IFRS 20: Profit In The Right Year

This article counts 0.25 units (15 minutes) of unverifiable CPD.

A water utility does a full year of work and reports a loss. The next year it does less and reports a healthy profit. Nothing changed in the business. The accounting just parked the result in the wrong year. Load-shedding means a power utility sells less electricity than the regulator assumed when it set the price. Revenue dips this year, then jumps next year when the utility is allowed to recover the shortfall. The business did not suddenly turn a corner. The billing just caught up.

These mismatches are exactly what the International Accounting Standards Board (IASB)'s new standard, IFRS 20 Regulatory Assets and Regulatory Liabilities, is built to fix for companies subject to a specific type of rate regulation. It was issued in May 2026 and replaces the old interim standard, IFRS 14. It is part of a wider push to sharpen how companies report, alongside the new presentation standard IFRS 18. Here is what IFRS 20 does, who it actually affects, and why most of your SME clients can relax after the scope section.

The problem: when revenue tells the wrong story

Some businesses cannot simply charge what they like. A regulator decides how much they can charge customers and when, and South Africa is full of them. Eskom's prices are set by National Energy Regulator of South Africa (NERSA). Municipalities buy that power and resell it to households and businesses. Bulk water suppliers like Rand Water sell to municipalities under approved tariffs. NERSA also regulates piped gas, Transnet moves fuel through its pipelines on regulated tariffs, and SANRAL sets the toll fees on national roads. In each case a regulator, not the open market, fixes the rate.

The clearest local example of the timing problem is Eskom's Regulatory Clearing Account (RCA). NERSA sets Eskom's allowed revenue for a year based on what it expects Eskom to spend and to sell. When the real numbers come in different, say sales volumes drop or costs run higher, the gap does not simply vanish. It is tracked in the RCA and then clawed back from, or refunded to, customers through tariffs in later years. Eskom has applied to recover billions of Rand this way, spread over several future years.

That is the heart of the problem. The work, and the cost, land in one year, but the matching income only reaches customers' bills a year or more later. When supply and billing fall in different periods, reported revenue stops matching the work actually done. IFRS 20 calls this a difference in timing. A year of solid work can look weak on paper, simply because the income it earned is only allowed to be billed later.

Want me to drop this into the article file? If so, I'll also apply the plain-language rewrite of the "How the model works" section from earlier, since that one is still sitting in the chat and not yet in the file.

How the model works

IFRS 20 works by adding two new items to the financial statements: a regulatory asset and a regulatory liability.

A regulatory asset comes up when the company has already supplied the service, but the regulator has not yet let it charge customers for part of what it is owed. Because the company has a solid, enforceable right to recover that amount through future rates, it records it now as an asset instead of waiting until the cash comes in.

A regulatory liability is the opposite. The company has already charged customers for something it has not yet supplied, so it will have to hand that back later through lower rates. That future "give back" is recorded now as a liability.

Every time you record one of these, the other side of the entry usually goes through profit or loss, as regulatory income when you book an asset, or regulatory expense when you book a liability. It sits on its own line, separate from normal revenue, so a reader can tell what is ordinary trading and what is the timing adjustment.

One important caution. This is not a free pass to pull revenue into an earlier year. You can only put these amounts on the books if they meet the standard's conditions. You need to be satisfied the right or obligation genuinely exists, you need to measure it properly, and in some cases the standard caps how much you are allowed to recognise. So treat "total allowed compensation" as the idea that guides the model, not as permission to record every rand you are hoping to recover one day.

A two-year example

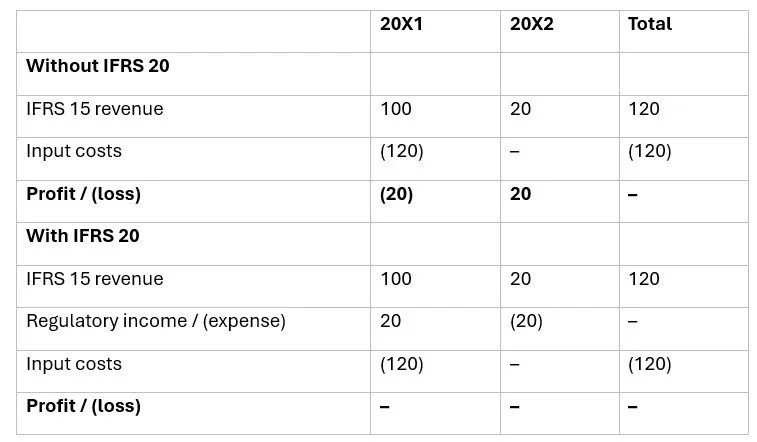

Say a water utility supplies water in 20X1. The regulator lets it recover its actual input costs through the tariff. The 20X1 tariff was set on estimated costs of R100, so 20X1 billed revenue under IFRS 15 is R100. Actual input costs came to R120. The agreement gives the utility an enforceable right to add the CU20 shortfall to the rates it charges customers in 20X2.

Without IFRS 20, the utility shows a R20 loss in 20X1 and a R20 profit in 20X2, even though it supplied the service and incurred the cost in 20X1. With IFRS 20, it recognises a R20 regulatory asset and R20 of regulatory income in 20X1, so the year reflects the full R120 it earned. In 20X2, when the R20 is billed and lands in revenue, it reverses the asset with a R20 regulatory expense so nothing is counted twice. Over the two years total profit is identical. The only thing that moves is the year the profit shows up, and now it sits where the work was done.

It supplements IFRS 15, it does not replace it

This is the point that trips people up. IFRS 20 does not replace your revenue standard. Companies still apply IFRS 15 Revenue from Contracts with Customers to recognise revenue from customers. IFRS 20 sits on top as an overlay, adding separate accounting for qualifying regulatory assets, liabilities, income and expenses. Think of it as a second layer, not a new revenue rulebook.

Not every regulated business is in scope

Here is the scope warning that keeps your file clean. Not every regulated entity will fall within the scope of IFRS 20. The regulatory framework must create enforceable rights and obligations that give rise to regulatory assets or regulatory liabilities. A business can be heavily regulated and still sit outside the standard if its agreement does not create those enforceable rights and obligations affecting future rates. So before you conclude a client is in or out, check the actual regulatory agreement against the standard's definitions, rather than assuming that "regulated" automatically means "in scope".

What about IFRS for SMEs?

For small and medium entities in South Africa, this is the line that matters most. IFRS 20 is a full IFRS Accounting Standard. The IFRS for SMEs Accounting Standard is a separate, self-contained framework, and new full standards do not flow into it automatically. IFRS for SMEs does not contain regulatory assets and liabilities, so an entity reporting under it does not apply IFRS 20. Such an entity would account for any rate-regulation effects using the general recognition principles already in IFRS for SMEs. If that ever changes, it would come through a future amendment to the IFRS for SMEs standard, decided through its own review cycle, and not through IFRS 20.

What this means for your practice today

Most of your clients on IFRS for SMEs are not affected, and you can say so with confidence. The work to do is narrow and specific:

For any client, or any audit, in electricity, water, gas or transport that reports under full IFRS, flag IFRS 20 now and read the regulatory agreement to test whether it is actually in scope.

Remember it is an overlay on IFRS 15, not a replacement, so your revenue accounting does not change, you add to it.

The effective date is annual periods beginning on or after 1 January 2029, with early application allowed, so there is real runway to plan rather than scramble.

Knowing the scope is the value you bring. A client who hears "this big new standard does not apply to you, and here is why" is a client who trusts your judgement on the ones that do.

Also refer to: