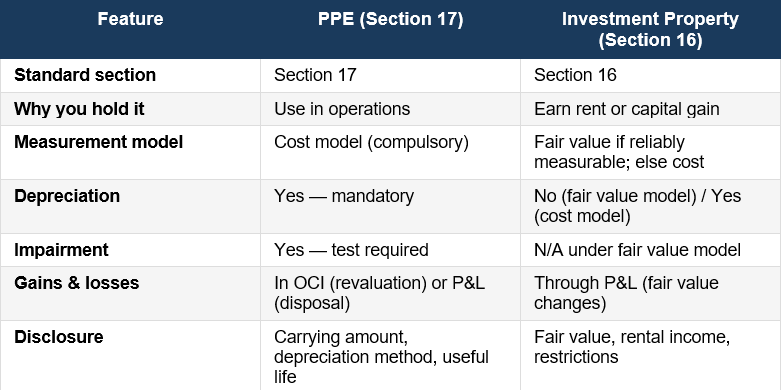

Section 17: Property, Plant & Equipment — The Workhorse

PPE is an asset your business uses to operate. That's the core test: is this asset being used in the production of goods, the delivery of services, for administrative purposes, or for rental in the ordinary course of trade (i.e. if you're a property rental business)?

Examples of PPE:

• A factory building where your client manufactures furniture

• The office building from which the business operates

• A delivery vehicle used daily for logistics

• Machinery used in a construction company's projects

• Rental properties held by a company whose primary business IS property rental

How Do You Measure PPE?

Under IFRS for SMEs Section 17, PPE is always measured using the Cost Model. There is no revaluation model in IFRS for SMEs (unlike full IFRS). The entity:

Initially recognises the asset at cost (purchase price plus directly attributable costs to bring it to working condition)

Depreciates it over its useful life using a systematic method (straight-line, diminishing balance, etc.)

Tests for impairment when there are indicators that the carrying amount may not be recoverable

Real-World Example: Thabo's Bakery

Thabo runs a bakery in Soweto. He owns the building where the bakery operates — he bakes there every day, employs 12 people, and uses every square metre. This building is PPE.

Why? Because the building is used in the business's operations to generate revenue — bread is made and sold there. It gets depreciated over its useful life (say, 40 years), and it sits on the balance sheet at cost less accumulated depreciation.

Section 16: Investment Property — The Passive Earner

Investment Property is property held for one of two purposes:

• To earn rental income, OR

• For capital appreciation (the value goes up and you eventually sell it for a profit)

Crucially, this is property NOT used in the entity's own operations. The business doesn't work in or with this property, the property earns its keep on its own.

Examples of Investment Property:

A spare commercial building your client owns and rents out to a third party, while their actual business operates from a different building

A piece of land purchased with no development intention other than resale at a higher price

A flat rented to a tenant by a manufacturer (not a property company)

A shopping centre owned by an entity whose primary business is manufacturing

How Do You Measure Investment Property?

This is where it gets interesting — and where IFRS for SMEs departs from PPE:

Under Section 16, if the fair value of the investment property can be measured reliably without undue cost or effort, the entity must use the Fair Value Model. If fair value cannot be reliably determined, the Cost Model (same as PPE) is applied.

This is a big deal. Under the fair value model, investment property can increase your client's profit in a year simply because the property value went up — without selling a single unit, baking a single loaf, or issuing a single invoice.

Real-World Example: Ntombi's Side Building

Ntombi also runs a bakery. She owns two buildings. Building A is the bakery (PPE). Building B is an adjacent property she rents to a dentist for R18 000 per month. The dentist has nothing to do with the bakery.

Building B is Investment Property. Ntombi's accountant must assess whether fair value can be reliably determined. If a valuer can value it without undue cost, Building B is carried at fair value — say R2.2 million at year-end. If it was R2 million last year, Ntombi recognises R200 000 in profit from the fair value increase. No depreciation. No impairment test. Just a fair value re-measurement every year-end.

Side-by-Side: PPE vs. Investment Property

The Accountant's Quick-Decision Checklist

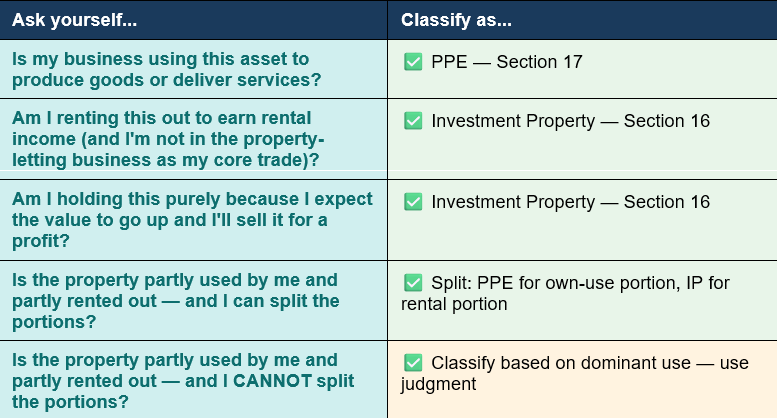

When a client has property on their books, run through these questions before classifying:

The Tricky Middle Ground: Mixed-Use Property

Here's where accountants earn their money. What about a property that is partly used by the business and partly rented out?

