Going Concern in a High-Rate Economy: How to Spot the Cliff Before They Drive Off It

This article will count 0.25 units (15 minutes) of unverifiable CPD. Remember to log these units under your membership profile.

Let's be honest. "Going concern" used to be the boring paragraph at the back of the financial statements. It was the one nobody read. You ticked it, the client signed it, and life moved on.

That world is gone.

The SARB repo rate is sitting at 6.75% and prime at 10.25% as of early 2026. Your SME clients are not borrowing at prime. They are borrowing at prime plus two, three, sometimes five. That means a R1 million overdraft is costing them R150,000 a year in interest alone. That is before they have paid a single supplier. That is before they have paid you.

So when you sign that independent review report, or when you hand over the May management accounts, you are not just doing maths. You are making a call on whether this business will still exist in twelve months. That call has your name on it.

Let's break down what to actually look for. In plain English. Because clients don't pay you to quote IFRS. They pay you to spot the cliff before they drive off it.

What going concern actually means in plain language

A business is a going concern if it can pay its bills for the next 12 months from the date you sign. That is it. Not "is it profitable". Not "does the owner drive a nice car". The question is simple. Can it pay the rent, the staff, SARS, and the bank for the next year?

If the answer is "probably not", you have a problem. So does the client. So does the bank, the landlord, and every supplier giving them 30 days.

Under ISRE 2400, which is the standard you use for independent reviews, and the IFRS for SMEs framework that most of your clients report under, going concern is the default assumption. But "default" does not mean "automatic". You still have to look. In this economy, you have to look harder.

The red flags that matter right now

Forget the textbook list. Here are the ones that will actually bite you in 2026.

1. The interest line is eating the profit. Pull the management accounts. Compare interest expense in 2024 to 2026. If it has doubled while revenue has stayed flat, that business is paying the bank to stay open. A retail client doing R8 million a year with R900,000 in interest is not running a shop. They are running a charity for the bank.

2. The overdraft is the working capital. Look at the bank balance pattern. If they live permanently in the overdraft and never come up for air, that is not a facility. That is a permanent loan dressed up as a facility. And the bank can pull it tomorrow with a phone call.

3. The SARS debt is creeping up. This one is the silent killer. It is especially common in construction, hospitality, and logistics. These are sectors where margins are tight and cash flow is lumpy. When clients cannot pay SARS, they delay PAYE first, then VAT, then they "arrange" a payment plan. By the time you see the SARS statement, the penalties and interest are already 30% of the balance. Ask for the latest SARS statement of account. Every time. No exceptions.

4. The director's loan is going the wrong way. In a healthy SME, the director takes money out of the business. In a dying SME, the director puts money in. That money comes from a personal bond, a credit card, or a family member. If the loan account from the director is growing every month, the business is on life support. The director is the ventilator.

5. Suppliers are demanding cash. Ask the question directly. "Are any of your suppliers requiring upfront payment now?" If a supplier who used to give 30 days now wants cash on delivery, the market already knows. You are just catching up.

6. The lease is up and the landlord is nervous. Think hospitality, retail, beauty salons, and anyone else with a physical footprint. If the lease renewal is coming and the landlord is asking for a personal surety from the spouse too, that is a signal. Landlords do not ask for extra security when business is good.

What to actually do about it

Spotting the red flags is half the job. The other half is documenting it properly. When something goes wrong, your file must show that you did the work.

Do a real cash flow forecast. Not a wishlist. A weekly cash flow for the next 13 weeks. Money in, money out, opening and closing balance. If the closing balance goes negative in week 7, you have a conversation to have. Today. Not at year-end.

Stress-test the interest rate. Yes, rates have started coming down. But they are still high. Take the current interest expense and add 1%. Does the business still cover its costs? If not, document the sensitivity. This is the part most reviewers skip. It is also the part that protects you when a client folds.

Read the loan covenants. A lot of SME loans have covenants the owner has never read. Debt service cover ratio. Minimum equity. Maximum leverage. If the business is in breach, the loan is technically callable. That means the loan is a current liability, not long-term. That single reclassification can flip a balance sheet from solvent to insolvent on paper.

Have the conversation. This is the bit nobody trains you on. Sit the director down. Be direct. "I'm worried about cash. Here's what I'm seeing. Here's what we need to do." You are not just a number-cruncher. You are the person who can see what they cannot see, because they are too close to it.

When you have to qualify

If after all of this you genuinely do not believe the business will survive 12 months, you have to say so. That means a modified going concern note. In serious cases, it means an emphasis of matter paragraph in your review report. Yes, the client will hate it. Yes, the bank manager will get nervous. Yes, you may lose the engagement.

But here is the deeper truth. Your signature is what gives those financials credibility in the first place. If you sign off on a business that collapses three months later, and the file shows you ignored obvious warning signs, that is not just embarrassing. That is your professional indemnity insurance, your CIBA membership, and your reputation. All at risk. For one client who did not want to hear bad news.

The bottom line

In a high-interest-rate economy, going concern is not a paragraph. It is the whole job. Every month, when you produce those management accounts, you are watching the patient's vitals. The reviewer who picks up the trouble in March saves the business. The reviewer who only notices in December gets to write the funeral programme.

SMEs are the engine of this economy. When they fail, jobs go with them. When they survive, because their accountant saw what the owner could not, communities keep eating. That is not a small job. That is why you exist.

Your clients are doing their best in a hard environment. Your job is to make sure their best is enough. And to tell them, clearly and early, when it is not.

That is the work. That is what professional accounting looks like.

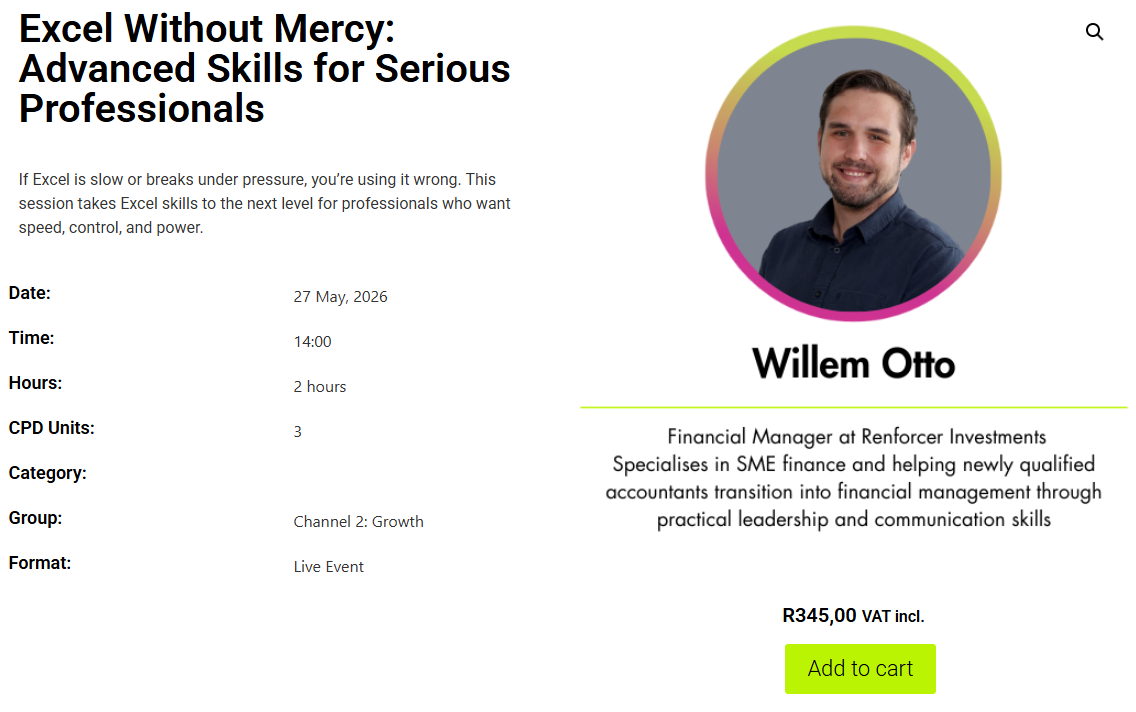

🚨 Excel is about to stop being your bottleneck.

Join Excel Without Mercy: Advanced Skills for Serious Professionals and learn how to work faster, smarter, and with far more control in Excel.

👉 Click here to register

Excel is one of the most powerful business tools in the world — but most professionals only use a fraction of what it can actually do.

If your spreadsheets are slow, break under pressure, or take hours to manage, the problem is not Excel. It is the way it is being used.

Join us for Excel Without Mercy: Advanced Skills for Serious Professionals — a practical session designed for professionals who want more speed, control, accuracy, and confidence when working with data.

This is not theory. This is real-world Excel for people who work under pressure and need results that are fast, reliable, and professional.

📅 27 May 2026

⏰ 14:00

🎓 3 CPD Units

📍 Live Event

💰 Free to CIBA Channel 2 Subscriber / R345 VAT incl. everyone else

You will learn:

✔ Working with large data sets

✔ Advanced formulas and functions

✔ Faster spreadsheet techniques

✔ Error prevention and smarter workbook design

✔ Data analysis tools

✔ Automating repetitive tasks

✔ Professional Excel best practice

Presented by Willem Otto, Financial Manager at Renforcer Investments.

Excel skills are no longer optional for professionals who want to work smarter and stand out.

Choose Your Path to Exclusive Insights

Stay ahead in the world of accounting with premium content designed for professionals like you. Access expert articles, industry trends, and essential resources. Become a CIBA member and claim your CPD hours from CIBA.

CIBA Member Access

R250.00 FREE!

100% Discount when you become a CIBA Member. Join now to claim your CPD Hours. Register here: https://accounts.myciba.org/register