IFRS for SMEs Section 16.2 gives you a clear rule: if portions can be sold or leased independently, account for each portion separately — one as PPE, the other as Investment Property.

But if the portions cannot be sold or leased independently — say it's one open warehouse with a small corner sublet — Sipho must ask: what is the dominant use? If most of the space is his warehouse, the whole thing is PPE. He cannot split it arbitrarily.

What Happens When Use Changes? Transfers Between Categories

Properties don't always stay in the same category forever. Life changes. Business strategies change. And IFRS for SMEs deals with this under Section 16.8 and 17.28.

A transfer occurs when there is a change in use — and the change must be evidenced by actual use, not management intention alone.

Common transfer scenarios:

• PPE → Investment Property: Your client stops using the building themselves and starts renting it to a third party

• Investment Property → PPE: Your client takes back a rented-out property to use in their own operations

• Investment Property → Inventory: Your client starts developing the property for sale (e.g. a developer)

Why This Classification Matters — More Than You Think

This isn't just a technical checkbox exercise. The classification of property affects:

• Net profit: Fair value gains on IP go to P&L — PPE under cost model doesn't benefit from appreciation until sale

• Balance sheet strength: Fair value IP shows market-adjusted values; PPE sits at historical cost less depreciation

• Loan covenants: Many bank covenants are tied to specific ratios (like debt-to-equity) which are directly affected by asset values

• Tax implications: Fair value adjustments are an accounting entry only — SARS will have its own view on timing of gains. Your client needs to understand the deferred tax consequences

• SARS scrutiny: Misclassifying rental property as PPE to access wear-and-tear deductions could attract attention

• Investor and lender perception: Rental income and fair value movements signal different risk profiles than operational asset usage

What Must You Disclose?

The standard requires specific disclosures for each category. Here's a quick summary:

For PPE (Section 17.31):

• Measurement basis (always cost for SMEs)

• Depreciation methods used

• Useful lives or depreciation rates

• Gross carrying amount and accumulated depreciation at start and end of period

• Reconciliation of carrying amount (additions, disposals, depreciation, impairment)

For Investment Property (Section 16.10):

• Methods and significant assumptions used in fair value determination

• The extent to which fair value was based on a valuer's assessment

• Rental income earned

• Direct operating expenses (including repairs and maintenance) on the property

• Restrictions on realisation or remittance of income/proceeds

Five Practical Tips for Accountants in the Field

1. Always document the classification decision. Write a brief note at the time of acquisition explaining why the property was classified as PPE or IP. A year later, neither you nor your client will remember.

2. Engage a valuer for investment property. If you're applying the fair value model, use a qualified independent valuer at least every three years, and document the basis of the valuation. The days of 'my client said it's worth R5 million' are over.

3. Watch out for the 'owner's house on the business books' trap. Many SME owners put their personal residence in the company. Unless it's genuinely leased to a third party at arm's length, this is a misclassification risk — and a potential fringe benefit.

4. Revisit property classification at every year-end. Has anything changed? Did the client start using a previously rented-out property? Did they vacate their office and start renting it out? Review annually.

5. Align the accounting with the lease agreement. If there's a lease in place, it should support the IP classification — the tenant, the rental amount, the term. No lease, no investment property income stream. Don't classify something as IP just because it's vacant and you plan to rent it out.

The Bottom Line

The question is never just "what kind of property is this?" The real question is: "what is this property doing for the business, and who controls it for that purpose?"

PPE works for the business. Investment property works independently of it.

As an accountant serving SME clients, you are the person standing between a correct financial statement and a filing that could misrepresent your client's position to everyone who reads it — their bank, their investors, SARS, and potential buyers.

Getting this right is not just a technical requirement. It's part of the professional responsibility that comes with the title you carry.

Choose Your Path to Exclusive Insights

Stay ahead in the world of accounting with premium content designed for professionals like you. Access expert articles, industry trends, and essential resources. Become a CIBA member and claim your CPD hours from CIBA.

CIBA Member Access

R250.00 FREE!

100% Discount when you become a CIBA Member. Join now to claim your CPD Hours. Register here: https://accounts.myciba.org/register